Key Takeaways

- The Tier 5 and Tier 6 changes combined are saving New York state and local governments outside New York City more than $1 billion this year.

- After record-busting investment returns in 2021, most of the state’s public pension plans report they are fully funded—but adjusting for financial risk, their combined unfunded liabilities still total nearly $400 billion.

- The traditional defined-benefit pension system remains biased in favor of career and long-term employees, to the disadvantage of those who work shorter government careers.

New York taxpayers have been hit with enormous increases in pension costs for state and local government employees over the past 20 years. From less than $1 billion in 2000, combined annual employer contributions to the Empire State’s public pension funds escalated to nearly $10 billion by 2010, peaking at nearly $17 billion in 2015. Contributions have leveled off at roughly $16 billion in recent years—but under lenient government accounting standards, even that figure conceals the full long-term cost of generous, locked-in pension benefits for generations of retired government employees.

New York’s pension bomb had already exploded a dozen years ago when state officials belatedly started responding to the problem by scaling back pension entitlements for newly hired employees. The first modified pension plan, Tier 5, took effect under Governor David Paterson in 2010. The second and more significant piece of legislation, establishing Tier 6, was successfully pushed by Governor Andrew Cuomo in 2012.

Approaching the 10th anniversary of Tier 6, this report looks back on what New York’s pension reforms accomplished—and failed to accomplish—and identifies further reforms needed to create a 21st century public pension system that fairly balances the interests of taxpayers and employees.

Among the key findings reviewed in these pages:

- The Tier 5 and Tier 6 changes combined are saving New York state and local governments outside New York City more than $1 billion this year, reducing total employer contributions by about 15 percent compared to what would have been billed to cover workers under previous plans.

- After record-busting investment returns in 2021, most of the state’s public pension plans report they are fully funded—but adjusting for financial risk, their combined unfunded liabilities still total nearly $400 billion. This much hasn’t changed: any future shortfall must be made up by taxpayers.

- The traditional defined-benefit pension system remains biased in favor of career and long-term employees, to the disadvantage of those who work shorter government careers. Public school teachers, in particular, are poorly served by the current system. Fewer than half of all teachers will earn as much or more in retirement benefits as is contributed on their behalf to the state teachers’ retirement system.

Key recommended reforms arising from the findings:

- Open the Tier 6 Voluntary Defined Contribution plan—now available to a limited number of non-union, appointed and elected officials—to all public school teachers.

- Follow the lead of the federal government by creating new defined-contribution and “hybrid” pension plans for state employees and give local governments the option of offering these choices to their employees.

- Mandate truth-in-accounting standards for New York pension funds, as recommended for all government plans by the Society of Actuaries.

BACKGROUND

Nearly all of New York’s 1.3 million state and local government employees belong to defined benefit (DB) pension plans, which guarantee a stream of post-retirement income based on peak average salaries and career duration. Pension benefits are financed by large investment pools replenished primarily by tax-funded employer contributions, calculated as a percentage of total covered payrolls. Pension payments to New York state and local retirees and their beneficiaries are exempt from state personal income tax and guaranteed by the state Constitution.

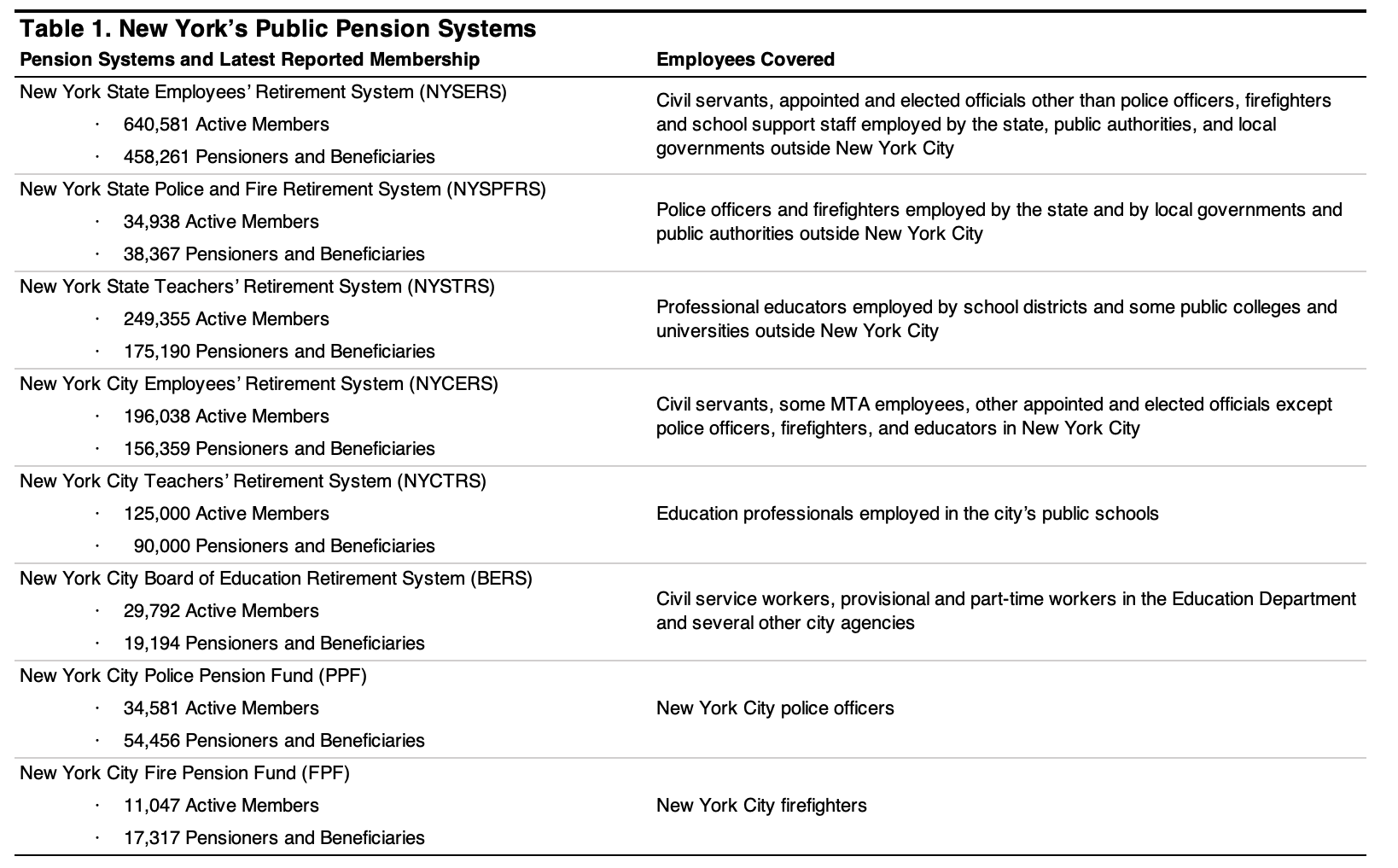

While some states have hundreds of local pension plans, New York’s system is more concentrated and centralized than most, consisting of eight separate retirement systems falling into three groups, as summarized in Table 1.

Source: Pension system annual financial reports

With $268 billion in assets as of June 30, 2021, the New York State and Local Retirement System (NYSLRS) is the nation’s third largest public pension plan, exceeded only by California’s public employee (CalPERS) and teacher (CalSTRS) retirement systems. The five New York City retirement systems collectively rank just behind NYSLRS, with combined assets of $266 billion. The New York State Teachers Retirement System (NYSTRS) is the nation’s sixth largest plan, with $149 billion in assets.

Like most of their counterparts across the country, New York’s public pension plans offer generous benefits, typically ranging from 50 to 75 percent of final average salaries for career government employees, with early retirement penalties. State and local employees in New York also belong to the federal Social Security system (supported by combined employer and employee payroll taxes), whose benefits can raise their annual post-retirement incomes to more than 100 percent of pre-retirement earnings.

NY’S LEGAL LOCK ON PENSION FUNDING AND BENEFITS

Even before a nationwide pension crisis mushroomed in the early 2000s, some states had dug themselves into deeper financial holes by delaying or deferring required employer pension contributions, or by issuing “pension bonds” premised on steady record stock market gains. In extreme cases, most notably of New Jersey and Illinois, state pension funds flirted with insolvency after their already depleted assets were further drained by the Great Recession.

New York was prevented from replicating underfunding abuses in other states by Article 5, Section 7 of New York’s Constitution, which guarantees that pension benefits shall not be “diminished or impaired.” In the landmark 1993 decision in McDermott v. Regan, the state Court of Appeals blocked an attempt by the Legislature to adopt an alternative pension funding method that would “deplete moneys in the existing pension fund by reducing the amount of employer contributions.”1

The constitutional provision also has long been interpreted to mean that increases in pension benefits, once granted, cannot be reversed—only changed for employees in subsequent retirement tiers. As a result, New York government workers benefitted from what a leading commentator on retirement finances has called the “public pension straddle option,” which allowed workers to collect bigger benefits financed by excess investment gains in the 1980s and 90s, while forcing taxpayers to cover subsequent pension fund investment losses.2

New York’s DB plans have two principal shortcomings: they expose taxpayers to open-ended financial risk, and their benefit structures are deliberately biased in favor of long-term and full-career government workers—generally those with at least 20 to 25 years of service credit. Employees who fail to reach the 10-year vesting point receive no pension, and benefits accrue at lower rates for those who devote less than half their careers to government service.

In the private sector, DB pensions have been largely replaced by the defined contribution (DC) model, such as 401(k) accounts, supported by a combination of pretax employer and employee contributions. Retirement income from such accounts depends on how much is saved and how much the money earns when invested in stocks, bonds, or other financial instruments, typically managed by an investment bank or insurance company at the individual employee’s direction. Crucially, after a typically short vesting period of a year or less, DC retirement accounts are solely the property of the employees who benefit from them. Such accounts are often portable among different employers.

The vast majority of privately employed and self-employed New Yorkers do not enjoy retirement benefits even approaching those available to public employees. Nationally, less than one in five private workers has access to an employer-sponsored DB pension plan; as noted, most of those who have access to any employer-sponsored retirement plan are dependent on 401(k)-style accounts. Where traditional pensions still exist, their benefits are usually smaller—and, of course, are not fully guaranteed if a plan sponsor goes bankrupt or otherwise lacks the assets to make good on its promises.

Replicating a guaranteed stream of income equaling a typical public pension would be prohibitive for most comparably salaried private sector workers, especially starting at similarly early retirement ages. For example, as of 2020, NYSTRS members retired at a median age of 61 after 28 years of service, their median final average salary was $90,305, and their median annual pension benefit was $50,101. A lifetime annuity promising the same income stream to a male of the same age would cost $932,000.3 The much higher pensions earned by career teachers in well-paying downstate districts are equivalent to private annuities costing well over $1 million. These figures do not include the value of heavily employer-subsidized health insurance coverage, which most teachers continue to receive throughout retirement. Retiree health insurance coverage is now even more rare than DB pensions in the private sector.4

SETTING THE RULES IN ALBANY

Public pension benefit levels and eligibility rules in New York are controlled solely by state legislation. Since the early 1970s, the state Taylor Law has prohibited collective bargaining over pension benefits, although union negotiators in New York City have at times produced non-binding side deals to recommend legislative changes to benefits.

New York’s public pension plans for non-uniformed employees of the state government, public authorities, local governments, and school districts are organized into benefit “tiers” based on hiring dates, as follows:

- Tier 1: benefits are available to all employees hired before June 30,1973;

- Tier 2: covers all employees hired on or after June 30,1973 and before July 27, 1976;

- Tier 3: covers employees hired on or after July 27, 1976, and before Sept. 1,1983;

- Tier 4: includes all employees hired on or after Sept. 1, 1983, and before Jan. 1,2010;

- Tier 5: covers employees hired on or after Jan. 1, 2010; and

- Tier6: covers employees hired on or after April 1, 2012.

New York City employees were not covered by the Tier 5 legislation. However, with a few exceptions, most of the city’s non-uniformed employees and teachers hired after April 1, 2012 are assigned to Tier 6, with benefit structures similar to those available to other state, local and public authority employees across New York.

Police and firefighters generally retire after 20 to 25 years, and their tier structure and benefits traditionally have differed from those available to non-uniformed employees. For more than 30 years prior to 2009, New York City police and firefighters were in a technically expired but repeatedly extended Tier 2 plan; those hired since 2009 have been assigned to Tier 3. Outside New York City, police and firefighters hired since April 1, 2012, are assigned to their own niche of Tier 6.

The breakdown of pension fund membership by tier is shown in Table 2.

Source: Pension system annual financial report

HOW PENSIONS ARE PAID FOR

Traditional DB pension plans aim to be fully funded—maintaining sufficient financial assets to cover all current and future pension obligations to retirees and their beneficiaries, spread out for seven decades or more, across the life expectancies of the plan’s youngest members. Calculating the amount required to hit this target is a complicated process, reflecting variables including long-term projected salary growth and inflation rates, as well as the estimated lifespans of pension system members who will be collecting benefits.

The projected rate of return on pension fund assets is the key determinant of the pension funding burden on employers and thus taxpayers—because public funds, unlike their private corporate and union counterparts, are allowed by government accounting standards to use an assumed return rate to “discount” the retirement benefits they are obliged to pay for decades to come. The discount rate applied to future obligations is a crucial determinant of a pension system’s necessary funding levels: the lower the rate, the larger the contributions required to meet the goal of fully funding all promised benefits.

Through the 1970s, public pension funds relied more on low-risk investments in corporate bonds and other highly secure financial instruments, with less than half of their assets in publicly traded corporate stocks. Even as inflation and interest rates rose in the 1970s, New York pension plans assumed low rates of return of less than 6 percent. However, from the mid-1980s through 1990s, as pension funds across the country began allocating more of their assets to publicly traded corporate stocks, rate of return assumptions for government retirement systems rose to between 7.5 percent to 8.75 percent

During the historic bull market of the 1980s and ‘90s, investment gains easily exceeded expectations, averaging in the double digits. As shown in Figure 1, this led to steep declines in tax-funded employer contribution levels. But as the funds lost money, required employer contributions rates began to rise steeply.

Sources: NYSLRS Annual Financial Reports, City of New York Financial Plans

TARGETING DISCOUNT RATES

As recently as 2009, all of New York’s public pension funds pegged their target rates of return at 8 percent, which was roughly the norm for public systems around the country at the time. Since 2010, Comptroller DiNapoli has been periodically reducing the rate assumed by NYSLRS—initially to 7.5 percent, then to 7 percent in 2015, and to 6.8 percent in 2019. The summer of 2021, DiNapoli announced he had accepted his actuary’s recommendation to further reduce the NYSLRS discount rate to 5.9 percent, the lowest (and therefore most prudent) adopted by any of the nation’s largest pension plans.

With no changes to other assumptions, the lower investment return assumption and discount rate would result in higher required contributions by employers. But DiNapoli coupled his discount rate reduction with another change in assumption: pension contributions for FY 2023 won’t be based on “smoothed” calculations of investment returns over the past five years but on a “restart” of the pension fund’s asset measure based on the supercharged FY 2021 return of 33.55 percent. The restart comes with risk: if investment returns over the next few years average below the assumed rate of return, as they did in the early 2000s and again in the Great Recession, employer contributions will need to be sharply increased in just a few more years.

Thanks to the restart, and despite the move to a lower return assumption, DiNapoli therefore was able to announce a sharp reduction in employer pension contribution rates for most NYSLRS employees (those enrolled in the Employee Retirement System, or ERS), from 16.2 percent to 11.2 percent of covered payroll for FY 2023. The rate for police and fire employees (enrolled in PRFRS) will be reduced by a smaller amount, from 28.3 percent to 27 percent of payroll. According to the fund’s actuary, this will reduce total employer contribution to $4.4 billion, or $1.5 billion less than the expected employer contributions during the same period for FY 2022, and the lowest level since 2011.

Sources: NYSLRS Annual Financial Reports, City of New York Financial Plans

New York’s other funds so far have failed to follow DiNapoli’s lead. The NYSTRS also realized a record return in 2021, but adopted only a token reduction in its discount rate, from 7.1 percent to 6.9 percent. Disregarding a recommendation by their own actuary, who sought a reduction to 6.8 percent, the five New York City pension fund boards approved a two-year extension of their existing discount rate of 7 percent (a level former Mayor Michael Bloomberg once compared to a promise from the notorious investment fraudster Bernie Madoff).5

While most public pension managers continue to resist the idea, many independent actuaries and financial economists agree that the net present value of risk-free public pension promises should be calculated based on lower discount rates.

As shown in Table 3, based on government standards, New York’s public retirement systems appear to be fully funded or even over-funded, with negligible unfunded liabilities. But measured using the risk-free rate associated with U.S. Treasury bonds (currently just above 2 percent), the ratios partially collapse—revealing combined unfunded liabilities of $227 billion for the state-level systems and $171 billion for the city pension funds. The city’s Fire Pension Fund is especially weak, with less than half the assets it needs to make good on liabilities discounted at a risk-free rate.

Source: Author’s calculations, based on data from pension funds

By comparison, measured by discount rates just above the risk-free level, the nation’s 100 largest corporate-sponsored pension plans were much healthier as of 2020: they had average funded ratios of 88 percent, meaning their assets equaled 88 percent of their promised benefits.6

The bottom line: when advocates of the existing system boast that New York public pensions are well-funded, the measure needs to be taken with a large grain of salt.

CHARTING THE TRAIL

The cutoff dates for each state and local pension tier reflect a nearly 50-year history of periodic legislative attempts to control surges in public pension costs.

The most generous broadly available pension plan was Tier 1, which required no employee contribution and allowed unrestricted retirement with full pension as early as age 55. Significantly, Tier 1 did not cap the final average salary (FAS) used as a basis for computing the pension. Thus, compared to employees hired after 1973, Tier 1 members had more ability to pad their pensions by working additional overtime in the year or two before retiring.

Tier 2, covering those hired starting in mid-1973, raised the basic retirement age to 62. Retirement at age 55 with the maximum pension was still allowed for Tier 2 employees but restricted to those with at least 30 years of service. Pensions were reduced for those with fewer than 30 years in the system who retire between the ages of 55 and 62. In addition, the definition of salary used to compute pensions was subject to a cap. Like Tier 1, Tier 2 required no employee pension contribution.

The creation of Tier 3 during the New York City fiscal crisis in 1976 marked the first time most state and local employees in New York were required to contribute some of their own money—3 percent of salaries—towards their future retirement benefits. The retirement ages were basically the same as in Tier 2, but the cap on the final average salary used as a basis for computing pensions was slightly lowered. Pension benefits included for the first time an annual automatic cost of living adjustment (COLA). Most significantly, Tier 3 also included a feature common to private pensions: the pension benefit would be “offset,” or reduced, to reflect a portion of the retiree’s Social Security benefit starting at age 62. Tier 3 pensions initially were significantly less expensive for employers.

Tier 4, adopted just seven years after Tier 3 in 1983, eliminated the Social Security offset and the COLA. For the first 16 years after its enactment, Tier 4 also required a 3 percent employee contribution. This tier also initially featured more restrictions on early retirement, which were loosened under a series of pension enhancements in subsequent years. Tier 3 members can opt for a Tier 4 benefit, which in most cases is larger. Under pension enhancements passed in 2000, Tier 3 and 4 workers outside New York City, and most civilians in city pension plans as well, are no longer required to make pension contributions after 10 years of government employment.

UPPING THE PENSION ANTE

The state Legislature repeatedly increased pension benefits for targeted groups of state and local employees during the 1990s, culminating at the end of the decade with approval of the biggest sweetener deal yet: a package combining cost-of-living adjustments to existing pensions, automatic partial inflation-indexing of future pension payments, and the permanent elimination of employee contributions for Tier 3 and 4 retirement system members who had been on the payroll for at least 10 years.7 Governor George Pataki, Comptroller Carl McCall, and state lawmakers effectively framed these changes as a free lunch, assuming the long stock market boom would continue indefinitely. In fact, ironically, the pension enhancements were signed into law just as Wall Street’s dot-com bubble was bursting in mid 2000.

As state officials should have recognized, the minimal employer contribution rates of the 1990s were a historical anomaly—and clearly unsustainable. “Normal” contribution rates—assuming a hypothetical steady state of asset returns meeting the systems’ optimistic investment targets—would have ranged from 11 to 12 percent for most non-uniformed state and local employees, including teachers, to nearly 20 percent for most police and firefighters in NYSLRS.

The decade that followed the enactment of the 2000 pension deal was characterized by extremely volatile—and ultimately stagnant—pension fund investment returns. Asset values dropped sharply between 2000 and 2002, recovered over the next five years, and then dropped even more sharply after 2007. The combination of falling asset prices and rising benefit outlays meant the pension funds were developing huge shortfalls. Meanwhile, employee contributions to the state pension funds actually decreased during this period, as a growing number of Tier 3 and 4 members reached the 10-year seniority mark.8

Taxpayers were left to pick up the slack. In 2000, tax-funded employer contributions to all of New York’s pension funds had totaled just under $1 billion. By 2009, as government revenues were crashing in the wake of the financial crisis and Great Recession, pension contribution had risen to nearly $10 billion—and still rising, towards their ultimate peak of nearly $17 billion. By then, the crisis had grown too large for Albany to continue ignoring.

THE TWO NEWEST TIERS

In December 2009, at the urging of then-Governor David Paterson, the New York State Legislature approved a fifth tier of slightly reduced pension benefits for state and local employees hired after Jan. 1, 2010. However, while benefits in the new plan were less expensive than those in previous tiers, Tier 5 was not the “significant pension reform” promised by Paterson when he originally proposed the law. Instead, the Tier 5 changes for ERS members essentially restored most key elements of the original 1983 Tier 4 pension plan, before those benefits were repeatedly enhanced in the 1990s and in 2000.

More clearly needed to be done, and Governor Andrew Cuomo proposed further changes in a new pension Tier 6. The principal money-saving changes to Tier 5 benefits included:

- An increase in the minimum full-benefit retirement age, from 62 to 63 for all members.

- Higher employee contribution rates, ranging from 3 to 6 percent for those earning $75,000 or more.

- An adjustment in the final average salary calculation to cover five instead of three consecutive highest-paid years, effectively reducing the base in most cases.

- A $15,000 cap, indexed to inflation, on “pensionable” overtime, which was unlimited for pre-2010 hires and subject to a looser cap for Tier 5 members.

- A cap on credited wages linked to the governor’s salary ($250,000 as of 2022).

While the changes of 2010 and 2012 did not fundamentally alter the defined-benefit system for the vast majority of government workers, the new tiers have produced real savings. In NYSLRS alone, contributions for 2022 will be $755 million lower for Tier 5 and 6 members than they would have been under Tier 4, based on data reported in the system’s annual report. A preliminary estimate from NYSTRS indicates the state teacher pension plan has saved $350 million. The New York City actuary’s office has not estimated the city’s savings from Tier 6 across all plans, but the NYCTRS alone has seen its net employee contributions increase by $82 million since the Tier 6 plan with its new salary-based contribution requirement took effect in 2012.9 The savings for all plans will only grow as more non-contributing members of tiers 1 through 4 are replaced by Tier 5 and 6 employees; Tier 6 members, in particular, will contribute more as their salaries rise.

Cuomo’s most significant Tier 6 innovation didn’t produce big savings but pointed the way towards more fundamental reform for all of government. Aside from amending the terms of existing defined benefit plans, the Tier 6 legislation created a new Voluntary Defined Contribution (VDC) Program, modeled on the Optional Retirement Plans offered since 1964 to employees of the State University of New York and City University of New York. The VDC program has been available as an alternative to the traditional DB plan for non-union state and local employees hired after June 30, 2013, at salaries of $75,000 or more.

Cuomo’s limited DC reform followed a recommendation in the Empire Center’s February 2012 report, “Optimal Option,” which explains the structure and benefits of SUNY plans. However, while the VDC was rooted in a higher education plan, it pointedly excluded elementary and secondary teachers from participating. The annuity-based SUNY retirement model represents a better-designed alternative than the defined-contribution proposal in Cuomo’s original Tier 6 plan, which would have set up a rudimentary and underfunded 401(k)-style retirement account as an alternative to the traditional pension for all workers, unionized and non-unionized.10

Employee contributions to the VDC are pegged at the same levels as in the Tier 6 traditional DB plan—ranging from 3 percent to 6 percent of salary, depending on total annual wages. The employer share is a flat 8 percent of gross wages, roughly equivalent to the predicted, theoretical “normal” employer rate for Tier 6 but only half the average billed rate for ERS members in fiscal year 2022-2023, and barely one-third of the contribution rate charged by the New York City ERS.

SEIZING AN ALTERNATIVE

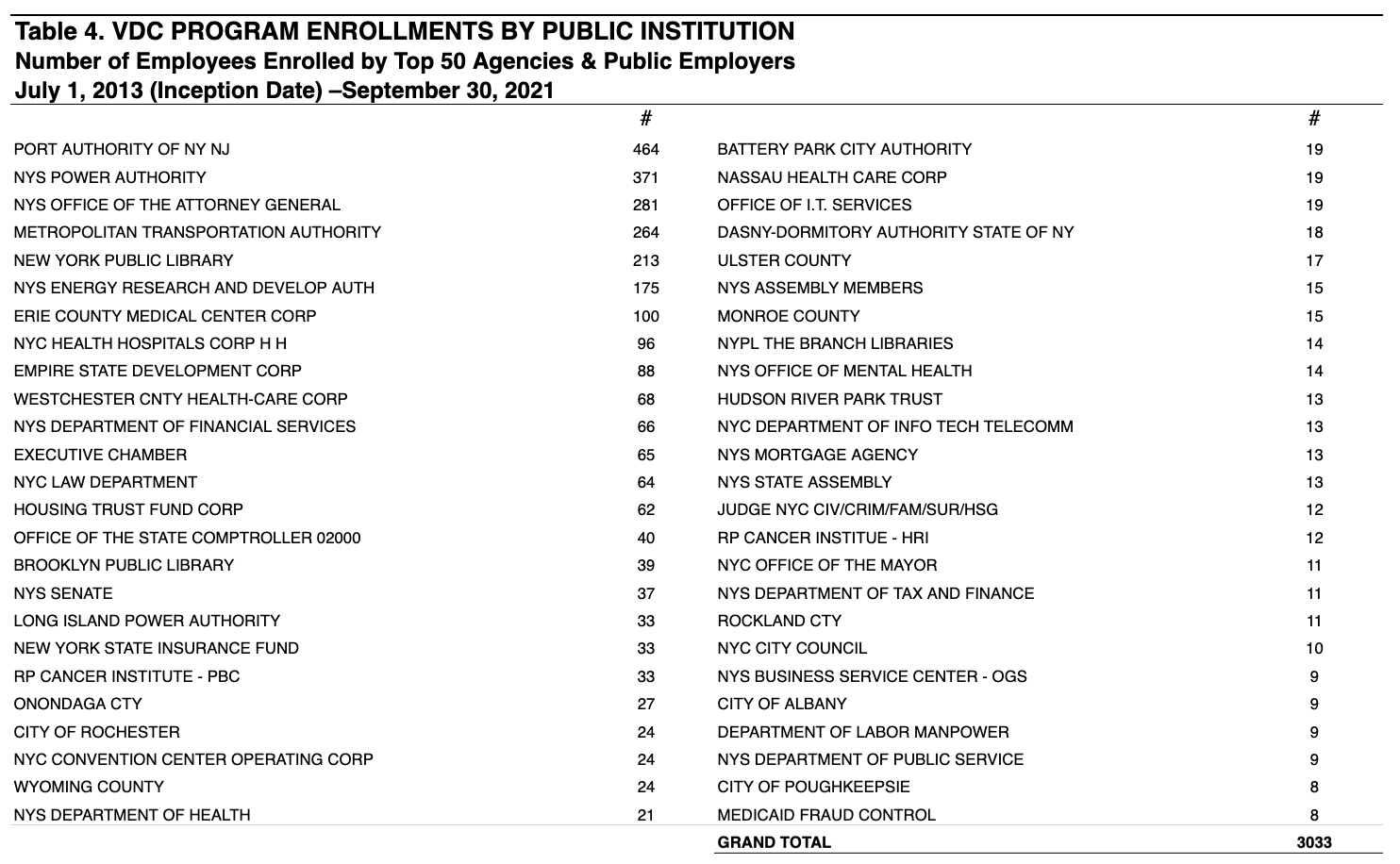

Since it opened to membership in mid-2013, the VDC option has been chosen by a total of 3,548 state and local employees, some 3,268 of whom were still on the payroll as of September 30, 2021. Total program contributions to date exceed $160 million, including $31 million through the first three calendar quarters of 2021. VDC members have a choice of four different private investment managers: TIAA, AIG Retirement Services, VOYA, and Fidelity. As of 2021, TIAA was the most popular choice, with 57 percent of contributions, followed by Fidelity with 30 percent.

Source: New York State Voluntary Defined Contribution Program

As shown in Table 4, the plan has been especially popular in public authorities and government health care institutions employing large numbers of higher-salaried, non-union professionals and technicians who have significant private-sector experience. The Port Authority, Power Authority, Metropolitan Transportation Authority, and New York State Energy Research and Development Authority collectively have employed nearly one-third of all VDC participants since 2013. Among state government agencies, the Attorney General’s office has had the most VDC enrollees with 281, or 41 percent of assistant attorneys general on the payroll as of 2020, while the Executive Chamber—i.e., the governor’s office—has employed 65, equivalent to nearly half of the latest total Chamber headcount.

The VDC has also been popular among members of the state Legislature, enrolling 15 Assembly members and seven state senators—a minority of the 213 total lawmakers, to be sure, but a non-negligible share of those elected since 2013 who were not already members of a government pension fund and thus ineligible for the new plan.

The DC option was not made available to more employees mainly because it was opposed by their unions, especially by the Civil Service Employees Association, whose members include the lowest-paid rung of clerical support and institutional services employees working in state and local government. But the eligibility limitation was especially questionable for public school teachers, who have especially high turnover rates during their early years in the classroom.

A BETTER DEAL FOR TEACHERS

Given the profession’s high turnover rates, traditional DB pensions are an especially raw deal for teachers. As a ground-breaking 2015 research report noted, “most teachers either won’t qualify for a pension at all, or will qualify for one so meager that it will be worth less than their own contributions.” Based on a review of pension plans across the country, the report continued:

Although the debate on public pensions concentrates on employees with 30 years of service, most public school teachers have much shorter careers. According to the latest national data, three in 10 new teachers leave within five years. Other teachers cross state lines to teach elsewhere in subsequent years, splitting their careers across multiple state pension plans. Those who leave subsidize benefits for teachers who stay in one state or school district for an entire career.

State pension plans provide little retirement income security to most teachers with shorter tenures, even many who spend as long as 20 or 25 years teaching in one state. Virtually every plan requires participants to contribute toward the cost of their retirement benefits, and employees must work many years before their future benefits exceed the value of their required contributions. Those who leave before reaching that milestone do not receive any employer-financed retirement benefits, despite their often-lengthy careers.11

Looking at New York in particular, the report estimated that NYSTRS members hired since 2012 need to serve 24 years to break even on their pension—but two-thirds will never stay in the system that long. Largely due to its five-year vesting period, Tier 4 had a much shorter break-even period—just 12 years—but even under that plan, the report estimated, 61 percent of teachers would never reach the break-even point.

The assertions in the Urban Institute-Bellwether report can be further illustrated by the hypothetical example of a young teacher hired by a northern Westchester school district in 2013-14, who chose to leave her job at the end of the 2020 school year—to change professions, raise a family, or move to another state, or for some other not-uncommon reason.

After seven years, this teacher was still three years short of vesting for a pension from the traditional DB plan, but she would be entitled to withdraw her contributions to NYSTRS, which would yield a refund of $22,660, including 5 percent annual interest, as shown in Table 5. If she’d been able to enroll in the VDC option during the same period, based on actual returns in a TIAA “Lifecycle” fund that would be a default option for someone her age, she would have accumulated $58,110 in a personal retirement account.

To be sure, the VDC comes with the same warning label as all private investment funds: past performance is no guarantee of future results. But even if her retirement account had yielded no investment gain, the ability to recover both her own and the employer contribution would leave her with $48,800, more than twice the NYSTRS refund for the same period.

Educators themselves need no persuading: 71 percent of the New York State public school teachers responding to a 2012 Empire Center survey said they favored having a choice of DC and DB retirement plans.

REAL PENSION REFORM AND WHY IT’S NEEDED

The Empire State can—and should—aim to minimize if not eliminate the financial risks, volatility and unpredictability of the existing pension system. From the standpoint of employers and taxpayers, the best way to accomplish this would be to shift new employees to DC plans emphasizing individual retirement accounts.

Pure DC plans so far have been mandated for broad government employee categories in only two states, Michigan and Alaska. However, at least 17 public pension funds in 14 other states have established “hybrid” plans combining elements of both DB and DC models.12 Specifics differ, but such plans generally offer employees the advantage of a small guaranteed basic benefit plus individual accounts, while protecting employers and taxpayers from open-ended losses.

The federal government adopted the hybrid model in 1984, when it replaced its own largest traditional pension plan for civilian workers with a combination of a reduced DB pension and a DC supplement known as the Thrift Savings Plan (TSP).13 With 5 million account holders and $558 billion in assets, the TSP is the world’s largest employer-sponsored DC retirement plan. According to a 2017 survey, nearly nine out of 10 TSP participants reported they were either satisfied or extremely satisfied with the plan.14 Even in 2008, when a looming financial crisis dampened investor optimism, the TSP had favorable rating of 81 percent.

The downside of a hybrid plan is that, by retaining elements of the DB pension structure, it also retains opportunities for the kind of steady sweetening that occurred when funding levels rose in the current system. The actuarial and financial accounting involved in the DB system is dauntingly complex, inviting the kind of buy-now, pay-later options that politicians historically have found difficult to resist.

RECOMMENDATIONS

End guaranteed pensions and retiree health coverage for elected officials

Most state and local elected officials are members of the traditional pension system. This gives politicians a vested interest in preserving the status quo—and in clinging to government employment as a way to build credited pension time. To end this cycle, all elected officials should be enrolled in the currently “voluntary” defined contribution plan, an extension of the existing SUNY optional plan created by Governor Cuomo’s 2012 Tier 6 pension reform. In addition, politicians should no longer be eligible for retiree health benefits.

Make K-12 teachers eligible for the VDC optional retirement plan

As a first step in moving all future hires into DC plans, all new teachers should be given the option of choosing the VDC plan. Seventy-one percent of the New York State public school teachers responding to a 2012 Empire Center survey said they favored the option, which also has been endorsed by the New York State School Boards Association.

In addition to providing a more portable and flexible retirement savings plan for those who spend a lifetime in the teaching profession, the VDC can help attract more non-traditional applicants for teaching positions at a time when schools are complaining of teacher shortages, particularly in subjects areas such as science and math.15

Create all-new retirement plans for the long run

Additional DB-DC “hybrid” retirement plans should be developed for all other employees. Such plans can be further tailored to continue providing for the earlier retirement ages of police and firefighters, while fully preserving existing disability and death benefits.

Mandate truth-in-accounting for public pension funds

As recommended in a 2016 report from the Blue Ribbon Panel of the Society of Actuaries, New York pension funds should be required to at least report their funded status using alternative measures based on risk-free interest rates.16 Constitutionally guaranteed benefits are the closest thing to a risk-free proposition for government employees. Taxpayers, who ultimately backstop the guarantee, should at least be informed of how close they are to actually funding those benefits on a risk-free basis.

In addition, any pension reform should retain the existing Taylor Law provision prohibiting collective bargaining of pension benefits—and that provision should be expanded to cover other retirement benefits. This is an essential step towards getting a handle on more than $300 billion in unfunded liabilities for retiree health coverage currently promised (but not constitutionally guaranteed) by state and local governments.17

CONCLUSION

Traditional DB pension funds are financially and actuarially complex. They tend to demand new infusions of cash when it is in short supply—in the wake of economic downturns that stretch government finances to the breaking point. And as noted here, they are expressly designed to short-change workers who don’t commit themselves to a long-term or full career on a government payroll. Tinkering with existing pension rules to address pension padding, double-dipping and overtime spiking won‘t change that.

Other benefit models can provide public employees with retirement security without threatening to crowd out vital services in a future fiscal crisis. DC or hybrid plans also would allow much less potential for abuse and gaming. To repeat a point with which we ended our 2010 report on the Empire State’s exploding pension bomb: the necessary next step in pension reform for New York is not to mend the existing system, but to upend it.

ENDNOTES

1 82 N.Y.2d 354 (1993)

2 Girard Miller, “Top 12 Pension and Benefits Plan Issues for 2009: Part I,” Governing magazine, Jan. 22, 2009. http://www.governing.com/columns/public-money/Top-12-Pension-and-.html

3 https://www.schwab.com/annuities/fixed-income-annuity-calculator.

4 E.J. McMahon, “Iceberg Ahead: The Hidden Cost of Public Sector Retiree Health Benefits in New York,” Empire Center, September 2010, http:/www.empirecenter.org/ Documents/PDF/iceberg-final.pdf

5 The city pension funds’ discount rate is established by law. The latest two-year extension of the 7 percent rate was unanimously approved by both houses of the Legislature in June and signed into law (Chapter 391) by Governor Cuomo in August.

6 As of October 2021, the average discount rate for a single-employer private pension plan was at 2.76 percent. https://www.mercer.us/our-thinking/wealth/mercer-pension-discount-yield-curve-and-index-rates-in-us.html

7 Article 19 of the state Retirement and Social Security Law.

8 Contributions to New York City pension funds increased by about 50 percent during this period, principally due to a surge in hiring of police officers and firefighters whose contributions are largely reimbursed by the city with increased take-home pay.

9 New York City Teachers Retirement System, 2020 Comprehensive Annual Financial Report, p. 157, Schedule 3.

10 Cuomo’s original proposed DC option for all workers was strongly opposed by public employee unions, none more so than the Civil Service Employees Association (CSEA). But after the SUNY-style plan was substituted for non-union workers in the final Tier 6, CSEA complained that the SUNY-style plan created by the final bill was an overly generous “boondoggle.” The New York Daily News called that “breathtaking hypocrisy.”

11 Chad Aldeman and Richard W. Johnson, “Negative Returns: How State Pensions Shortchange Teachers,” TeacherPensions.org and Bellwether Education Partners, September 2015. https://www.urban.org/sites/default/files/publication/71521/2000431-Negative-Returns-How-State-Pensions-Shortchange-Teachers.pdf

12 https://www.nasra.org/hybrid

13 Guaranteed pension benefits for post-1984 Federal Employee Retirement System members accrue at the rate of 1 percent of salary per year, which is half the maximum level available to New York State employees.

14 https://www.frtib.gov/ReadingRoom/SurveysPart/TSP-Survey-Results-2017.pdf

15 See e.g. ”Teacher Shortage? What Teacher Shortage?” a 2017 report from the New York State School Boards Association.https://www.nyssba.org/clientuploads/nyssba_pdf/teacher-shortage-report-05232017.pdf

16 https://www.soa.org/blueribbonpanel/

17 Peter Warren, “New York’s Growing Debt Iceberg,” Empire Center, December 1, 2021. https://www.empirecenter.org/publications/new-yorks-growing-debt-iceberg/

You may also like

34 MTA Workers Made $200K+ In Overtime In 2025

Thirty-four employees of the Metropolitan Transportation Authority (MTA) received more than $200,000 in overtime payments in 2025, as total annual pay surpassed half a million dollars for some, according to , the Empire Center’s governm Read More

Overtime on State Payroll Jumps 21%

104 employees made over $500k in 2025 total annual pay.

2,450 employees were paid more than Gov. Kathy Hochul's Read More

Seven Reasons Not To Raise Taxes in New York

Despite the robust growth of state revenues in recent years, many of New York's elected officials are pushing to further increase the tax burden on the state's residents and businesses.

Read More

Ninety New York Educators Receive $300k+ in Annual Pay

Ninety employees from New York’s school districts (outside New York City) received more than $300,000 during fiscal year 2025, according to , the Empire Center’s transparency website.

The public educator pay data are based on salary information rep Read More

NYC Employees Receive $300k+ in Overtime

Two New York City employees received more than $300,000 in overtime payouts, according to fiscal year 2025 , the Empire Center’s government transparency website. The city paid a total of $2.9 billion in overtime during fiscal year 2025. Read More

State Lawmakers Spend $268 Million on Legislative Operations

Spending by state lawmakers on office personnel and administrative costs varies widely, with some paying out nearly twice as much as others on their office operations, according to the most recent reported, posted to SeeThroughNY.net.

Read More

School Districts Plan To Spend Over $35K Per Student, Outpacing Inflation

School districts presenting budgets to voters on Tuesday, May 20, plan to spend an average of $35,012 per student, up 4.6 percent from the current school year, according to new state data.

Data collected by the state Education Departme Read More

Overtime on State Payroll Surges 11%

Twenty-three New York State employees collected over $200,000 each in overtime, according to posted today on SeeThroughNY, the Empire Center’s government transparency website. Read More