Testimony of Edmund J. McMahon

Founding Senior Fellow, Empire Center for Public Policy

Before the Joint Legislative Fiscal Committees

February 9, 2023

New York’s tax coffers have swelled to overflowing in the past two years, producing record surpluses and budgetary reserves. This surge, the opposite of what was expected when the Covid-19 pandemic began in March 2020, is the direct result of our dependence on a steeply progressive state personal income tax. New York’s revenues quickly recovered from the pandemic because the state government does, in fact, “tax the rich” to a far greater extent than almost any other state. However, there are clear signs that the state’s heavy reliance on its highest earners, already at record levels before 2020, is both unstable and unsustainable.

Governor Hochul began this year’s legislative session by declaring that she would not propose any further increase in personal income taxes. But standing pat is not enough. As reviewed in this testimony, even as New York’s income tax revenues surged, its income tax base was eroding. This trend began before 2020 and got worse during the pandemic.

To slow down if not reverse the erosion before it’s too late, the next budget should include provisions designed to reverse the historically large tax increase enacted on top earners two years ago, which is otherwise scheduled to expire all at once at the end of tax year 2027.

A top-heavy tax structure

New York’s personal income tax code has long been among the most progressive of any state’s, placing a much heavier burden on high incomes than low- or moderate-income households.1 In 2020, the highest-earning one percent of New Yorkers reported 32 percent of adjusted gross income but paid 46 percent of income taxes collected from full-year state residents, as shown in Appendix Figure 1. And as shown in Appendix Figure 2, even prior to the most recent increases for top earners and cuts in lower brackets, the effective tax rate paid by the highest-earning one percent of all New Yorkers was more than double the rate paid by middle-income filers.

The state raised marginal tax rates further in 2021, as part of the changes enacted with the FY 2022 state budget. As detailed in Appendix Table 1, the personal income tax changes added three new brackets on incomes starting just above $2 million for married joint return filers (or $1 million for singles), translating into higher tax payments of nine percent to 24 percent. For New York City residents, the combined rates on millionaire incomes are now the highest in the country, exceeding California’s statewide rate of 13.3 percent.

New York’s higher income tax rates, originally projected to generate $4 billion a year in added revenue by 2025, are scheduled to expire in 2027. The FY 2022 revenue bill also eliminated the 2024 sunset on the repeatedly extended “millionaire tax” hike of 2011, making it permanent. This change by itself constituted New York’s most significant permanent-law income tax increase since the 1960s.

The state financial plan assumes that high-income households will remain literally and figuratively unmoved by the most significant hike in marginal rates since the early 1970s. In fact, however, between 2010 and 2020, Internal Revenue Service data show New York’s share of the nation’s millionaire earners decreased from 12.7 percent to 8.9 percent, the lowest level on record.2

State personal income tax data from the first tax year affected by the pandemic disruption indicate that New York was continuing to lose high earners in the wake of the March 2020 Covid-19 outbreak.3 In 2020, the state’s personal income tax base included 54,824 full-time New York residents with incomes of $1 million or more, which was down slightly from the 2019 total of 55,308. During the same period, the number of full-year nonresident and part-year resident New York taxpayers rose from 70,222 to 73,899 filers in the $1 million-and-up bracket.4 Millionaire earners living in Florida accounted for the largest share of new full-year nonresident filers; there were 7,218 Floridians who owed some New York income tax in 2020, compared to 6,471 in the previous year.

Despite the continuing decline in the number of high-earning New York residents, the Empire State’s personal income tax collections rose a healthy $1.3 billion, or 2.4 percent, in the fiscal year ending March 31, 2021. The higher-than-expected tax revenues were due mainly to the unexpectedly strong recovery of stock prices in the second half of 2021, which boosted the capital gains component of New York’s income tax base to $132 billion—up 58 percent from the previous year to a new all-time high, exceeding the previous record set in 2007. The increased net capital gains of New York’s income millionaires generated at least $3 billion in added state tax revenue, more than making up for the decline in total taxes paid by lower-earning households.

Capital gains rose again in 2022, to a new all-time high of $203 billion—a record 18 percent of total adjusted gross income reported by New York taxpayers. But investment income is highly volatile. With the S&P 500 down 15 percent since early 2022, the Executive Budget estimates that capital gains dropped 10 percent last year and will fall another 10 percent in 2023. Across two fiscal years, those decreases translate into a revenue decline of at least $3 billion.

Meanwhile, thanks in large part to a record large bonus pool, the securities industry share of total state revenues rose to a record 22 percent, the state comptroller’s office reports. Since this data series began in the late 1990s, spikes in Wall Street-originating tax revenues have always been followed by steep decreases in this category.

The pinch of SALT

The impact of state tax increases in high-income brackets has been compounded by the $10,000 cap on federal deductions for state and local taxes (SALT), enacted as part of the Tax Cuts and Jobs Act (TCJA), which took effect in 2018. Despite New York’s higher average SALT deductions under previous law, the other major provisions of the TCJA resulted in net tax cuts for most New York taxpayers, including a majority of middle-income residents who previously could claim a SALT deduction for their high property taxes. The negative impact of the SALT cap is overwhelmingly concentrated among New York’s highest earners—especially those with incomes topping $1 million a year, nearly 30 percent of whom paid higher taxes under the new federal law.5

For taxpayers claiming it, the pre-2018 SALT deduction functioned as a discount, reducing the effective impact of the statutory state and local rate. In 2011-17, for example, the SALT cap reduced New York’s top rate from 8.82 percent to 5.3 percent. Even in the early 1970s, when the state’s top income tax rate was 15.35 percent, its effective cost was just 4.6 percent. With no federal deduction, the state’s current top rate on the same earners ranges from 9.65 percent to 10.9 percent, by far the highest effective rates in New York’s history.

The state has sought with a series of workarounds to preserve the deduction for at least some taxpayers. The most significant by far has been the Pass-Through Entity Tax, or PTET, created by the FY 2022 budget, which effectively allows owners of many closely held businesses to claim federal tax deductions and state tax credits for net profits that “pass through” to them as taxable personal income. But the PTET has obscured the underlying trend in personal income tax receipts, for which the new tax effectively substituted.

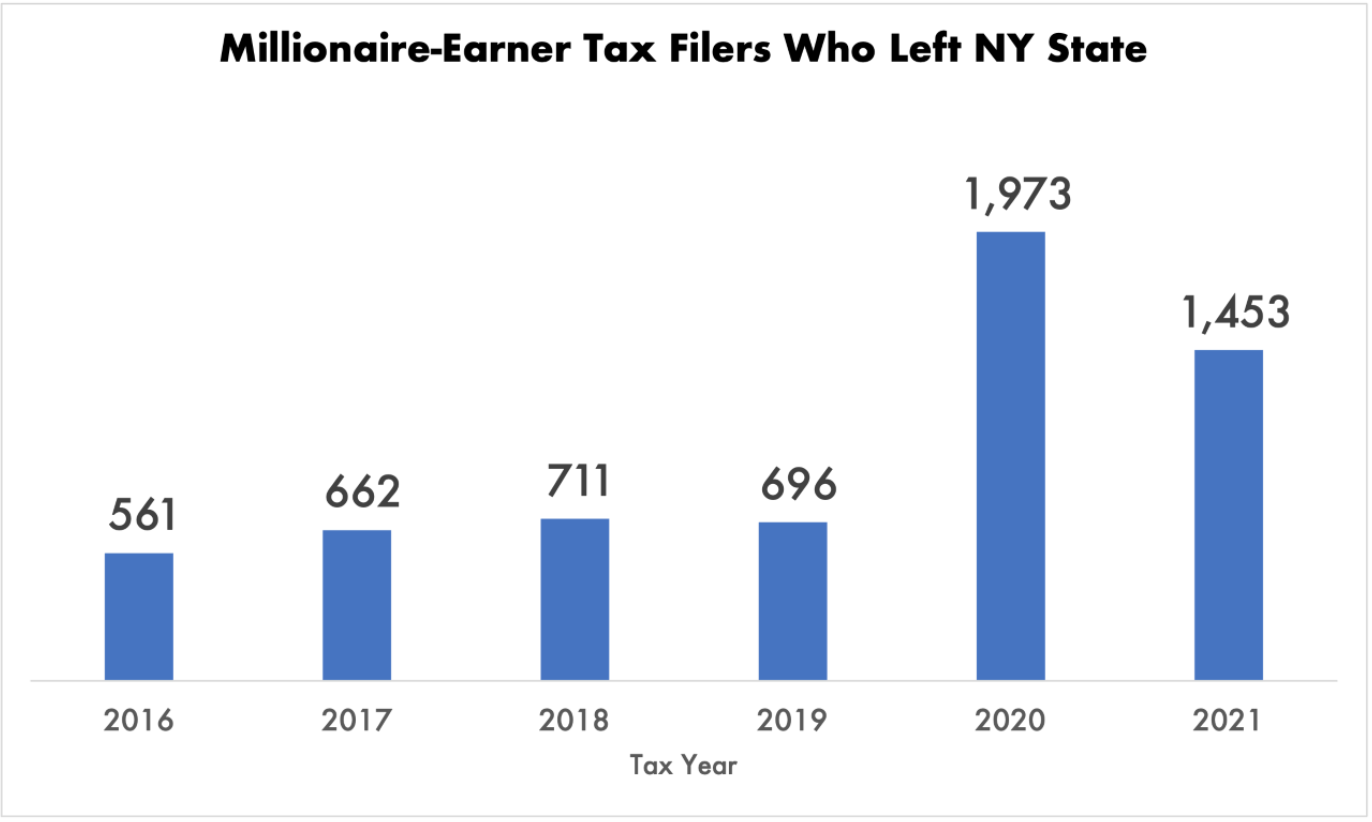

Newly posted data from the state Department of Taxation and Finance dramatically highlight the risks of maintaining historically high state income tax rates. Between 2016 through 2019, the data show, the number of filers with New York source income of $1 million or more ranged from 561 to 711 a year (see Appendix Figure 3).

In 2020, according to the same state data, income millionaire out-migration surged to a loss of 1,973 filers. The number dropped slightly in 2021, to a still-elevated level of 1,453 out-migrant income millionaires. But as the data also show, this decline was concentrated among filers with incomes below $25 million (see Appendix Figure 4). Notably, out-migration by New Yorkers earning more than $25 million rose again, from less than 6 percent in 2020 to just over 8 percent in 2021— the same year their New York State tax rates were increased by 24 percent.

It is impossible to look at these data and conclude that mega-earners are oblivious to higher taxes. If anything, the trends suggest the centrifugal impact of the pandemic has accelerated an existing out-migration trend among income millionaires. To repeat: viewed in a national context, New York’s share of top earners was dropping prior to the pandemic and began dropping faster in the first year affected by the Covid-19 outbreak. This is a danger signal the Legislature must heed.

Under current law, the higher rates imposed in 2021 are supposed to sunset at the end of 2027. In reality, if the state remains on its current course, the 2021 tax rates will be extended indefinitely—and raised even higher at the first sign of a revenue shortfall. High earners, and their tax advisers, can read these tea leaves as well as anyone.

Instead of simply avoiding further personal income tax hikes, the Legislature should assign a priority to phasing out the 2021 tax increases in four equal increments, starting in tax year 2024. Advertising a clear intent to return to a more competitive tax climate should discourage at least some high earners from making relocation decisions now that will more severely undermine our tax base before the end of this decade.

Beyond undoing the damage of 2021, the Legislature should also adopt a schedule for continuing to ratchet back the top income tax rate to the 6.85 percent level of the late 1990s—only slightly below the 7 percent top rate adopted by Governor Mario Cuomo and bipartisan legislative majorities in New York’s landmark 1987 tax reform law.

To offset a portion of the revenue impact from reversing broad-based tax hikes, it’s time the Legislature finally eliminated the single largest tax giveaway in our tax code. I’m referring to the Film Tax Credit. By far the largest of its kind, the credit costs us $420 million a year, a total of more than $5 billion over the past 16 years, despite the absence of any evidence that it comes close to paying for itself. Repeal of the credit was recommended by a gubernatorial tax reform commission a decade ago. Since then, the arguments for the credit have, if anything, grown even weaker.

Governor Hochul inexplicably has proposed increasing the tax credit to $700 million and extending it to the early 2030s. The Legislature should instead reject this proposal and direct the administration to shut the tax credit window for all planned productions that have yet to be guaranteed a subsidy.

APPENDIX

Figure 1

Figure 2

Table 1

Figure 3

Source: Department of Taxation & Finance, “Tax Facts” at https://www.tax.ny.gov/data/stats/tax-facts.htm#expanded-content-menu2

Figure 4

Source: Department of Taxation & Finance, “Tax Facts” at https://www.tax.ny.gov/data/stats/tax-facts.htm#expanded-content-menu2

ENDNOTES

1 Frank Sammartino and Norton Francis, “Federal-State Income Tax Progressivity,” Tax Policy Center, June 2016. https://www.taxpolicycenter.org/sites/default/files/publication/131621/2000847-federal-state-income-tax-progressivity.pdf

2 E.J. McMahon, “New York lost more high-earning taxpayers in pandemic-wracked 2020,” Dec. 19, 2022, post at https://www.empirecenter.org/publications/new-york-lost-more-high-earning-taxpayers-in-pandemic-wracked-2020/

3 NYS Department of Taxation and Finance, Personal income tax summary datasets through tax year 2020, https://www.tax.ny.gov/research/stats/statistics/pit-filers-summary-datasets-beginning-tax-year-2015.htm

4 Nonresidents must pay New York income tax on any wage, salary or net profits earned from work or business activity in the Empire State, but not on capital gains and other investment- and savings-related income.

5 See summary of Empire Center analysis on the SALT cap’s impact in New York, “The SALT Story: Washing Away the Brine,” at https://www.empirecenter.org/salt/

You may also like

Testimony of Bill Hammond on Medicaid’s Consumer Directed Personal Assistance Program

Testimony of Bill Hammond

Senior Fellow, Empire Center for Public Policy

Before the U.S. Congress Joint Economic Committee

Read More

Testimony of Zilvinas Silenas on FY 2027 New York State Executive Budget Revenue Article VII Legislation, part K

Testimony of Zilvinas Silenas

President, Empire Center for Public Policy

Before the Joint Legislative Fiscal Committees,

on FY 2027 New York State Executive Budget Revenue Article VII Legislation Read More

Testimony of Bill Hammond on the Health and Medicaid Budget for FY 2027

Testimony of Bill Hammond

Senior Fellow, Empire Center for Public Policy

Before the Joint Legislative Fiscal Committees

February 10, 2026

Medicaid Read More

Testimony on FY 2027 New York state executive budget Article VII legislation, parts N, O, P

Testimony of Zilvinas Silenas

President, Empire Center for Public Policy

Read More

Testimony of Bill Hammond on the Health and Medicaid Budget for FY 2026

Testimony of Bill Hammond

Senior Fellow for Health Policy, Empire Center for Public Policy

Before the Joint Legislative Fiscal Committees

February 11, 2025

Read More

Foundation Aid Study Testimony

https://www.youtube.com/watch?v=bmhFZr5ftxs

FULL WRITTEN TESTIMONY:

Thank you for the opportunity to provide feedback on the Foundation Aid Formula. As a parent of New York City schoolchildren, the Vice President Read More

Statement to the New York City Charter Revision Commission

Empire Center founding senior fellow E.J. McMahon showed the New York City Charter Revision Commission how the charter can be improved to better protect the public fisc. Read More

Testimony of Bill Hammond Before the Joint Legislative Fiscal Committees

Testimony of Bill Hammond

Senior Fellow for Health Policy, Empire Center for Public Policy

Before the Joint Legislative Fiscal Committees

January 23, 2024

Read More