On the eve of Governor Kathy Hochul’s FY 2024 Executive Budget presentation, which is likely to call for a continued expansion of New York’s already high state debt, Comptroller Thomas DiNapoli has unveiled a new proposal for constitutionally curbing the state’s seemingly uncontrollable appetite for borrowing.

Article VII, Section 11 of New York’s State Constitution has long barred any general obligation bond issuance without voter approval, but this provision effectively has been negated by decades’ worth of “backdoor borrowing” in the form of public authority bonds, backed by annual state budget appropriations.

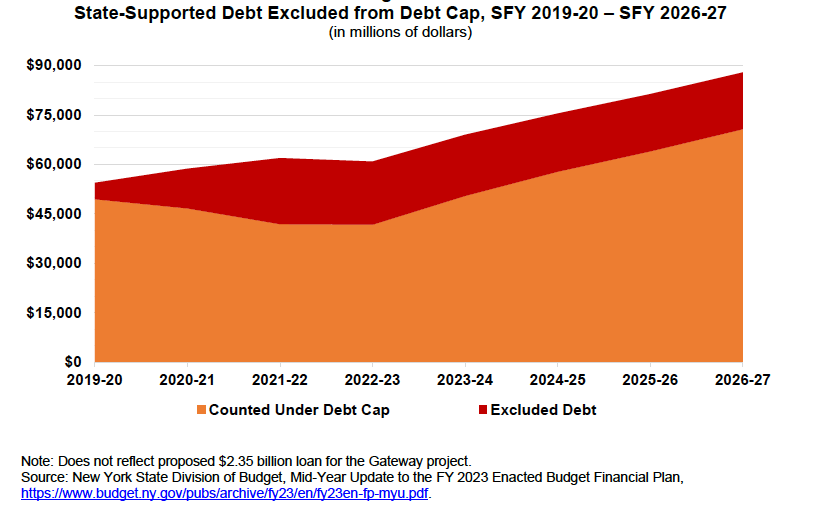

A reform enacted in 2000 limited total state debt to 4 percent of state personal income. However, because the 2000 cap is only statutory, exceptions to the cap routinely have been made through debt authorized by other statutes. As illustrated in this chart from the state comptroller’s latest debt reform report, nearly $20 billion in state-supported debt has been excluded from the current cap.

DiNapoli’s remedy—updating a proposal he first made a decade ago—would be a constitutional cap limiting outstanding debt to 5 percent of a rolling 10-year average of the state’s total personal income. Exceptions to the cap, or any increase in the cap itself, would require voter approval.

The borrowing binge

The need to rein in state debt couldn’t be clearer.

As shown in the table below from Empire Center’s “Next New York” policy guide, New York’s total long-term debt load of $5,134 per capita was more than double the national average. Even using the narrower debt measure favored by the state Division of the Budget, New York’s total is higher than six of its peers and almost twice the national average. New York’s relatively heavy state debt load by both measures is noteworthy given the unusually large, separately financed capital budgets of its county and municipal governments—especially New York City, which fiscally dwarfs all but a few states.

As the comptroller notes, Hochul’s FY 2023 capital financing plan forecast a significant increase in state-related debt over the next several years. Having averaged $55 billion over the previous decade, outstanding state-related debt jumped to $62 billion in FY 2022 and is forecast to hit nearly $88 billion in FY 2027—a 42 percent increase.

In a notable shift, economic development is projected to displace higher education as the state budget’s second largest capital projects spending category in FY 2023-27, averaging $2.2 billion in annual disbursements, more than double the average from 2010 to 2022. Most of this money will be funneled through the Empire State Development Corp. (ESDC), New York’s umbrella agency for economic development financing. ESDC’s five-year projected spending through FY 2027 comes to nearly $11 billion, with the lengthy list of planned capital disbursements including $1.4 billion for urban and rural broadband access, $500 million for offshore wind development, and a $600 million state contribution to the $2 billion cost of building a new Buffalo Bills stadium.

DiNapoli says a constitutional debt reform amendment should include a ban on “the use of State debt … solely benefiting a private enterprise.” In fact, however, the wording of Article VII, Section 8.1 of the State Constitution already prohibits—or seems to prohibit—such borrowing:

The money of the state shall not be given or loaned to or in aid of any private corporation or association, or private undertaking; nor shall the credit of the state be given or loaned to or in aid of any individual, or public or private corporation or association, or private undertaking, but the foregoing provisions shall not apply to any fund or property now held or which may hereafter be held by the state for educational, mental health or mental retardation purposes.

Despite that clear prohibition, the state Court of Appeals in the 2011 case of Bordeleau v. State upheld the dismissal of a taxpayer lawsuit challenging state appropriations directly or indirectly benefiting, among others, IBM Corp. and Global Foundries. As a result, as one of two dissenting judges put it at the time, “it is hard to see what is left of the constitutional prohibition.” Any constitutional amendment aiming to stop economic development grants will need airtight wording to shut down the loophole opened by the state’s highest court in Bordeleau.

Outside of a constitutional convention—which the state’s voters haven’t been willing to authorize since 1967—an amendment to New York’s constitution must originate as a joint legislative resolution. The resolution, in turn, must be passed by two consecutively elected legislatures (e.g., the members taking office in 2023-24 and 2025-26), before it can be placed on the statewide ballot for voter approval. Note: this process must be initiated by and within the Legislature, with no gubernatorial involvement.

In practical terms, New York’s progressive-dominated Senate and Assembly are unlikely to support any borrowing or spending limitation. But DiNapoli’s proposal isn’t pointless. At the very least, the comptroller has laid out a marker for active consideration when—not if—the state spends, taxes, and borrows its way into another serious fiscal crisis. When a crisis looms, prospective bond investors and rating agencies will demand evidence that Albany is serious about controlling its appetites.

You may also like

Federal Suit Traces Medicaid Fraud to the Top of NYS Government

The Trump administration's latest salvo against Medicaid fraud takes aim at a different kind of target – two high-ranking New York officials along with a major state contractor.

A Read More

Healthcare Highlights in the New State Budget

Governor Hochul's focus on affordability seems to have skipped over the healthcare portions of the new state budget.

The deal finalized May 27 Read More

Lack of Common Sense on Energy in the Budget

Lack of Common Sense on Energy in the Budget

Anyone hoping the governor would make even modest, common-sense changes to New York’s disastrous energy policies will be disappointed. The energy portion of the budget is out, and the nons Read More

Four Problems with a Statewide Pied-à-Terre Tax

Soon after Governor Hochul floated the idea of a "pied-à-terre" tax in New York City, Albany Sen. Patricia Fahy proposed to expand the concept to the rest of the state.

As with H Read More

Albany Should Listen to Jamie Dimon

In his annual message to shareholders, JP Morgan Chase's chief executive, Jamie Dimon, offered a timely and pointed warning for New York policymakers.

It's worth , with emphasis add Read More

Albany Wavers on Shutting Down a Medicaid Racket

As Washington threatens to crack down on fraud and abuse in New York's Medicaid program, state legislators are doing their best to demonstrate why federal intervention is needed.

A Read More

Ideas for Cleaning Up New York Medicaid

As the Trump administration cracks down on fraud, waste and abuse in Medicaid, New York is a logical place to start.

New York spends far more Read More

The Bottom Line of Hochul’s Essential Plan Overhaul

Now that New York has won partial federal approval for overhauling its Essential Plan, it's worth being clear about what the state is doing and why.

The is not primarily about "pre Read More