Nearly two-thirds of New York State’s tax receipts are now generated by the personal income tax, or PIT, which relies disproportionately on the highest-earning one percent of New York taxpayers.

Nearly two-thirds of New York State’s tax receipts are now generated by the personal income tax, or PIT, which relies disproportionately on the highest-earning one percent of New York taxpayers.

This paper presents charts and tables highlighting notable trends in state PIT data in light of proposals to extend or increase the state’s so-called “millionaire tax,” along with scheduled PIT rate reductions in tax brackets below the highest income levels.

Key points with a bearing on the income tax debate include the following:

- More of New York’s wealthiest taxpayers are choosing to live in other states, thus minimizing their exposure to the higher millionaire tax. As of 2014, nonresidents were nearly half of all New York taxpayers with total incomes above $1 million—and 59 percent of taxpayers in the more rarified $10 million-and-above class.

- The percentage of New York residents and New York source income among all the U.S. income millionaires has not increased since the millionaire tax was enacted.

- New York is now more dependent than ever on PIT receipts—which in turn are disproportionately generated by the highest-earning 1 percent.

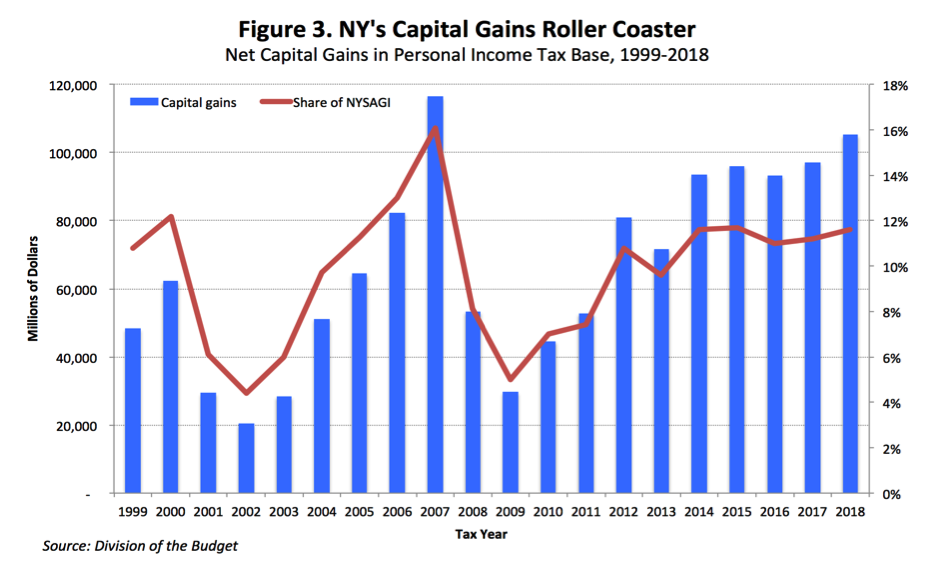

- Net capital gains in New York’s PIT base have recovered nearly to pre-recession levels—tracking an increasingly volatile stock market.

New York State’s temporary surtax rate of 8.82% is 7th highest among all statewide income tax rates. In New York City, the combined state-local top rate is second highest in the nation after California’s.

Scheduled multi-year cuts in personal income tax rates will affect three brackets, ranging from taxable income of $27,750 to $321,050 (or half as much for single filers), as outlined in box above. Two brackets now subject to rates of 6.45% and 6.65% as of 2017 will be collapsed into a single 5.5% tax bracket by 2025. The fully implemented changes, assuming no extension of the millionaire tax, will leave the state with six PIT brackets and a top rate of 6.85%.

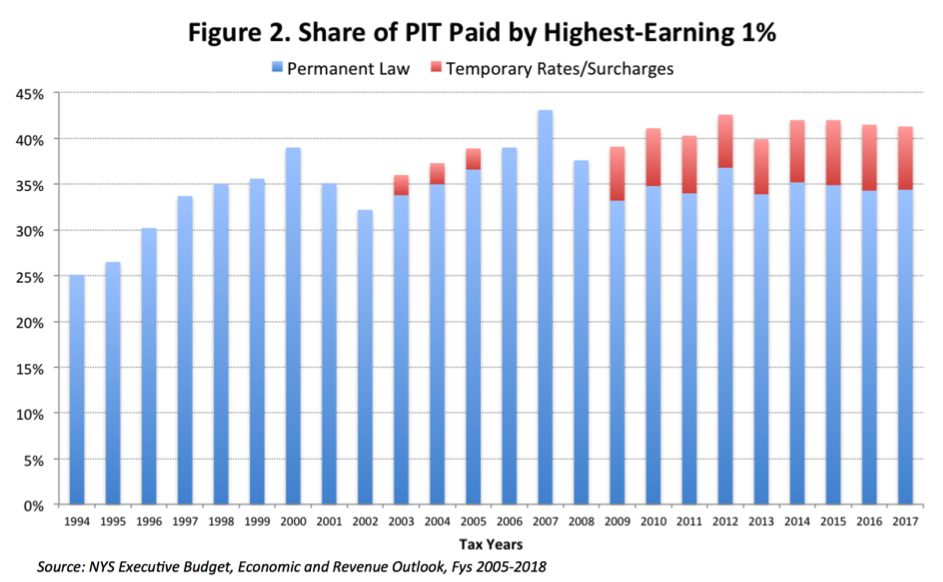

Including the millionaire tax, the highest-earning 1% of New York State taxpayers generate more than 40% of state PIT receipts. But even without added rates on higher incomes, the top 1% share has averaged around 35% since the Tax Reform Act was fully effective in 1997—up from 25% when Gov. Mario Cuomo left office.

As shown in Figure 3, above, the share of New York personal income tax receipts attributed to net capital gains — heavily reflective of stock prices — has risen back to near-record highs. But as the historic trend shows, capital gains are also highly volatile. They crashed by 75% during the Great Recession, just a few years after falling by 66% during the 2001-03 downturn.

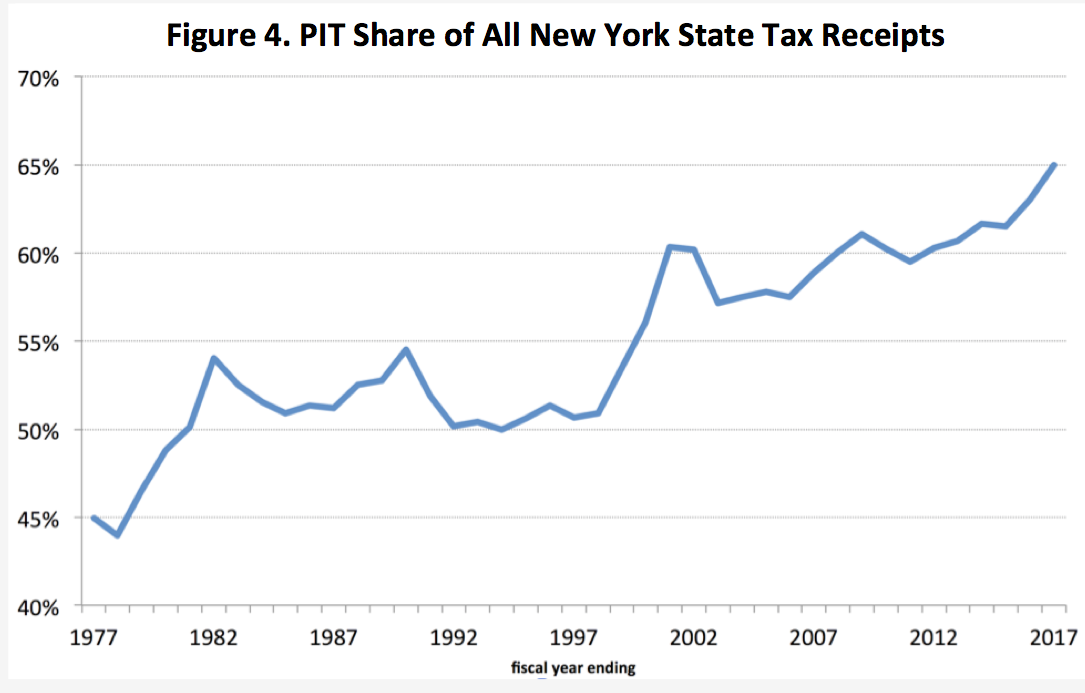

As shown in Figure 4, the personal income tax share of total New York State tax receipts has grown significantly over the past 40 years. In fiscal 2017, the state is more reliant than ever on the PIT, which is generating nearly two-thirds of total tax receipts—which, as shown in Figure 3, are in turn heavily influenced by stock market trends affecting net capital gains income.

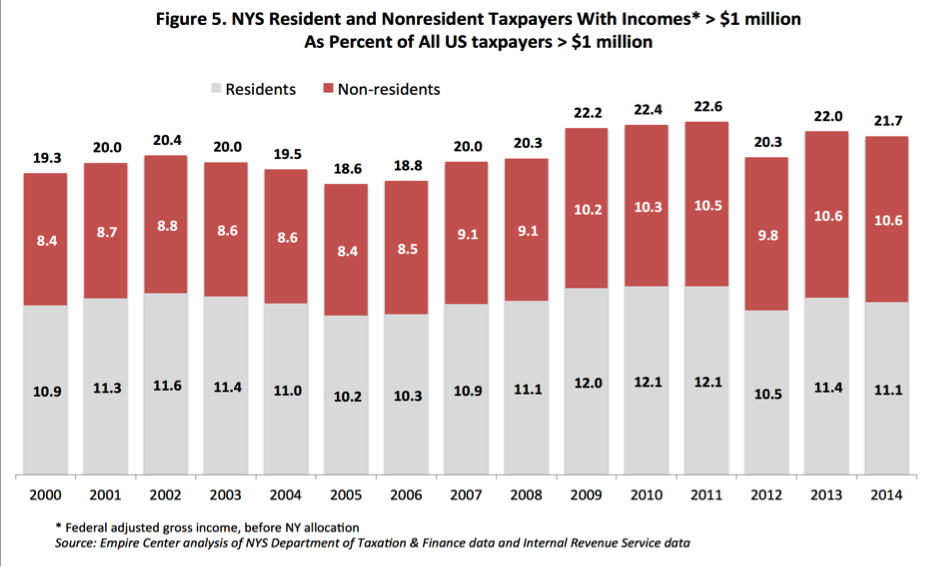

As of 2014, Figure 5 shows, New York State residents comprised about 11% of the U.S. income millionaire total—unchanged from the level of 2008, the year before the state’s temporary millionaire tax was first imposed. But nonresident income millionaires owing some taxes to New York have grown from 9.1% to 10.6% of the national total.

Figure 6 shows how the nonresident share of income millionaires in New York’s PIT base has grown since the recession and initial enactment of the temporary millionaire tax. The greatest shift was in the highest income category—from 51% to 59% among earners of $10 million or more from 2008 to 2014.

You may also like

Altered State: A checklist for change in New York State

This paper describes seven core objectives and offers specific policy recommendations toward their accomplishment. It’s by no means an exhaustive list, rather a good place to start work towards an Altered State with a growing economy, a more efficient public sector and new opportunities for an engaged and informed citizenry. Read More

NY gained fewer “millionaire” filers than US average in 2010-15

New York State has long been home to a large share of the nation’s wealthiest households. But since the Great Recession ended, the Empire State has fallen behind when it comes to gaining additional income millionaires Read More

Making Work Pay

The poverty-fighting effectiveness of the state and federal Earned Income Tax Credit in New York is the focus of “Making Work Pay,” a new Issue Brief from the Empire Center for Public Policy.

In light of Governor Andrew Cuomo’s push for a $15-an-hour statewide minimum wage, the briefing paper explains how the EITC already serves to boost low wages to levels well above the poverty line. Read More