Starting next year, New York’s state government plans to (finally) stop deferring a portion of its annual required pension payments—but over the next 10 years, it will still have to repay $3.3 billion it owes on pension fund borrowings since fiscal 2011.

Starting next year, New York’s state government plans to (finally) stop deferring a portion of its annual required pension payments—but over the next 10 years, it will still have to repay $3.3 billion it owes on pension fund borrowings since fiscal 2011.

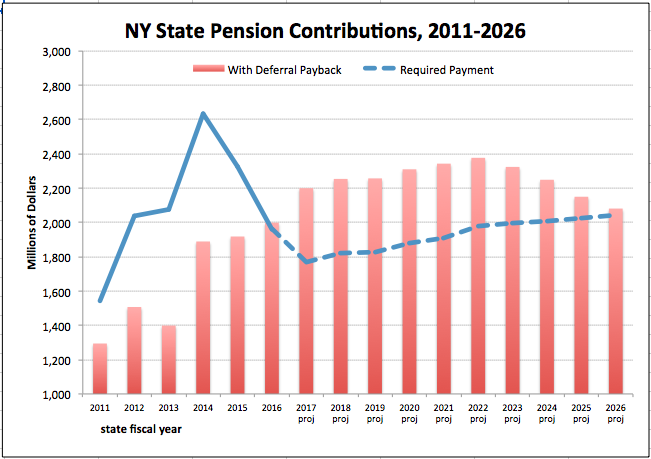

From fiscal 2017 to 2021, as illustrated below, the state expects to pay the New York State and Local Retirement System (NYSLRS) an additional $432 million a year to repay previous pension deferrals, an amount that will decline steadily before ending after 2026, according to data in the Mid-year Financial Plan Update. The report was posted by the Budget Division late Thursday—six days past the statutory deadline.

Instead of making its fully required pension payment, the state effectively has borrowed a total of $3.6 billion from NYSLRS since fiscal 2011, including $350 million in fiscal 2016, which ends next March 31, the financial plan update says. Through this year, it will have repaid about $1 billion, leaving it still owing $3.3 billion, including interest.

This pension gimmick was first allowed under a 2010 law proposed by Comptroller Thomas DiNapoli and signed by former Governor David Paterson. As recently as the summer of 2014, Cuomo was assuming the state would resume making its full required pension contributions, as well as scheduled payments on past deferrals, starting in fiscal 2016. But that changed after the pension fund adopted a new “mortality table” reflecting the longer lifespans—and therefore greater benefit expense—of younger retirees and current workers.

Last month, DiNapoli approved more changes to pension actuarial assumptions that, taken together, will have the effect of slightly lowering the pension contribution rates in the coming decade. Based on those changes, Cuomo has dropped his plan to borrow more, effectively reverting to what he had been intending to do until year ago.

Confused? You’re not alone. The complexity of a traditional defined-benefit pension plan makes it prone to manipulation of this sort.

The main thing to remember is that all this is all fraught with risk. If the pension fund falls short of its average annual investment return target of 7 percent over the next few years, the state’s pension costs would go up. Say, for example, that within the next three or four years, the stock market actually experiences a downturn even half as bad as the 2007-09 crash. In that case, pension contributions would rise sharply again before the state is even done paying what it borrowed in the aftermath of the financial crisis.

You may also like

Cuomo’s House Testimony Added New Misinformation about Covid in Nursing Homes

Throughout the scandal over former Governor Andrew Cuomo's handling of Covid-19 in nursing homes, Cuomo and his administration repeatedly spread bad information – misstating how its policies had worked, understating death Read More

What Paul Francis Got Wrong About the Empire Center’s Nursing Home Research

In February 2021, the Empire Center published the first independent analysis of the Cuomo's administration much-debated directive ordering Covid-positive patients into nursing homes. The report found that the directive was associated with a statistically significant increase in resident deaths in the homes that admitted the infected patients. Read More

Internal Cuomo Administration Documents Showed Evidence of Harm from Nursing Home Order

State Health Department documents from June 2020, newly unearthed by congressional investigators, appear to show harmful effects from a controversial order requiring nursing homes to admit Covid-positive patients.

Read More

NY Taxpayers Face Bitter Truth from Sweeter Pensions

Governor Hochul and state lawmakers this year approved a costly giveaway for public employee unions that retroactively hiked pension benefits. Now the bill is arriving. Read More

On Covid in Nursing Homes, There’s No Comparison Between Cuomo and Walz

Former Governor Andrew Cuomo and his political critics have something in common: They're both trying to drag Minnesota Governor Tim Walz into Cuomo's nursing home scandal.

Cuomo’s attempt to hide behind Walz, li Read More

A Closer Look at $4 Billion in State Capital Grants to Health Providers

[Editor's note: This post was corrected after it came to light that records supplied by the Health Department gave wrong addresses for 44 grant recipients. The statistics and tables below were updated on July 18.] Read More

Hochul’s Pandemic Study Is a $4.3 Million Flop

The newly released study of New York's coronavirus pandemic response falls far short of what Governor Hochul promised – and the state urgently needs – in the aftermath of its worst natural disaster in modern history. Read More

82 Questions Hochul’s Pandemic Report Should Answer

This is the month when New Yorkers are due to finally receive an official report on the state's response to the Covid-19 pandemic, one of the deadliest disasters in state history.

T Read More