New York’s employer-sponsored health insurance premiums – which were already among the steepest in the mainland United States – rose faster than the national average in 2018, pushing the state’s affordability gap to new heights.

New York’s employer-sponsored health insurance premiums – which were already among the steepest in the mainland United States – rose faster than the national average in 2018, pushing the state’s affordability gap to new heights.

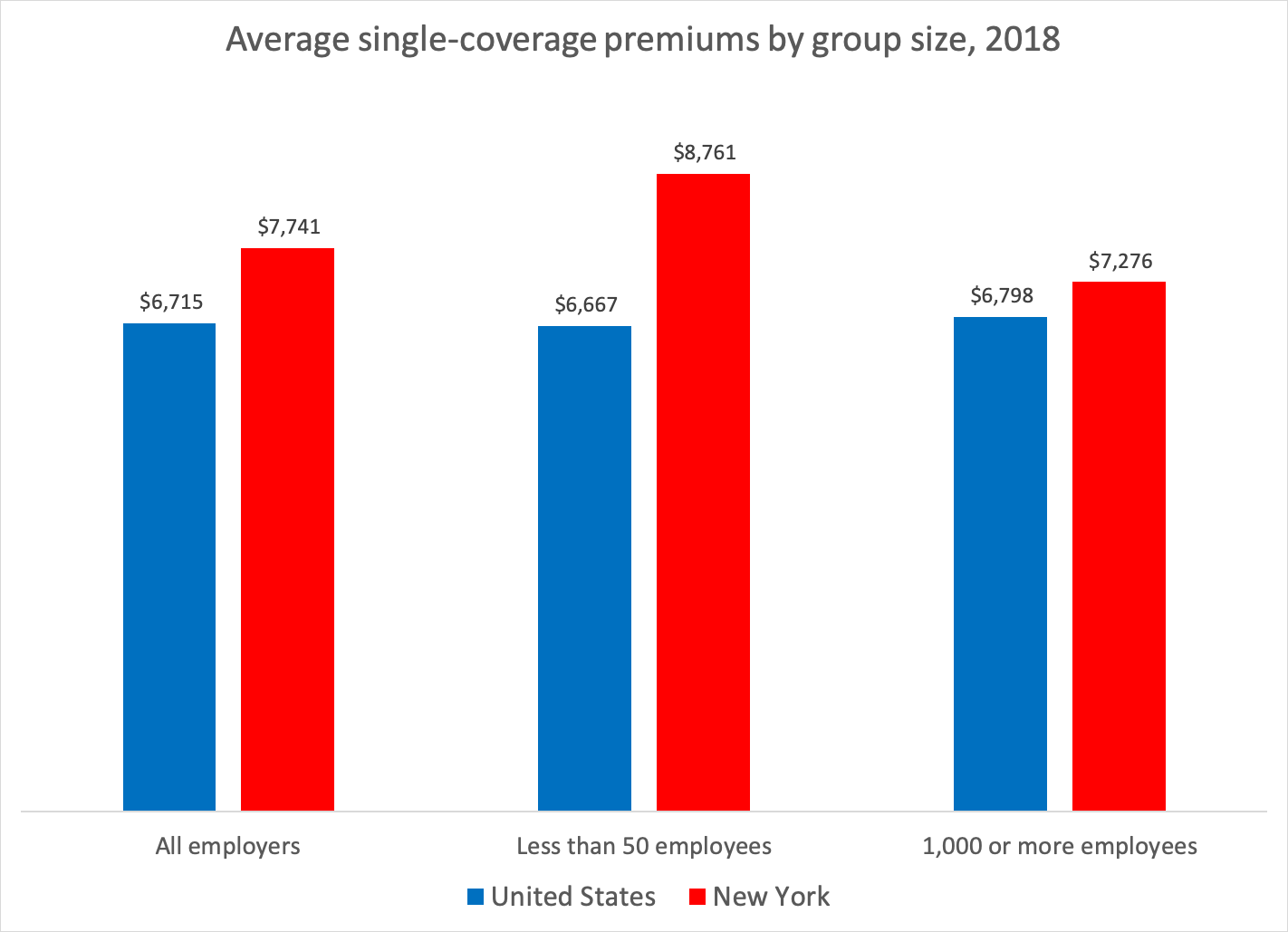

The state’s average single-coverage premium in 2018 surged by almost 6 percent to $7,741 – second only to Alaska (see chart). The rate is 15 percent higher than the national average, New York’s widest gap since the federal survey began in 1996.

The average premium for family coverage grew 3 percent to $21,904. That also ranks second, behind New Jersey, and stands 12 percent higher than the national norm.

The results, from a recently published federal survey, are the latest symptom of an unusual cost spiral in New York’s health-care system.

Earlier this month, a study from the New York State Health Foundation and the Health Care Cost Institute found that the state’s employer-sponsored insurance spending per person rose twice as fast as the national average from 2013 to 2017, outpacing every other state but North Dakota.

Meanwhile, Medicaid spending has been spiking so dramatically that the Cuomo administration resorted to postponing $1.7 billion in payments from the end of fiscal year 2019 to the beginning of fiscal 2020 to stay in technical compliance with a budget cap. If not for that gimmick, state expenditures would have exceeded budgeted amount by almost 8 percent.

Why are New York’s cost pressures especially severe? Contributing factors include the state’s generally high cost of living, especially downstate, along with rapid consolidation in the health-care industry and a high rate of unionization among health workers.

State policies also play a part, including heavy state taxes levied directly on health insurance – which add $5 billion a year to premiums – and an ever-growing list of coverage mandates that Albany routinely enacts without careful cost-benefit analysis.

Far from acting to control health spending, Governor Cuomo and the Legislature keep doing things that will push it higher.

On Aug. 2, for example, Governor Cuomo signed a bill mandating insurers to cover annual mammography screenings for breast cancer starting at age 35 instead of 40, which is the existing policy. The U.S. Preventive Services Task Force does not recommend routine screening until age 50, and says it should be done every other year.

That was one of 10 eight mandates passed by the Legislature this year, three of which have been signed by the governor so far. The most significant was a requirement that large-group plans cover in vitro fertilization, which by itself is projected to increase premiums by 1 percent, or more than $200 for a family of four.

When Medicaid spending first showed signs of running over budget last summer, the Cuomo administration refrained from developing a cost-control plan as the “global cap” law provides. Instead, the governor quietly approved a major rate increase for hospitals and nursing homes – a top priority of industry lobbying groups that were backing his reelection campaign.

More evidence of the harm done by state policy is found in the federal premium data.

Large employers – most of which escape the state’s heavy-handed regulations by becoming “self-insured” – paid average single-coverage premiums that ran 7 percent higher than the national norm in 2018 (see chart).

By contrast, employers with fewer than 50 workers – which are fully exposed to Albany’s policy regime – paid premiums that were 30 percent higher than the U.S. average.

It’s clear that excessive health costs are a growing burden on New Yorkers – and that decisions made in Albany are part of the problem. The question is whether state lawmakers will start trying to make things better rather than worse.

About the Author

You may also like

The Attorney General’s MFCU SNAFU

Attorney General Letitia James' latest fight with the Trump administration focuses on New York's Medicaid Fraud Control Unit, a federally funded agency housed in James' office.

On T Read More

Healthcare Revelations in the Enacted Budget Financial Plan

The state financial plan published on June 10 disclosed key information about healthcare revenue and spending that lawmakers had not made public when approving the annual budget two weeks before.

Read More

Federal Suit Traces Medicaid Fraud to the Top of NYS Government

The Trump administration's latest salvo against Medicaid fraud takes aim at a different kind of target – two high-ranking New York officials along with a major state contractor.

A Read More

Healthcare Highlights in the New State Budget

Governor Hochul's focus on affordability seems to have skipped over the healthcare portions of the new state budget.

The deal finalized May 27 Read More

Lawmakers Consider Hiking Fees for Filling Prescriptions

UPDATE: The proposal discussed below passed the Assembly Friday evening by an unofficial vote of 133-0. Having previously been approved by the Senate, the bill will head to Governor Hochul's desk for her signature or ve Read More

Budget Deal Reportedly Earmarks $100M for 1199 and Extends MCO Tax

As Governor Hochul and legislative leaders rush to finalize the overdue state budget, outlines of some healthcare-related deals have begun to emerge from the closed-door negotiations.

Read More

Albany Wavers on Shutting Down a Medicaid Racket

As Washington threatens to crack down on fraud and abuse in New York's Medicaid program, state legislators are doing their best to demonstrate why federal intervention is needed.

A Read More

Getting to the Bottom of the 340B Drug Discount Boondoggle

Some of New York's largest and most prosperous hospitals are reporting rapidly growing amounts of revenue from pharmacy sales – most of it apparently flowing from a controversial drug discount program known as 340B. Read More