Presented to the Joint Legislative Fiscal Committees

February 12, 2019

Governor Cuomo’s Executive Budget for fiscal year 2020 includes a short list of state revenue actions. By far the most significant tax proposal on the list would extend, for five years, the temporary added personal income tax (PIT) rate also known as the “millionaire tax.”

The effective tax burden imposed by the PIT, the state budget’s largest single revenue source, has been significantly increased by the new federal tax law, not least by the cap on deductions for state and local taxes, or (SALT). Just last week we heard Governor Cuomo blame the tax law and the SALT cap for an unexpected decline of $2.3 billion in personal income tax receipts.

Several points to keep in mind:

- Despite New York’s higher average SALT deductions under previous law, the major individual income tax provisions enacted by Congress in 2017 will produce a tax cut for at least 61 percent of New York taxpayers, with the cuts averaging $2,400—compared to 65 percent and $2,180 nationally.Even those who previously itemized will see offsetting benefits from lower federal tax rates, a doubling of the standard deduction, expanded child credits, and the partial rollback of the Alternative Minimum Tax. Only 8.3 percent of New York taxpayers will pay more, with the increases averaging $3,340—compared to 6.3 percent and average an average increase of $1,630 nationally.

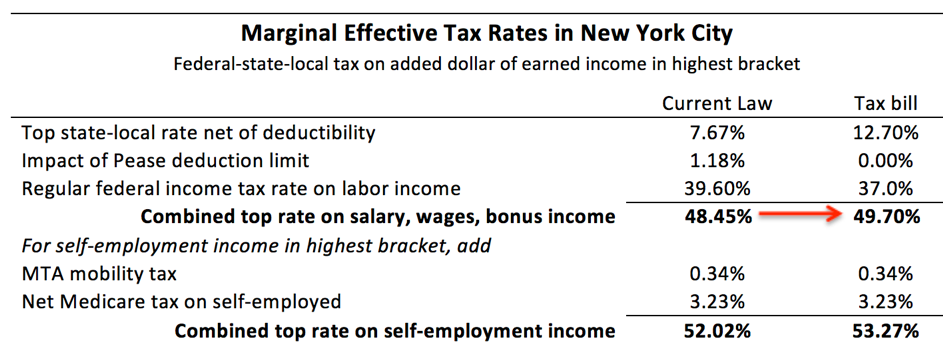

- The negative impact of the SALT cap is concentrated among New York’s highest earners—especially those with incomes topping $1 million a year, nearly 30 percent of whom will pay highertaxes under the new law. Despite a cut in the top federal rate, top- bracket taxpayers living in New York City now face a higher combined federal-state-city marginal tax rate than they did under previous law, as shown in Table 1.

- New York is exceptionally reliant on a small number of high-earning taxpayers most likely to face higher taxes due to the SALT cap. As repeatedly pointed out by the Assembly Majority Ways & Means staff in past reports, high-earning individuals are an “inherently unstable,” “volatile” and “unsustainable” revenue source, because they depend on investment income for a larger share of their incomes. In fact, it’s highly likely that market volatility affecting higher-bracket capital gains income played a role in the state’s current revenue shortfall, which followed a sharp drop in stock prices in the fourth quarter of 2018.

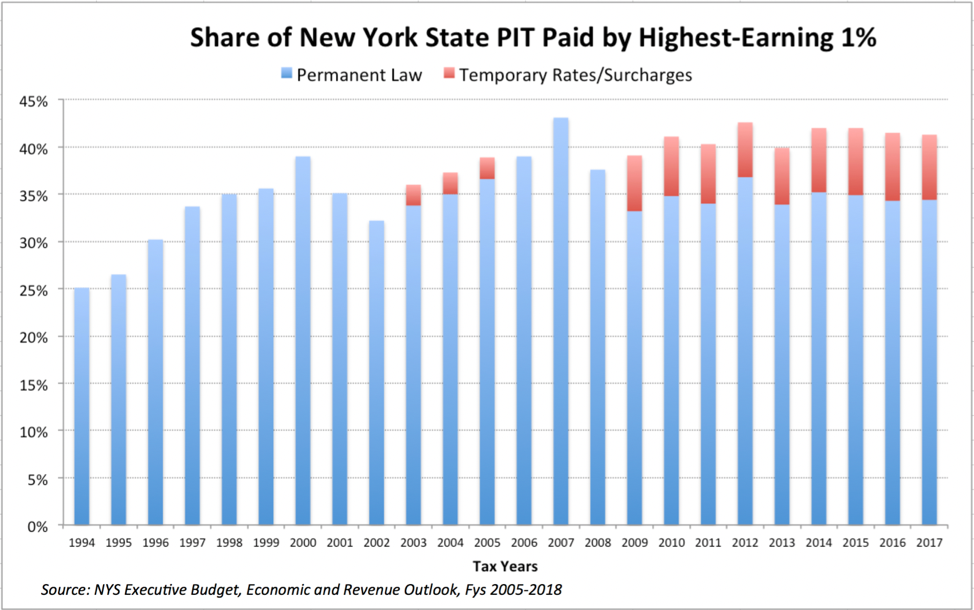

The share of New York income taxes generated by the highest-earning 1 percent has jumped significantly over the past 20 years. In recent years, it’s averaged roughly 40 percent of total personal income tax liability, up from 25 percent in 1994, Mario Cuomo’s last year as governor, as shown in Figure 1. Among state residents alone, the top 1 percent accounts for 46 percent of tax liability, according to the governor.

The New York State personal income tax turns 100 this year. Through the PIT’s first 99 years of existence, the net marginal cost of the tax was offset to a significant degree by full deductibility on federal tax returns. Now, however, the SALT cap has laid bare an enormous competitive tax gap between New York and many other states.

Figure 2 illustrates the effective combined top rate of income tax for New York City residents during the 50 years following the city income tax in 1967. As shown, the effective state and city rate, net of federal deductibility, was already near an all-time high before the new federal law was enacted. Under the new federal law, the net-of-deductibility state and city tax rate for high earners is nearly 13 percent—second highest in the country.

Residents in the highest New York personal income tax brackets now have a much stronger financial incentive to consider relocating to states and cities with lower taxes—by no means limited to Florida. For example, neighboring Massachusetts offers much lower property taxes and a higher-rated overall business tax climate than New York’s, including a flat income tax rate that just decreased to 5.05 percent (and is scheduled to drop next year to 5 percent).

It wouldn’t take an exodus of high earners to put a dent in New York’s revenues. Even a small degree of out-migration within the top 0.1 percent “tippy top” of the income pyramid would have a noticeable impact.

Consider: in 2016, there were 2,149 resident New York households with adjusted gross incomes of more than $10 million, who owed $5.3 billion in state income tax. Those taxpayers had average gross income of $31 million and average New York PIT liability of $2.5 million. Let’s assume the average is boosted by a few super-high earning households, and that median income for this group is actually $15 million. If we lost just 10 percent of those median earners in the highest reported category—just 215 tax filers, or enough people to fill an average movie theater—the state would lose $265 million in tax revenue. That’s more than the entire state- funded budget of the Department of Environmental Conservation.

There is indirect evidence that a portion of the high end already has been shrinking in relative terms, like a melting glacier. The resident share of millionaire earners in New York’s PIT base has been getting smaller since 2000, including decreases every year since 2008, as shown in Figure 3. The steepest drop in the resident payer category has been among those with incomes of $10 million or more, where the resident share was just 39 percent as of 2016. Nonresidents don’t pay New York taxes on their capital gains and dividends, or wages and salaries earned outside New York, and so their effective New York income tax rates are much lower.

Governor Cuomo has begun calling urgent attention to the state’s heavy reliance on the top 1 percent and to the risk that more high earners will move in response to the SALT cap. Unfortunately, his budget heads in a contradictory direction by extending the millionaire tax.

In another move that would run counter to Governor Cuomo’s warning against raising taxes on high earners, the governor has revived his 2018 proposal to impose an enormous state tax penalty on a particular type of income, known as “carried interest,” commonly collected by managers of private equity and hedge funds. Part Y of the revenue bill would recharacterize carried interest as taxable New York source income from a trade or business, and further subject that income to a 17 percent “fee.” Implicitly acknowledging the likely taxpayer response to a 200 percent tax increase, the bill would not take effect unless similar legislation is adopted by the neighboring states of Connecticut, Pennsylvania, Massachusetts and New Jersey.

The governor’s bill memo does not include a revenue estimate for the carried interest proposal, and the Executive Budget financial plan apparently does not anticipate its adoption. But you don’t have to support the federal tax treatment of carried interest to spot the problem with even considering such a punitive proposal on a state level.

This proposal is essentially designed to stigmatize some of the most highly paid taxpayers in New York, a relatively small group of people who collectively pay hundreds of millions of dollars a year into the state treasury. No highly portable industry can be expected to sit still for a targeted 200 percent tax increase.

In light of the structural issues I’ve cited here, the Legislature should:

- Reject the governor’s proposal for a five-year extension of the full 8.82 percent millionaire tax, and instead schedule a phased-in, multi-year reduction of the tax with the goal of returning it to the permanent-law 6.85 percent level.

- Reject the proposed carried-interest tax penalty.

- As assumed in the financial plan, continue to phase in already scheduled personal income tax reductions for middle- and upper-middle-income brackets, enacted in 2016 and due for full implementation in 2025.

In addition, the Legislature should consider:

- Recoupling the Empire Child Credit to the increased level and expanded income limits for the federal Child Credit, which would raise the maximum credit to $666. The $500 million cost of this change can be covered by eliminating another state tax break that was supposedly intended to help working families but is far less effectively targeted: the sales tax exemption on clothing purchases under $110.

- Beginning a long-term rollback of the New York Estate Tax, starting with the tax rate “cliff” inadvertently created by the 2014 reform of the law.

One final recommendation tied to the state budget deals with an issue of overriding important to local taxpayers. Part G of the governor’s Public Protection and General Government Article 7 revenue bill includes a provision making permanent the state cap on local property tax levies, which has been a temporary provision of the rent regulation law since 2011.

The case for a permanent cap—with no added exclusions or loopholes— is clear and overwhelming. The tax cap has been working, property owners billions of dollars year. The new federal tax law makes this restraint more important and valuable than ever.

The bottom line: do not delay. Make the tax cap permanent as soon as possible.

APPENDIX to E.J. McMahon Testimony

Before the Joint Legislative Fiscal Committees February 12, 2019

Table 1

Figure 1

Figure 2

Figure 3

You may also like

Testimony of Bill Hammond on Medicaid’s Consumer Directed Personal Assistance Program

Testimony of Bill Hammond

Senior Fellow, Empire Center for Public Policy

Before the U.S. Congress Joint Economic Committee

Read More

Testimony of Zilvinas Silenas on FY 2027 New York State Executive Budget Revenue Article VII Legislation, part K

Testimony of Zilvinas Silenas

President, Empire Center for Public Policy

Before the Joint Legislative Fiscal Committees,

on FY 2027 New York State Executive Budget Revenue Article VII Legislation Read More

Testimony of Bill Hammond on the Health and Medicaid Budget for FY 2027

Testimony of Bill Hammond

Senior Fellow, Empire Center for Public Policy

Before the Joint Legislative Fiscal Committees

February 10, 2026

Medicaid Read More

Testimony on FY 2027 New York state executive budget Article VII legislation, parts N, O, P

Testimony of Zilvinas Silenas

President, Empire Center for Public Policy

Read More

Testimony of Bill Hammond on the Health and Medicaid Budget for FY 2026

Testimony of Bill Hammond

Senior Fellow for Health Policy, Empire Center for Public Policy

Before the Joint Legislative Fiscal Committees

February 11, 2025

Read More

Foundation Aid Study Testimony

https://www.youtube.com/watch?v=bmhFZr5ftxs

FULL WRITTEN TESTIMONY:

Thank you for the opportunity to provide feedback on the Foundation Aid Formula. As a parent of New York City schoolchildren, the Vice President Read More

Statement to the New York City Charter Revision Commission

Empire Center founding senior fellow E.J. McMahon showed the New York City Charter Revision Commission how the charter can be improved to better protect the public fisc. Read More

Testimony of Bill Hammond Before the Joint Legislative Fiscal Committees

Testimony of Bill Hammond

Senior Fellow for Health Policy, Empire Center for Public Policy

Before the Joint Legislative Fiscal Committees

January 23, 2024

Read More