EXECUTIVE SUMMARY

EXECUTIVE SUMMARY

As recently as 2000, all 50 states joined the federal government in imposing some form of tax on property and assets left by the deceased. However, the national landscape of the estate tax—also known as the death tax—has shifted dramatically since 2001, when the federal government began to phase out a tax credit that neutralized the impact of most state estate taxes.

In response to the federal change, two-thirds of all states—including California, Florida and Texas—have allowed their own estate taxes to disappear. New York is among the holdouts—one of 14 states that still tax estates.

As of 2014, the federal estates and gifts tax applies only to taxable assets exceeding $5.34 million, or up to double that amount for a married couple. New York, however, still taxes estates with gross values starting at a fixed level of $1 million, with no added break for spouses.

The extensive reach of New York’s tax is reflected in tax filing statistics. In 2012, federal death taxes were owed by a total of 3,738 estates nationwide. That same year, New York alone collected state taxes from nearly 4,000 estates. Because it is tied to the rules of the pre-2001 federal law, New York’s estate tax also imposes higher compliance costs on those subject to it.

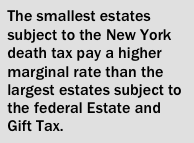

In another twist, the smallest estates subject to the New York death tax effectively pay a higher marginal rate than the largest estates taxed by the federal government.

In another twist, the smallest estates subject to the New York death tax effectively pay a higher marginal rate than the largest estates taxed by the federal government.

The state’s enacted budget for fiscal 2014-15 reforms the New York Estate Tax by phasing in an increase in the basic estate exclusion to match the federal threshold. This would reduce the number of estate tax filings by 90 percent—a giant first step toward complete repeal. But because the budget did not include Governor Andrew Cuomo’s original proposal to reduce the Estate Tax rate, there has been no change in the tax burden potentially faced by New York’s wealthiest residents—who, research suggests, are most likely to move in order to avoid or minimize the impact.

As reviewed in this report, the reasons why New York’s death tax should be killed, once and for all, include the following:

• It will hit a growing number of middle- and upper-middle class households, family-owned small businesses and farms.

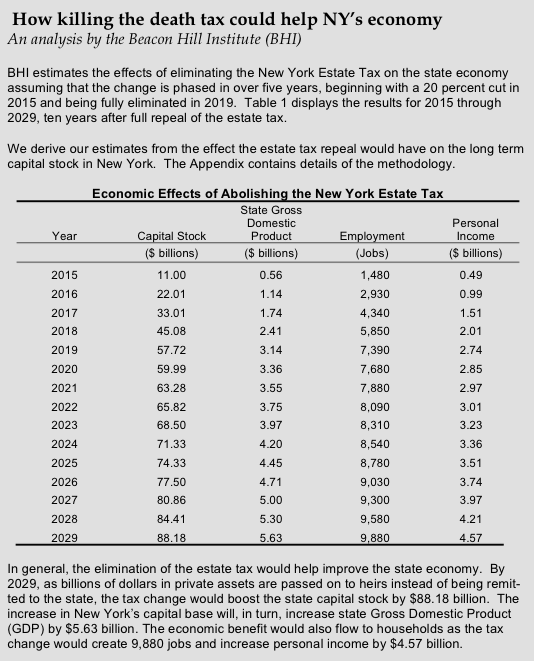

• It hinders economic growth. Repealing the tax could ultimately boost the state’s net economic output by $5.6 billion dollars—five times the revenue it currently generates—and lead to the creation of nearly 10,000 additional jobs, according to an econometric analysis by the Beacon Hill Institute.

• It gives too many New Yorkers yet another incentive to “move to die,” as the governor has put it. The wealthiest New York residents with the biggest estates are most likely to migrate to avoid a higher death tax, research cited in this report would suggest.

Note: The original print download edition of this Special Report, including the material that follows on this web version, does not reflect the Estate Tax changes adopted as part of the enacted 2014-15 budget.

1. ORIGINS AND BACKGROUND

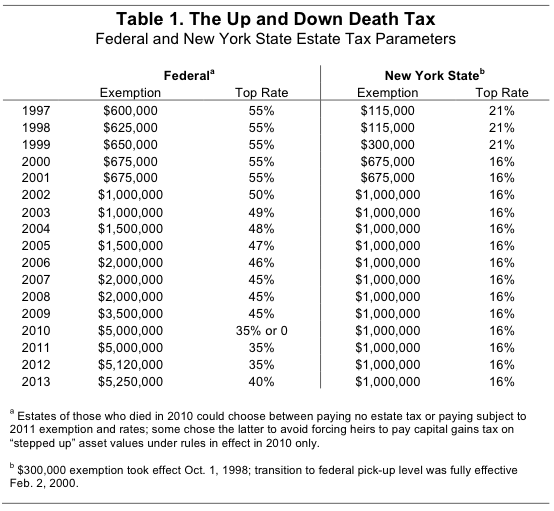

New York has been imposing some form of death tax since the late 19th century; the current version of the state Estate Tax, based on the Estate and Gift Tax provisions of the federal Internal Revenue Code, dates back to 1963. As in most states, the recent history of changes to New York’s Estate Tax is closely related to significant changes in the same tax at the federal level.

The federal Estate Tax was first enacted in 1916 and amended 10 years later to include a credit for death taxes paid to states. A state tax equaling the maximum amount of the federal credit was known as a “pick-up tax,” because it picked up what would otherwise be paid to the federal government if no state tax were imposed. In permitting this arrangement, the federal government was effectively sharing estate tax revenues with the states. For nearly as long as the federal credit existed, all 50 states imposed at least a pick-up tax on estates—and some, including New York, imposed their own added estate taxes on top of that.

By the mid-1990s, New York was one of only a dozen states still taxing estates at a higher level than the pick-up tax. New York’s tax affected gross estate values starting at just $115,000, much lower than the federal exemption (at the time) of $600,000. More than 20,000 New York estates owed taxes to Albany every year.

That began to change in 1997, when then- Governor George E. Pataki signed a law repealing New York’s added estate tax. As of Feb. 1, 2000, New York’s estate tax would equal the state death tax credit on federal returns, thereby eliminating any separate New York burden for all estates. It then became one of 37 states to rely solely on the pick-up tax.

That began to change in 1997, when then- Governor George E. Pataki signed a law repealing New York’s added estate tax. As of Feb. 1, 2000, New York’s estate tax would equal the state death tax credit on federal returns, thereby eliminating any separate New York burden for all estates. It then became one of 37 states to rely solely on the pick-up tax.

The change reduced New York estate tax liabilities by an average of 40 percent, eliminating the death tax for more than 80 percent of estates that would have been subject to it under the prior law. The 1997 reform also repealed New York’s gift tax, leaving only four other states still imposing such a tax at the start of 2000.

The Empire State’s historic reform had been in full effect for barely a year when Congress passed the Economic Growth and Tax Relief Reconciliation Act (EGTRRA), which included nine-year a phase-out of the federal Estate and Gift tax, aiming to eliminate the tax in 2010. The state death tax credit was phased out on an accelerated basis, expiring in 2005. This essentially resurrected a separate, added estate tax in New York and other states whose laws continued to link their death taxes to the previous federal statute.

The result: while New York’s estate tax affects fewer estates at lower rates than applied through the 1990s, it is once again out of line with the norm in the vast majority of states.

New York’s estate tax reform statute is specifically based on the federal law as it stood in 1998, so New York’s tax remained in effect at the 1998 pick-up level even as the federal tax was phased out. Another eight states adjusted their laws to do much the same thing, while 11 states had a stand-alone tax as of 2002. Thirty states had laws incorporating whatever pick-up credit existed under the federal law of the moment, so their taxes disappeared along with the credit in 2005.

To comply with federal budget rules, EGTRRA (which also included President George W. Bush’s income tax cuts) had a sunset date of Dec. 31, 2010. If no other action had been taken by Congress, the old estate tax law—complete with the pick-up credit for state death taxes—would have gone back into effect in 2011. That would have restored a level playing field for states like New York, but it also would have meant a huge immediate increase in the size and scope of the federal estate tax.

Instead, the federal death tax was brought back to life. At the end of 2010, President Barack Obama and Congress agreed to revive the tax for at least two years, with a top tax rate of 35 percent and an exemption level of $5 million. Two years later, a permanent new Estate Tax was enacted, imposing a maximum rate of 40 percent and setting the 2013 exemption at $5.25 million, indexed to rise annually with inflation.

Table 1, below, shows the changes in federal rates and exemptions related to New York’s death tax law from 1997 through 2013.

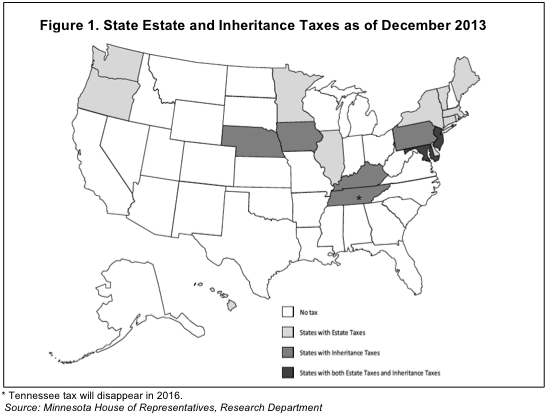

Mapping the death tax

As of January 2014, New York was one of 14 states with an estate tax, including two that imposed both estate and inheritance taxes. Another five states imposed inheritance taxes only. Indiana and North Carolina repealed their death taxes effective in 2013, and Ohio’s 2010 death tax repeal also took full effect last year. Tennessee’s death tax is being phased out and is scheduled to disappear by 2016. Pennsylvania has begun to chip away at its inheritance tax, eliminating the tax on family farms and family-owned small businesses.1 As the map shows, state death taxes have disappeared in most of the South and all of the Southwest and Rocky Mountain regions.

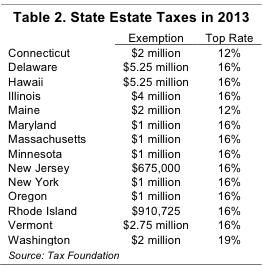

Half of the states still imposing estate taxes in 2013 had exemptions higher than New York State’s $1 million, which means they taxed fewer estates than New York did. Four states matched New York’s $1 million exemption (including Minnesota, which exempts $4 million of qualified small business and farm property), while only two states had lower exemption levels.

Half of the states still imposing estate taxes in 2013 had exemptions higher than New York State’s $1 million, which means they taxed fewer estates than New York did. Four states matched New York’s $1 million exemption (including Minnesota, which exempts $4 million of qualified small business and farm property), while only two states had lower exemption levels.

Reflecting their origins in the old federal pick-up credit, most of the state taxes had top rates of 16 percent. Connecticut and Maine were lower, and Washington (which has no income tax) was higher.

2. DEATH TAX NUTS AND BOLTS

On both the federal and state levels, the Estate Tax applies to the value of cash, real estate (including homes), stocks and bonds, life insurance and other assets owned by a person who has died.2 If the deceased person was not a resident of New York, his or her estate can nonetheless be taxed based on the value of real estate or tangible personal property it owns in New York State.3

The starting point for calculating the estate tax is the total value of property and assets, reduced by the amount of any bequests to spouses, charitable contributions and certain other gifts. As noted, the federal government excludes estates worth less than $5.34 million from taxation (up from $5.25 million in 2013). New York State’s death tax applies to all estates worth more than $1 million, a hangover from the pick-up credit mechanism of the pre-2001 federal tax.

Effective in 2013, the federal Estate Tax exemption is “portable” from one spouse to another, allowing the surviving spouse to apply the decedent’s unused exclusion to reduce taxes on his or her estate. This effectively doubles the exclusion to as much as $10.68 million for married couples as of 2014. New York, however, does not allow for portability of its exemption among spouses.

Effective in 2013, the federal Estate Tax exemption is “portable” from one spouse to another, allowing the surviving spouse to apply the decedent’s unused exclusion to reduce taxes on his or her estate. This effectively doubles the exclusion to as much as $10.68 million for married couples as of 2014. New York, however, does not allow for portability of its exemption among spouses.

Adding further to the cost of the state death tax, New York’s exemption is not a threshold but a cliff. Estates worth up to $1 million pay no tax—but above that amount, the tax applies to the entire estate, starting at the first dollar.

In effect, New York and other states basing their death taxes on the old federal law impose much higher “bubble” marginal rates on estates valued just above the exemption amount.4 For example, the New York tax on a gross estate of $1.08 million is $32,800—which equates to a marginal rate of 41 percent on the $80,000 in assets exceeding $1 million.

On the federal level, a tax credit effectively wipes out any tax on the first $5.34 million of taxable estate value. Amounts above that level are taxed at a 40 percent rate.

In place of the old pick-up tax credit, the new federal Estate and Gift Tax allows deductions for state death taxes. For the very largest estates, this reduces New York’s 16 percent top rate to a maximum effective rate of 9.6 percent. But smaller estates subject only to state law effectively pay almost that much to Albany alone. The estate of a New Yorker dying in 2014 with taxable assets of $5.34 million would be free of federal tax while owing $431,600 in state tax, an effective rate of 8 percent.

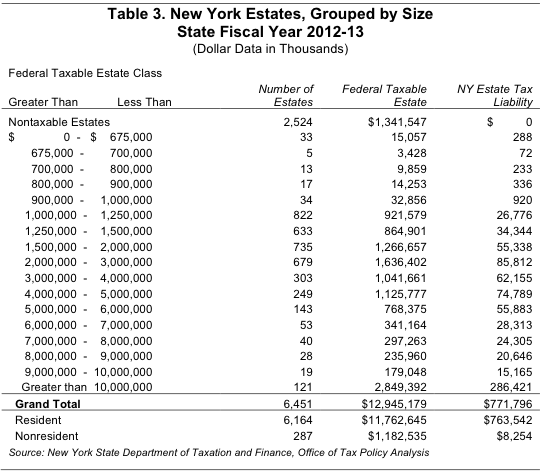

Between fiscal years 2003-04 and 2012-13, an average of 6,624 estates filed New York estate tax returns annually, according to data from the Department of Taxation and Finance. Of that number, an annual average of 4,077 estates owed tax to the state. In 2012-13, the average tax liability for all taxable estates was $196,400.

Ninety percent of New York’s taxable estates in 2012-13 were valued at less than $5 million, which was the federal tax threshold for most of that year.5 They generated 44 percent of the state’s total estate taxes, with an average liability of $96,810. Details are presented in the table below.

The number of estates subject to the federal Estate and Gift tax has decreased sharply since the EGTRRA reforms were initiated.

In 2000, the last year of the old federal pick-up tax structure, 7,396 New York estates filed federal estate tax returns, and 3,963 of those estates were taxable. As recently as 2004, after the phase-out of the federal tax had begun, the number of federally taxable estates in New York (2,591) was roughly equal to the number of estates subject to the state tax (2,837).

In the last decade, however, the number of New York estates taxed by the state has far exceeded the number subject to federal taxes. In 2012, just 855 New York estates filed federal returns, and only 279 of those estates owed federal estate tax—just 7 percent of the number with a state death tax liability in 2012-13.

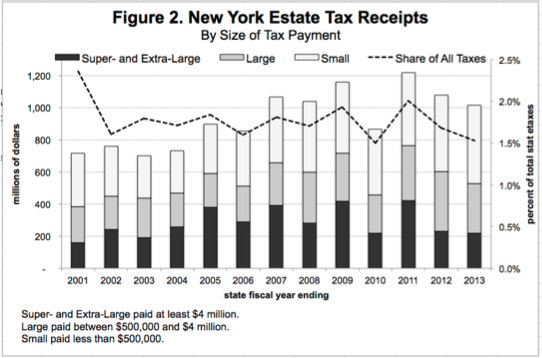

In fiscal 2012-13, New York’s estate tax raised just over $1 billion in revenue, including installment payments from previous years. That was about 1.5 percent of total state tax collections, the second lowest share since New York’s current estate tax structure became fully effective in 2000.

Receipts from the estate tax, which are uneven and difficult to forecast, have decreased as a share of total tax revenue since the reform of the 1990s.

The segmented bars in Figure 2, below, show the ups and downs of estate tax collections since the state moved to its current law in 2000. One notable trend has been the increase in the share of estate tax receipts generated by small estates—those paying $500,000 or less in taxes, which would generally have taxable assets of less than $5,000,000. Small estates were the source of 63 percent of all receipts from the tax in fiscal 2012-13, according to the fiscal 2014-15 Executive Budget. This could reflect a combination of more estates worth over $1 million, an increase in tax avoidance planning by wealthier New Yorkers, and the lingering impact on financial asset values of the stock market crash in 2008-09.

Assuming no change in state law, the state’s November 2013 Mid-Year Financial Plan Update projected that the estate tax share of all tax revenues would continue to decrease through 2017.

3. FOR WHOM THE TAX TOLLS

Estates worth $1 million or more—and thus potentially subject to the state death tax—equated to 16 percent of all wills admitted to probate in New York over the past decade.6 After deducting bequests to spouses, charitable contributions and other non-taxable items, about 62 percent of estates filing a return were still large enough to owe New York estate taxes.

How many New Yorkers are in a position to leave $1 million or more when they die?

The answer is by no means limited to the “1 percent” vilified by Occupy Wall Street protestors.7 In fact, it includes many middle- and upper-middle class New Yorkers who have worked and saved their way to that level.

Who has gotten to be a millionaire?

Political debates over the tax treatment of “millionaires” tend to focus on people reporting incomes of at least $1 million a year. This group, consisting of 38,240 New York resident individuals and couples as of 2011, actually comprises the upper half of the top 1 percent of tax filers in the state that year.8

However the dictionary definition of “millionaire” is broader.9 Millionaires aren’t just those who earn $1 million in any given year but those who own $1 million worth of property—land, buildings, insurance policies, farms, businesses, stocks, bonds, cash and other goods.

However the dictionary definition of “millionaire” is broader.9 Millionaires aren’t just those who earn $1 million in any given year but those who own $1 million worth of property—land, buildings, insurance policies, farms, businesses, stocks, bonds, cash and other goods.

And as it turns out, that’s a much larger group.

New York was home to 429,153 households with assets of $1 million or more as of 2013, according to a report produced by Phoenix Marketing International.10 The report said that “millionaire households” made up 5.79 percent of all households in New York, the 12th largest share of any state.11 Since married couples comprise about 44 percent12 of New York households, this estimate suggests more than 600,000 adult state residents either have wealth of $1 million or more, or share it with a spouse.

The Phoenix Marketing report is a state-by-state approximation of household “investable” assets, such as stocks held in an individual retirement account, but does not include real property. Thus, if anything, it under-estimates the true number of millionaire households in New York. For example, more than a few residents of New York City and surrounding suburbs live in homes and apartments, purchased years ago for modest sums, whose value now approaches or exceeds $1 million.

Downstate homeowners aren’t the only middle-class New Yorkers who have seen their property values sharply appreciate. The average price of agricultural land in New York has nearly doubled since 2000, increasing from $1,430 to $2,600 per acre.13 There were 3,142 New York farms worth $1 million or more as of 2007.14

Homes and properties aside, millions of New Yorkers also own small businesses. Depending on the industry, even small firms generating a relatively modest income for their owners can be worth a significant amount. For example, a small manufacturing company with earnings of $150,000 before interest, taxes, depreciation, and amortization could be worth $825,000 to $1.275 million.15

New Yorkers who don’t own their own farms or businesses can amass seven figures or more in assets merely by following advice to save sufficiently for retirement. Take, for example, a couple approaching retirement with combined income of $130,000—squarely in the middle class by downstate standards. They would need $1 million to buy an annuity replacing half their lost wages starting at 65.

In sum, while the recent thrust of state tax policy has been to provide relief for the middle class, the growth in asset values means the New York estate tax will hit a significant number of such families, including small business owners and farmers.

Economic impacts

In a 2006 report examining the arguments for and against taxing estates, the Joint Economic Committee of Congress came to this conclusion:

The rather small potential benefits of the estate tax stand in sharp contrast to large and significant costs of the tax. The estate tax discourages savings and capital accumulation, thus impeding economic growth. Small businesses and innovation suffer as well, as the estate tax reduces funds available for investment and employment, and destabilizes the business at a vulnerable moment, the death of the founder or current leader of the enterprise. Since owning a small business is a key means for lower- and middle-income families to accumulate wealth, the estate tax also hinders economic mobility. Even the environment is harmed by the estate tax, since the enormous liquidity demands of the tax force owners to sell and develop environmentally sensitive habitats in order to meet their estate tax obligations. On top of all these costs, the estate tax lacks the basic features of good tax policy due to its complexity and lack of equity.16

Since that study was issued, the federal tax has been reformed and simplified so that it affects a much smaller number of estates. By remaining among the small number of states retaining a pre-2001 version of the estate tax, New York will continue to experience the negative impacts cited in the JEC report. Conversely, by repealing the tax, the state can remove a hindrance to savings and capital accumulation, expanding the pool of funds for small business investment and employment.

The benefits of doing so were estimated for the Empire Center by the Beacon Hill Institute of Boston, Ma., as presented in the analysis below.

The costs of complying with—or avoiding—the estate tax can be another drag on the economy. As one economist supportive of retaining but reforming the estate tax has put it, “People spend substantial time and money organizing their financial affairs, buying insurance policies, and constructing wills and trusts to minimize taxes on their estates, all an unproductive waste of resources.”17

In a quarter-century of debates over death tax policy on a national level, estimates of compliance costs associated with the estate tax ranged widely, from 7 percent18 to 100 percent19 of the revenues raised by the tax. Whatever the true level may be under the new federal tax structure, there can be little doubt that New York imposes significant added compliance costs on a larger number of residents by maintaining an additional estate tax based on the old federal law.

“Moving to die”

While the impact of state taxes on taxpayer migration is debated by economists, there is no lack of studies finding a link between taxes and locational decisions.20 The effect of estate and inheritance taxes, in particular, was most recently and thoroughly examined in a 2004 paper by economists Jon Bakija and Joel Slemrod.21

Based on an analysis of estate filings over 18 annual intervals between 1965 and 2000, Bakija and Slemrod found that “high state inheritance and estate taxes and sales taxes have statistically significant, but modest, negative impacts on the number of federal estate tax returns filed in a state.” Specifically, they said, “a one percentage point increase in the wealth-class-specific effective state (estate and inheritance) average tax rate is associated with 1.4 percent to 2.7 percent decline in the number of federal estate tax returns filed in the state, depending on the specification.”

The researchers also found that estates worth more than $5 million were “particularly sensitive” to death tax rates, with filings in this class declining by 4 percent for every percentage point increase in taxes. This finding is particularly relevant to current circumstances, since the new federal estate tax threshold above $5 million, and the difference among states with and without death taxes is higher than it was for much of the period covered in the study.

What Connecticut found

In 2007, the Connecticut Department of Revenue and Office of Policy Management surveyed practitioners in the legal, accounting and estate planning communities to determine the impact of that state’s death tax on the migration of taxpayers.22 Most of the 166 survey respondents were from Fairfield, Hartford, and New Haven counties, including affluent suburbs comparable to those in Westchester County and Long Island in New York State.

About 77 percent of the respondents said they had clients who had moved out of Connecticut “partially” to avoid the state’s estate tax, including 53 percent who indicated clients had moved “primarily” as a result of the tax.

The average gross estate of those changing their Connecticut domicile was $7.5 million, which would equate to a Connecticut tax of $705,000, and the average income of those migrating to other states was $446,000, the study said. The top four destinations for those leaving Connecticut, the survey respondents indicated, were Florida, Arizona, North Carolina and New Hampshire. Estate tax concerns were the leading reason for clients’ changes in domicile, followed by “climate/recreational activities” and the state income tax.

The same study compared economic growth indicators between 2004 and 2007 for states with and without added estate and inheritance taxes. It found that employment, personal income, real gross state product and population all grew faster during that period in the states without death taxes.23

The findings were consistent with anecdotal information presented to Governor Cuomo’s Tax Reform and Fairness Commission. During its outreach meetings, the Commission reported, “tax practitioners and business leaders noted that the low exemption threshold of the estate tax was a possible factor in taxpayer migration from New York to states without an estate tax.”24

It’s noteworthy that Connecticut’s threshold already was twice as high as New York’s, thus taxing fewer estates, during the period covered by the Department of Revenue study (although, unlike New York, Connecticut also continues to impose a separate gift tax). More recently, the Nutmeg State has lowered its estate tax rate from 16 percent to 12 percent.

4. PROPOSED REFORMS

Governor Andrew Cuomo’s fiscal 2015 Executive Budget called for the most significant reduction and reform of the New York Estate Tax in 17 years. Under the governor’s proposal:

• The state tax exemption would be raised in stages from its current $1 million to match the federal level in effect in 2019—which, assuming 2 percent inflation in the meantime, will approach $6 million. 25

• The maximum rate would be lowered from 16 percent to 10 percent.

The budget also would have repealed the state’s generation-skipping transfer tax (GST) on estate beneficiaries two or more generations removed from the decedent. New York’s GST is based on a federal credit that expired in 2004, “affects a few dozen taxpayers each year, yields minimal annual revenue, and frequently causes taxpayer confusion,” the governor’s bill memorandum said. “Repealing this tax would result in minimal revenue loss and provide taxpayer relief.”

Cuomo’s budget proposal also includes one change that would tend to increase the scope of the state death tax, by requiring gifts made after April 1, 2014 to be included in an individual’s estate. The memorandum in support of the governor’s proposalsaid it would be “closing a loophole by preventing deathbed gifts from escaping the estate tax.” However, the actual bill language does not appear to limit the time period before death in which gifts would be considered taxable; therefore, it could significantly broaden the base of the tax for those who remain subject to it.

The governor’s proposal goes beyond options identified in the November 2013 report of his Tax Reform and Fairness Commission, which suggested raising the exemption to $3 million but did not call for a change in the tax rate. The repeal of the GST and reinstatement of a gift tax were also options cited by the Commission.

In related change, Cuomo’s budget bill would follow through on a Commission’s suggestion by amending the state’s personal income tax law to, in the words of his budget memorandum, “tax distributions of accumulated trust income to New York beneficiaries of non-resident trusts and exempt resident trusts” and “eliminate a loophole that allows incomplete gift, non-grantor trusts set up by New York residents to completely avoid New York income tax.”

If it had been effective in 2012-13, the governor’s proposal would have eliminated the tax for 90 percent of the estates with taxable returns that year. If enacted, it will save smaller estates a net $33 million in 2014-15, growing to $757 million in 2019.

To be sure, Cuomo’s proposal would not eliminate the competitive disadvantage created for New York by the existence of a separate state tax. Nor would it completely eliminate an incentive for the wealthiest households to move. But it would represent a giant first step on the road to repeal.

CONCLUSION

On both the state and federal level, the death tax has been promoted as a means of breaking up and redistributing concentrations of inherited wealth. But research by economists Jagadeesh Gokhale and Pamela Villarreal found that inheritances make a “surprisingly small” contribution to personal wealth and inequality.26 “More importantly, skills acquired through education, entrepreneurship and hard work determine whether individuals move from one wealth level to another,” they said.27

As shown in this report, most of the estates affected by the existing New York tax represent the accumulated business values and life savings of individuals, couples and families who are not among the wealthiest one percent. There are easily 10 times as many households with investable assets of more than $1 million as there are New York tax filers with incomes of at least $1 million.

As also documented here, New York’s estate tax suppresses economic growth by creating a disincentive to save and invest. Its repeal would add billions to the economy and lead to more job creation.

In the final analysis, the strongest argument against maintaining New York’s estate tax at any rate on any level of wealth is the disappearance of such taxes from most other states. This creates yet another competitive disadvantage for the Empire State, which has led the nation in its domestic out-migration loss of population.28

The appendix and endnotes can be found on the pdf of the report.

You may also like

34 MTA Workers Made $200K+ In Overtime In 2025

Thirty-four employees of the Metropolitan Transportation Authority (MTA) received more than $200,000 in overtime payments in 2025, as total annual pay surpassed half a million dollars for some, according to , the Empire Center’s governm Read More

Overtime on State Payroll Jumps 21%

104 employees made over $500k in 2025 total annual pay.

2,450 employees were paid more than Gov. Kathy Hochul's Read More

Seven Reasons Not To Raise Taxes in New York

Despite the robust growth of state revenues in recent years, many of New York's elected officials are pushing to further increase the tax burden on the state's residents and businesses.

Read More

Ninety New York Educators Receive $300k+ in Annual Pay

Ninety employees from New York’s school districts (outside New York City) received more than $300,000 during fiscal year 2025, according to , the Empire Center’s transparency website.

The public educator pay data are based on salary information rep Read More

NYC Employees Receive $300k+ in Overtime

Two New York City employees received more than $300,000 in overtime payouts, according to fiscal year 2025 , the Empire Center’s government transparency website. The city paid a total of $2.9 billion in overtime during fiscal year 2025. Read More

State Lawmakers Spend $268 Million on Legislative Operations

Spending by state lawmakers on office personnel and administrative costs varies widely, with some paying out nearly twice as much as others on their office operations, according to the most recent reported, posted to SeeThroughNY.net.

Read More

School Districts Plan To Spend Over $35K Per Student, Outpacing Inflation

School districts presenting budgets to voters on Tuesday, May 20, plan to spend an average of $35,012 per student, up 4.6 percent from the current school year, according to new state data.

Data collected by the state Education Departme Read More

Overtime on State Payroll Surges 11%

Twenty-three New York State employees collected over $200,000 each in overtime, according to posted today on SeeThroughNY, the Empire Center’s government transparency website. Read More