THE PROBLEM:

New York’s property tax levy cap makes it more important than ever for local governments and school districts to bring their long-term spending into line with long-term revenues. This is an especially challenging task in the wake of an economic slowdown that has strained the finances of local taxpayers and local governments alike. But most localities don’t issue budget forecasts that look further than a year ahead —making it it easier to put off tough decisions as underlying budget imbalances get bigger and bigger.

THE SOLUTION:

Counties, municipalities and school districts throughout New York State should formally amend their budgeting rules to require long-term financial planning — including spending and revenue forecasts covering at least four future years. These plans should be posted online and made readily available in print form, to ensure to the fullest possible public awareness and engagement in the budgeting process.

The tools for this budgeting reform are readily available to those willing to use them. A multi-year planning guide for local governments has been developed by the state comptroller’s office, which also offers training to local officials in building long-term plans off simple spreadsheet templates. Basic guidelines for long-term financial plans also have been issued by the Government Finance Officers Association (GFOA).

New York City has provided the rest of the state with a strong model of long-term financial planning since its brush with bankruptcy in the 1970s. Other examples are provided by a handful of New York counties and municipalities (including the city of Buffalo and Nassau County) that were forced to begin developing their own long-term plans after running into fiscal problems serious enough to require state control boards.

The danger of short-termism

Imagine driving your car down a rural highway at 65 mph in the steadily gathering dusk of a moonless night—with nothing more to guide you than your parking lights.

That pretty much describes the financial planning approach of most counties, municipalities and school districts across New York State. As of 2011, localities other than New York City spent nearly $76 billion on vital services such as policing, fire protection, road maintenance, sanitation and education. Yet very few issued forecasts of spending and revenues beyond the end of their next fiscal year. As a result, taxpayers can’t see challenges looming just over the horizon.

In a Local Management Guide on multi-year budget planning, the state comptroller’s office explains the pitfalls of failing to take a longer view:

Without planning, fiscally stressed localities sometimes try to limp along from year to year, spending down reserve funds or using various one-time revenues to keep afloat. But the practicality of those strategies is limited. As local governments ranging in size from New York City to Troy have discovered, putting off painful decisions doesn’t make problems disappear—in fact, it usually makes them worse. Financial problems that remain hidden for a long time have a way of emerging suddenly as full-blown financial crises.

As of 2012, only five of New York’s 80 largest counties, municipalities and school districts, other than New York City, issued budgets projecting revenues and expenditures more than a year into the future.* Of that group, only Yonkers is not currently subject to oversight by a state financial control board.**

Some local government and school officials develop long-term projections as an internal planning and management tool, without routinely sharing their projections with the public as part of the annual budget process. In the absence of such information, it is almost impossible to independently evaluate claims by many local governments and school districts that they are approaching their own steep fiscal “cliffs” — although the available evidence suggests they are.

Based on an examination of largely unpublished local fiscal data, state Comptroller Thomas DiNapoli has reported that “more than 100 local governments do not have enough cash on hand to pay even 75 percent of their current liabilities, almost 300 local governments ended either fiscal years 2010, 2011, or both, in a deficit situation, and 27 local governments appear not only to have drained their rainy day funds, but spent more than they had in such reserves.” Similar trends have prompted Education Commissioner John B. King to warn that the state’s most fiscally vulnerable school districts could be at risk of “educational insolvency.”

_______________________________________________________________________________

Albany’s “multi-year” misfire

New York State’s 2005-06 budget—the next to last of Governor George Pataki’s 12-year tenure—included a gubernatorial initiative to replace the state’s previous revenue sharing and unrestricted aid programs with a new program known as Aid and Incentives for Municipalities (AIM), targeted at cities and villages. As its name implied, the new formula was designed to provide these local governments with incentives to improve their financial performance.

The following year, the law was amended to make AIM permanent and link future AIM increases in aid to the filing by each municipality of a “fiscal performance plan,” including:

“… a multi-year financial plan including projected employment levels, projected annual expenditures for personal service, fringe benefits, non-personal services and debt service; appropriate reserve fund amounts; estimated annual revenues including projected property tax rates, the value of the taxable real property and resulting tax levy, annual growth in sales tax and non-property tax revenues, and the proposed use of one-time revenue sources.”

The requirements represented a significant improvement over prior practices, but had two major shortcomings:

1. Multi-year plans were required to be as much backward- as forward-looking, requiring a minimum of “four fiscal years including the municipality’s most recently completed fiscal year, its current fiscal year adopted budget, and the subsequent two fiscal years.” Most municipalities already presented results from the current or prior year, so the net effect was to look just one year beyond the customary fiscal horizon – e.g., to include a projection for 2010 in a 2009 proposed budget.

2. The law required multi-year plans to be filed with the Office of the State Comptroller and the state Division of the Budget – but did not require either state agencies or local authorities to publicize them.

The Legislature tried to address the second problem in a 2008-09 budget provision requiring the posting on municipal websites of multi-year plans and other information localities were required to file as a condition for increases in their aid awards. Unfortunately, the new planning requirement was triggered solely by increases in AIM, assuming state aid would rise every year. That assumption almost immediately proved to be unsustainable. The disclosure requirement effectively has been moot since state fiscal year 2008-09 – the year AIM appropriations peaked before being cut in each of the next three state budgets, and frozen in 2012-13.

Ideally, local governments in New York will move to long-term planning on their own initiative, with or without a renewed increase in state aid. While the last thing localities need is another state mandate, it would be difficult to argue that a statewide requirement for long-term planning would be either unduly costly or burdensome, especially in light of the offsetting benefits.*

* At least one bill introduced early in the Legislature 2013-14 session (A.1446, sponsored by Assemblyman Kenneth Zebrowski, D-Rockland) would require four-year plans of all counties and municipalities, but not school districts.

_______________________________________________________________________________

The case for reform

Both Comptroller DiNapoli and the Board of Regents have advocated multi-year financial planning as a reform that can help local governments and school districts get a better handle on their problems.

So why aren’t more local officials embracing it?

The response boils down to a simple truism: “It’s difficult to predict the future.”

But as New York State, New York City and several other local governments and school districts continue to demonstrate, it is possible to make reasonable assumptions about future trends—and to adjust those assumptions as events warrant.

The largest locally funded item in local and school budgets is employee compensation, which is determined by a combination of staffing levels, local statutes and collective bargaining agreements. Salaries are predictable; even when union contracts have expired or are about to expire, long-term plans can be based on clear assumptions about affordable pay levels. As for health insurance benefits, local budget-makers can draw on their own experience as well as industry and government sources for forecasts of health care cost trends under existing benefit arrangements.

Pensions have been the most difficult spending variable for localities and school districts to predict in recent years. Measured as a percentage of payrolls, pension rates have followed a roller-coaster path since the late 1980s: dropping throughout the 1990s; bottoming out at near zero as of 2000; rising and falling for a few years; and rising very steeply since 2009.

Unlike New York City’s pension actuary, neither the New York State and Local Retirement System (NYSLRS) nor the New York State Teachers’ Retirement System (NYSTRS) issues projections of pension contribution rates more than a year or two in advance. However, in the wake of the pension funds’ investment losses in 2008-09, both systems repeatedly warned employers that costs would rise significantly. NYSLRS pension rates have been accurately predicted by the state Division of the Budget in the state’s own published four-year plans, and the rise in NYSTRS rates was forecast in a 2010 report by the Empire Center.

Property taxes and sales taxes—the main revenue sources for local governments—are much less volatile and difficult to predict than personal income or business taxes, which are important parts of the revenue base for New York State and New York City. Fines and fees, which comprise most other local revenues, are also fairly easy to forecast.

State aid, an important component of many school budgets in particular, can pose more of a long-term forecasting challenge. However, by linking school aid to the rate of growth in personal income, Governor Andrew Cuomo has provided a benchmark for forecasting aid growth in the future. For counties, the largest stream of revenue from Albany consists of Medicaid reimbursements, which have been capped by the state since 2006.

Strict accuracy is not required

Long-term forecasts are not, by themselves, a budgetary fix, but they provide important indicators of a government’s overall fiscal health and vulnerability to future shocks even when they are off-target.

During a series of sustained economic expansions since 1983, revenue forecasts for both the state and New York City consistently proved to be overly pessimistic. Throughout this period, however, the persistence of “out-year” budget shortfalls provided a continuing reminder that the city and state were spending at levels that could not possibly be sustained when revenue growth slowed down. In the absence of long-term plans, history suggests both the city and state would have dug themselves into even deeper holes before revenues plummeted after the recession hit in late 2007.

Buffalo’s move to comprehensive four-year financial planning, which began in 2003, has been described by the Buffalo Fiscal Stability Authority as “one of the most critical components” of that city’s fiscal recovery. Long-term planning, the authority says, has helped the city “address structural budget gaps as well as to recognize and prepare for future fiscal challenges.” While Buffalo is by no means free of fiscal pressures, it is in far better shape than it was earlier in the decade. And in contrast to other fiscally troubled upstate cities, Buffalo has clearly defined future challenges in dollars and cents terms.

Likewise, Nassau County’s move to a four-year planning process (now enshrined in a charter provision) after a financial control period beginning in 2000 did not prevent a fiscal crisis relapse, which led a state Interim Finance Authority to reassert ultimate control of the county budget in 2011. However, as in Buffalo’s case, long-term financial planning in Nassau County at least has highlighted an unsustainable structural budget gap and made it more difficult for local officials to avoid tough decisions.

The city of Yonkers was last under state fiscal control in the 1980s, but its growing budget imbalances led newly elected Mayor Mike Spano to voluntarily embrace long-term financial planning for his city in 2012. His initial four-year plan, indicating the city faces budget gaps growing from 9 to 19 percent of revenues between 2014 and 2016, has called public attention to the need for tighter control of city spending.

What is the optimal plan length? New York City issues five-year plans – for example, forecasting revenues and spending out to fiscal 2017 under the budget approved in June 2012. The city’s plan must be updated quarterly and balanced according to Generally Accepted Accounting Principles (GAAP), which allows for far less gimmickry than the checkbook-style “cash” accounting used in most local and school district budgets.

However, for localities now budgeting on a cash basis, a move to GAAP accounting is by no means essential. Properly implemented, long-term planning will at least make it easier for independent analysts and taxpayers to spot the kinds of financial gimmicks that cash accounting permits.

As for plan duration, the GFOA recommends five years, which is generally regarded as the outer limit of a realistic forecasting horizon. The minimum recommended period, as reflected in the template developed by the state comptroller’s office, would be four years, including the upcoming fiscal year.

Template for reform

A useful long-term plan includes most of the same information provided in an annual budget – but projected further into the future.

Many counties, municipalities and school districts already provide multi-year projections of future funding needs for capital purposes only – for example, park facilities, building renovations and road reconstruction financed in part by borrowing. But what they need is a long-term financial plan including projections of both revenues and expenditures – for all public funds, capital and operating.

The plan should begin with a summary of revenues, expenditures and surpluses or deficits for each year of the plan, as outlined in a useful template is developed by the state comptroller’s office (see Appendix). As recommended by the comptroller, it should cover not only the budget’s catch-all general fund, but also separate operating funds that many municipalities have created for water, sewer and other services, as well as capital funds. And beyond the summary level, the plan should break down the summary into the same categorical details presented in annual budgets, along with current and projected employment levels and other useful information now presented in many current budgets with shorter time horizons.

However, the comptroller’s falls short in failing to recommend the disaggregation of past, present and projected employee benefits into their major constituent elements of pensions, health insurance and other fringe benefits. Such a breakdown—including separate amounts for health coverage of active and retired employees—should be regarded as an essential element of any county, municipal or school district financial plan. Otherwise, local elected officials and taxpayers will not fully understand the factors that are driving future expenses; in particular, they may continue to overlook the growing expense of retiree healthcare obligations, over which they might be able exercise more direct control.

GFOA, to which most local budget and finance officials belong, says long-term financial planning should be treated as an “inclusive” process, “involving elected officials, staff, and the public.” In its own guide to the issue, GFOA adds:

Inclusiveness is important because a viable long-term financial plan must satisfy two requirements that can at times be difficult to reconcile. First, the plan must result in strategies to achieve and maintain financial sustainability. Second, the plan must identify how the government will provide a consistent level of services and address issues of major concern to the community within financial constraints.

Forging a plan that will gain the support of elected officials, staff, and the public is critical for successful implementation. It requires reaching out to stakeholders inside and outside the government and a rigorous technical analysis.

CONCLUSION

Long-term financial plans are not binding commitments. They are guidance documents, reflecting where a government is headed if current, reasonably foreseeable trends continue. By showing where and when revenues diverge significantly from expenditures, long-term plans provide an early warning of potential trouble ahead, giving local leaders time to make adjustments.

Long-term planning won’t, by itself, solve fiscal problems or guarantee better results. However, by requiring local officials to consider the long-term impacts of their short-term decisions, it will promote more responsible fiscal behavior. Beyond the numbers, it can also provide a vehicle for establishing performance goals and objectives, and for measuring a government’s progress in meeting them.

— by E.J. McMahon, Senior Fellow

_______________________________________________________________________________

ENDNOTES

*Two of the state’s largest and highest-spending towns, Babylon and Ramapo, do not even post their annual budgets online. Ramapo’s town clerk says his town budget is available in digital form to “those who request it,” while Babylon’s clerk insists on a written Freedom of Information Law request.

**Rockland County has a law requiring its county executive to submit five-year budget projections to the County Legislature, but the Legislature does not post the numbers on its website.

BIBLIOGRAPHY

Local Performance Management Guide on Multiyear Financial Planning, Office of the State Comptroller, http://www.osc.state.ny.us/localgov/pubs/lgmg/multiyear.pdf

Long-Term Financial Planning for Governments, Government Finance Officers Association, www.gfoa.org

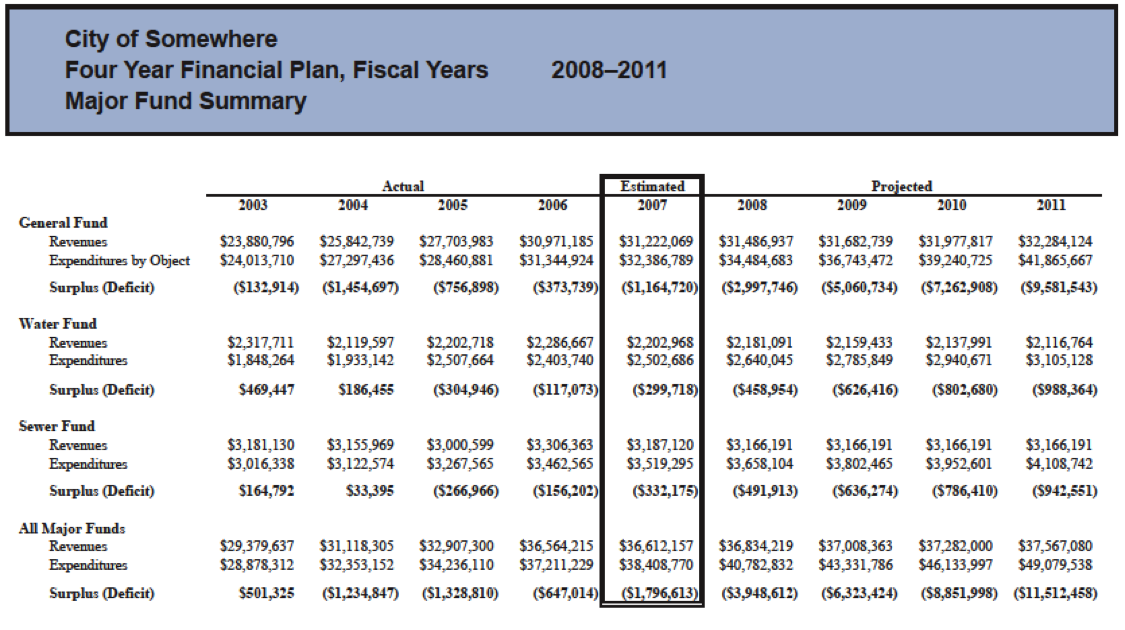

APPENDIX

State Comptroller’s Sample Summary Plan

You may also like

34 MTA Workers Made $200K+ In Overtime In 2025

Thirty-four employees of the Metropolitan Transportation Authority (MTA) received more than $200,000 in overtime payments in 2025, as total annual pay surpassed half a million dollars for some, according to , the Empire Center’s governm Read More

Overtime on State Payroll Jumps 21%

104 employees made over $500k in 2025 total annual pay.

2,450 employees were paid more than Gov. Kathy Hochul's Read More

Seven Reasons Not To Raise Taxes in New York

Despite the robust growth of state revenues in recent years, many of New York's elected officials are pushing to further increase the tax burden on the state's residents and businesses.

Read More

Ninety New York Educators Receive $300k+ in Annual Pay

Ninety employees from New York’s school districts (outside New York City) received more than $300,000 during fiscal year 2025, according to , the Empire Center’s transparency website.

The public educator pay data are based on salary information rep Read More

NYC Employees Receive $300k+ in Overtime

Two New York City employees received more than $300,000 in overtime payouts, according to fiscal year 2025 , the Empire Center’s government transparency website. The city paid a total of $2.9 billion in overtime during fiscal year 2025. Read More

State Lawmakers Spend $268 Million on Legislative Operations

Spending by state lawmakers on office personnel and administrative costs varies widely, with some paying out nearly twice as much as others on their office operations, according to the most recent reported, posted to SeeThroughNY.net.

Read More

School Districts Plan To Spend Over $35K Per Student, Outpacing Inflation

School districts presenting budgets to voters on Tuesday, May 20, plan to spend an average of $35,012 per student, up 4.6 percent from the current school year, according to new state data.

Data collected by the state Education Departme Read More

Overtime on State Payroll Surges 11%

Twenty-three New York State employees collected over $200,000 each in overtime, according to posted today on SeeThroughNY, the Empire Center’s government transparency website. Read More