WHAT YOU’LL LEARN IN THIS REPORT:

- The Health Care Reform Act (HCRA) began as an effort to bring market-driven change and efficiency to New York’s hospital industry, but has evolved into little more than a revenue-generating mechanism in support of the status quo.

- HCRA’s combined surcharges on health insurance and cigarettes have more than quadrupled in size over the past 24 years, and now rank as the state’s third-largest revenue source.

- HCRA’s insurance taxes add approximately $440 per person to the cost of private health coverage, or $1,760 for a family of four.

- HCRA’s insurance taxes make no adjustment for ability to pay, hitting working- and middle-class consumers as hard as the wealthy.

- Three-quarters of HCRA funds now flow into the Medicaid budget, accounting for 18 percent of the state’s contribution to a program that was formerly financed with general revenues.

- Other HCRA funds pay for questionable purposes that do not directly contribute to improving patient care or broadening coverage – such as subsidizing doctors’ malpractice costs and boosting health-care workers’ pay and benefits.

- Belying its name, the $1.1 billion HCRA-supported Indigent Care Pool distributes money to hospitals based not on how much free care they provide to the uninsured, but mostly on how much aid they have received in the past.

EXECUTIVE SUMMARY

Faced with a $2.5 billion deficit in the Medicaid budget, Governor Andrew Cuomo has floated the idea of closing the gap in part with “additional industry revenue.” This raises concern that lawmakers will again hike New York’s already heavy taxes on health insurance – and deepen the state’s addiction to an unhealthy source of revenue.

It’s a counterproductive habit that makes premiums less affordable for consumers and employers while fueling waste and inefficiency in the state’s medical system. Lawmakers should be weaning the state away from taxes on health care, not increasing the dose.

The two biggest levies date back to 1996, when New York State deregulated hospital fees in hopes that market forces would tame spiraling health care costs. In the name of smoothing the transition, the law provided hospitals with extra aid financed with special taxes on health plans and medical services.

Almost immediately, the state’s per capita hospital spending and employment levels – which had been the highest in the nation – gradually moved closer to the norm, saving billions of dollars for New York taxpayers and consumers.

It was a turning point that then-Governor George Pataki aptly dubbed the Health Care Reform Act, also known as HCRA (“hick-ruh”).

Twenty-four years later, however, it’s hard to find any “reform” left in the Health Care Reform Act. Beginning with its first renewal in 1999, HCRA has transformed from a vehicle for positive change into a revenue source for the status quo.

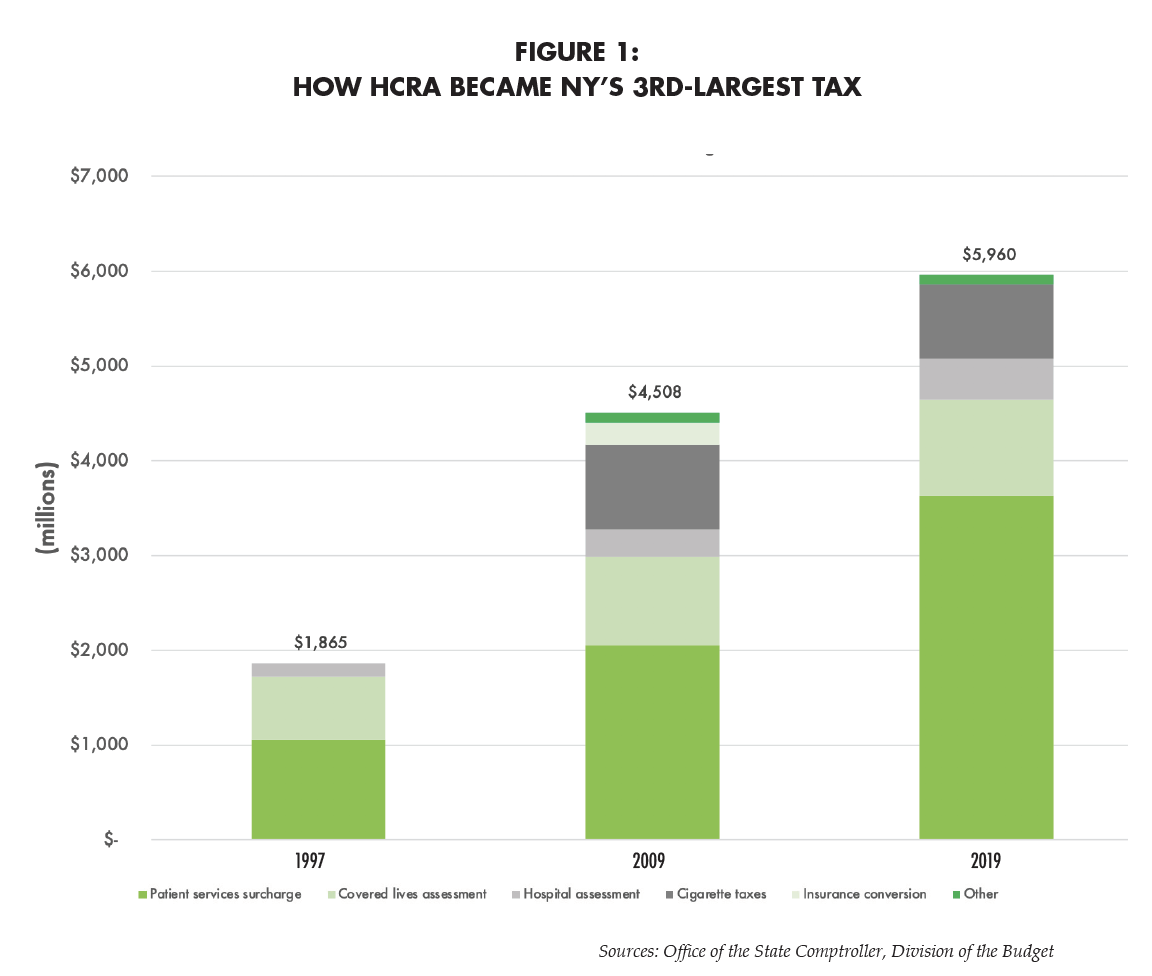

Rather than phasing out the original taxes, lawmakers repeatedly extended them, hiked them, and added new ones. HCRA receipts now total $6.2 billion per year, making them the third largest revenue source in the nation’s highest-taxed state.

Collected in ways that hide them from public view, the taxes add approximately $1,760 to the average insurance costs for a family of four, compounding the pain of skyrocketing premiums and deductibles. And the HCRA taxes make no allowance for ability to pay – squeezing just as much from families in the working and middle classes as from the wealthy.

Nor is all the money spent effectively. State lawmakers have funneled HCRA funds into programs that have little or nothing to do with direct patient care – such as subsidizing doctors’ malpractice premiums, boosting pay and benefits for health-care workers, or simply plugging holes in the state budget.

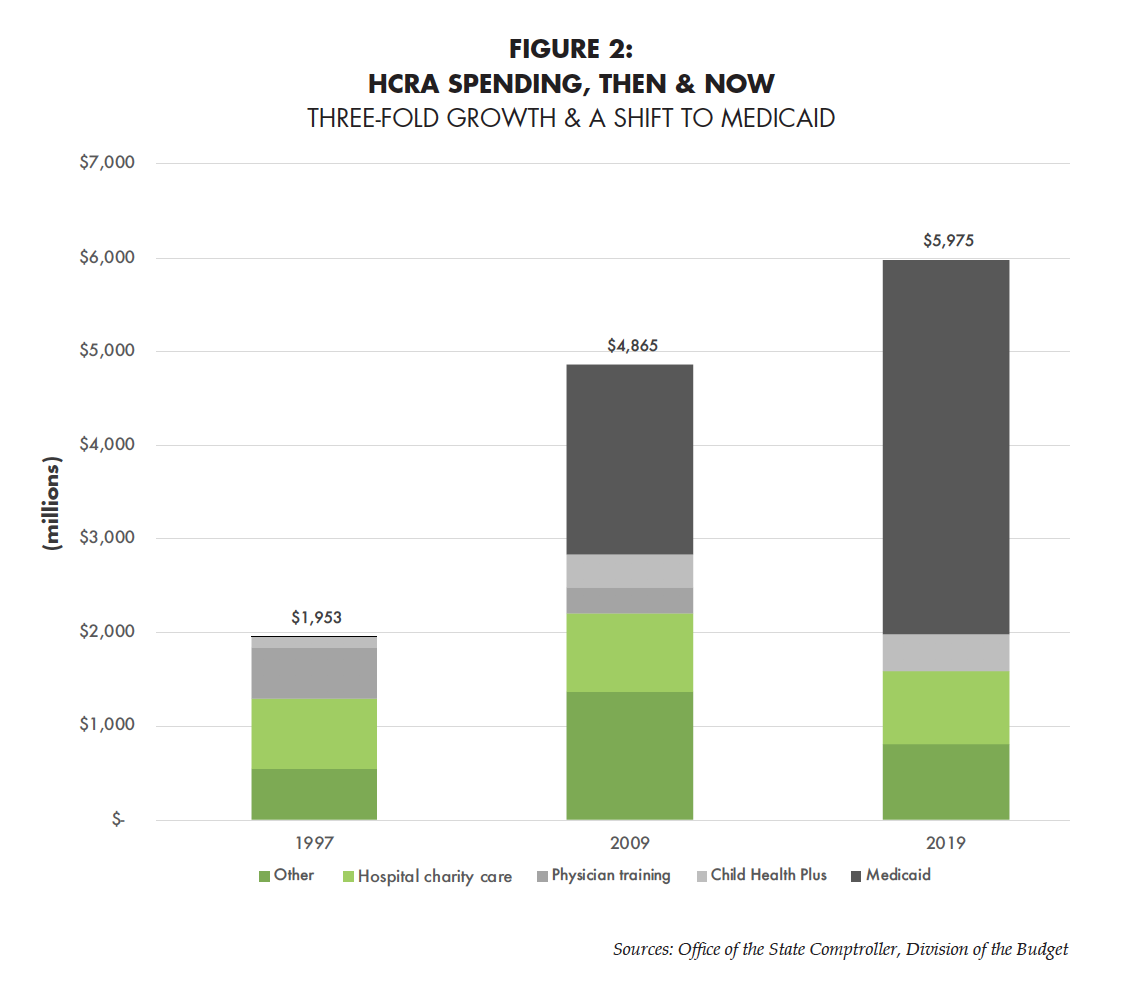

Today, three-quarters of HCRA monies flow into the state’s Medicaid health plan for the poor. They cover 18 percent of the state’s cost for the program, which formerly was entirely financed with broad-based tax revenues.

Delivering safety-net care to the uninsured – which was one of the law’s original purposes – accounts for an ever-smaller share of the HCRA budget. Even that amount is spent haphazardly at best.

An analysis of HCRA’s so-called Indigent Care Pool, which distributes about $1 billion a year, shows that it pays some relatively well-off hospitals two, three, or four times the cost of the free care that they provide, while safety-net institutions doing the bulk of the charity work get pennies on the dollar.

In the name of “reform,” in short, New Yorkers struggling to afford health coverage are paying billions in regressive taxes to finance programs that do little to improve health care – and, in some cases, enable dysfunction.

Many of the law’s key provisions, including its major taxes, are due to expire on December 31, 2020, putting the future of HCRA on the table as state lawmakers try to balance the budget for the fiscal year that starts April 1.

Governor Andrew Cuomo has appointed a Medicaid Redesign Team to develop a plan for closing that gap – and told them that “additional industry revenue” is one of the options they should consider.

Immediately reducing or eliminating HCRA taxes might be impractical in the face of a $2.5 billion Medicaid deficit. At the least, lawmakers should refrain from hiking the HCRA levies, and instead focus on spending the state’s existing health-care dollars more efficiently and prudently.

In the longer term, New York needs to kick its health tax habit.

THE HISTORY OF HCRA

The Health Care Reform Act of 1996 grew out of an earlier mega-statute that had gone badly awry: the New York Prospective Hospital Reimbursement Methodology, or NYPHRM (“nie-frum”).

Approved in 1982 and first implemented in 1983, NYPHRM was a system of price regulation that dictated the fees charged by almost every hospital in the state. It was mandatory for almost all health insurers, the exception being health maintenance organizations (HMOs), which were a small but growing phenomenon.

Under NYPHRM, regulators in the state Health Department established a basic price per day for each of the hundreds of possible medical procedures a hospital might perform, which they then adjusted upward or downward for the patient’s degree of illness, the region’s cost of living, the hospital’s financial condition, and other factors.

Fees also varied based on who was paying the bill. For-profit commercial insurers were required to pay the highest rates. Next down the ladder was Empire Blue Cross & Blue Shield, a nonprofit company considered the state’s “insurer of last resort” because it accepted high-risk customers. Medicare paid less than Empire, and Medicaid paid the lowest fees of all. Hospitals were expected to use profits from privately insured patients to offset losses on Medicaid.

Beyond this cross-subsidization, NYPHRM set aside pools of money to support charity care for the uninsured, on-the-job training for young physicians (known as graduate medical education), insurance for low-income kids through Child Health Plus, and a laundry list of other “public goods.” To raise money for these public goods pools, insurers paid a tax on inpatient hospital bills averaging 5.5 percent, and hospitals paid a 1 percent tax on their inpatient revenue.[1]

NYPHRM was a massively complicated system that was the subject of continual political battles at the state Capitol, as employers and insurers fought to keep a lid on rising costs and hospitals and other players angled to increase their revenue. Yet most players on all sides took for granted that the system was generally working to hold down hospital spending in New York.

That assumption turned out to be wrong. In March 1994, health consultant John Rodat – a former Health Department regulator – published a study that turned conventional wisdom on its head. Analyzing federal data, Rodat showed that New York’s per capita hospital spending rate was the second-highest in the nation – and growing faster than the national average – even as the state’s spending on physician care was below the norm.[2]

Rodat further showed that the rate at which New Yorkers were hospitalized, and the average number of days per patient, were both the highest of 16 states for which comparable data were available – symptoms of inefficiency that a top-down regulatory system had failed to control.[3]

“While New York’s policy of centralized control of hospital payments may have been relatively effective in the past, it cannot be an effective foundation for the future,” he wrote.[4]

Awoken to these unintended consequences, employers, labor unions, insurers, and advocates for the poor began agitating for reform – a cause that became a priority for newly elected Governor George Pataki after he took office in 1995. He signed the Health Care Reform Act into law on September 12, 1996, and it took effect on January 1, 1997.[5]

How HCRA originally worked

The central thrust of the new law was to deregulate fees paid by private health plans – which were most of hospitals’ collective revenue – thus exposing them to competitive pressure that would contain costs. The belief was that negotiations driven by market forces would lead to a better balance between what hospitals needed in revenue, and what employers and insurers could afford to pay.

As a report from Public Policy Institute said in 1998, the rationale “was that the marketplace would help achieve what government lacked the political will and ability to do by itself – force greater efficiencies and reduce hospital excess capacity.”[6]

The statute’s “statement of legislative intent” declared: “The NYPHRM system does not provide the economic discipline to contain costs, affects a shrinking proportion of the market, maintains excess hospital capacity, provides incentives to train too many physicians and inappropriately targets funds for uncompensated care.”[7]

The statement further said that the new law would “promote competition in the health care marketplace by increasing reliance on market incentives while reducing the role of regulation.”[8]

At the same time, however, HCRA continued subsidies for charity care and physician training – albeit at lower levels – along with other programs formerly supported by NYPHRM. To raise money for newly established “public goods” pools, the law levied two new taxes on insurance:

- An 8.18 percent “patient services surcharge” on hospital, clinic, and laboratory bills to private insurers (exempting physicians and other providers). Medicaid would pay the surcharge, too, at a rate of 5.98 percent. This would collect just over $1 billion annually in its first years, which was earmarked for charity care and other public health programs.

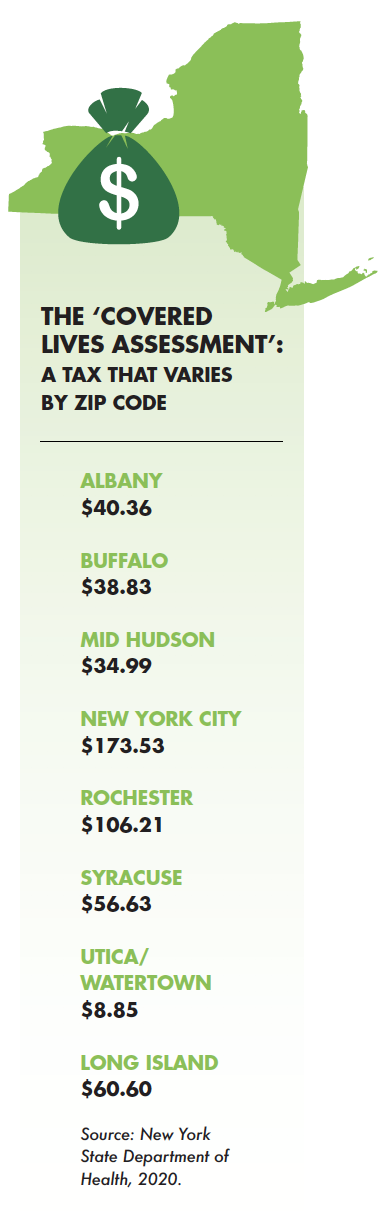

- A flat per-customer fee, or “covered lives assessment,” on private insurance. Most of the $665 million collected went to fund graduate medical education. In a striking departure from usual practice, the rate of this tax was not consistent throughout the state, but varied from place to place based on the number and size of teaching hospitals in each area. To start, it ranged from a high of $116.75 per insured in New York City to a low of $4.69 in the Utica-Watertown region.

The money flowed not to the state, but to a private contractor hired as a “pool administrator.” This contractor – which has been Excellus BlueCross BlueShield of Rochester for the entire history of the law – not only collected the funds, but took charge of distributing them to hospitals according formulas established by the state.[9]

Some of the proceeds were also used for other programs, such as expanding Child Health Plus and financing poison control centers.

HCRA’s evolution

As HCRA 1996 neared its expiration date at the end of 1999, employers and insurers lobbied for the taxes to be rolled back or repealed. They argued that health insurance taxes existed on this scale in no other state, and that they undercut the reform goals of affordability and efficiency. They questioned the need to subsidize physician education given that half the doctors trained in New York were leaving for other states. They further noted that deregulation had not triggered a wave of hospital closings or layoffs, contrary to the fears of industry officials.[10]

Ultimately, these arguments fell on deaf ears.

In early 2000, Pataki and the Legislature agreed on a four-year extension that not only preserved HCRA’s taxing and spending scheme, but dramatically expanded it – setting a pattern that would continue through the next 12 years.

Here is a summary of the key changes:[11]

2000: At Pataki’s behest, lawmakers enlarged HCRA with two new revenue streams: a portion of proceeds from a multistate legal settlement with tobacco companies, of which New York was expected to collect $25 billion over 25 years, and the near-doubling of the state tax on cigarettes, from 56 cents to $1.11 per pack.

They used the new money, in part, to launch two new insurance programs – Family Health Plus for low-income parents with children, and Healthy New York, for self-employed individuals and small businesses. They also boosted subsidies to hospitals for charity care, and ramped up spending on anti-smoking programs, among other increases.

In an especially significant move, they also drew on $800 million in HCRA funds to finance existing programs, such as Medicaid and Elderly Pharmaceutical Insurance Coverage (EPIC) – in effect, using dollars nominally dedicated to healthcare to plug holes in the overall budget.

2002: With the state’s finances reeling in the aftermath of 9/11, Pataki might have been expected to call for cuts to healthcare spending. Instead, he proposed – and lawmakers approved – an extra $2.2 billion in Medicaid spending over four years ($900 million from the state and $1.3 billion in federal matching funds) specifically dedicated to higher wages and benefits for rank-and-file health-care workers.

The extension also increased the share of HCRA funding used to cover existing Medicaid expenses – and thereby balance the budget – to $1 billion a year.

To pay for these outlays, lawmakers levied an additional cigarette tax hike (from $1.11 to $1.50 per pack) and used increased federal Medicaid funding from Washington.

In another precedent-setting move, lawmakers also relied on the anticipated proceeds from the conversion of Empire Blue Cross & Blue Shield to for-profit status. By law, corporations that make such a move must compensate the public for the value of assets accumulated while enjoying tax protection as a non-profit. Across the country, this is often accomplished by selling stock in the new company and transferring all or most of the proceeds to a charitable foundation.

With HCRA 2000, however, lawmakers opted for the state treasury to receive most proceeds from the conversion of Empire, which would ultimately exceed $1 billion, setting aside 5 percent for what became the New York State Health Foundation.

Even by Albany standards, this was an unprecedented “one-shot” – the notorious budgeting practice of using a short-term windfall to finance ongoing expenses. Yet lawmakers would repeat the pattern with the conversions of other insurance companies in the years ahead.

The framework of HCRA 2000 emerged from closed-door negotiations between the governor and healthcare labor leader Dennis Rivera, whose politically influential union 1199 endorsed Pataki for reelection a few months later.[12]

2003: The very next year, facing continuing deficits in the post-9/11 recession, lawmakers boosted HCRA funding again with increases in both the patient services surcharge (from 8.18 to 8.85 percent) and the covered lives assessment; proceeds from more insurance company conversions; and the “securitization” of the tobacco lawsuit settlement, in which the state swapped its ongoing annual payments in return for a lump-sum payout.

2005: Lawmakers again hiked the patient services surcharge (to 8.85 to 8.95 percent) and the covered lives assessment, as well as sweeping in $2.7 billion in receipts from insurer conversions. On the spending side, they established the Healthcare Efficiency and Affordability Law for New Yorkers, or HEAL-NY, which offered $1 billion in grants to providers.

2007: In Governor Eliot Spitzer’s first year, lawmakers hiked the covered lives assessment by $75 million and collected $1 billion from insurer conversions. On the spending side, they raised the eligibility ceiling for Child Health Plus from 250 percent to 400 percent of the federal poverty level and established a fund for stem cell research.

2008: As part of Governor David Paterson’s first budget, lawmakers increased the cigarette tax from $1.50 to $2.75 and boosted the covered lives assessment by $70 million.

2009: Lawmakers increased the covered lives assessment by another $120 million and hiked the patient services surcharge from 8.95 to 9.63 percent. They also levied a new $399 million assessment on insurance companies to cover the costs of Healthy New York and HMO Direct Pay, two programs formerly financed by HCRA.

2010: Lawmakers increased the state cigarette tax to $4.35 per pack from $2.75.

2011: As part of Governor Cuomo’s first budget, lawmakers levied a $40 million hospital quality contribution assessment on charges for inpatient obstetrical services, to finance a compensation program for babies injured in childbirth.

To summarize, lawmakers hiked the original HCRA taxes (or imposed new ones) 14 times in 12 years – more than quadrupling annual revenues – even as they used up several billion dollars’ worth of windfalls from insurance conversions and tobacco litigation. (See Figure 1.)

As revenues grew, the spending side of HCRA changed, too – and drifted ever further from the law’s original purpose.

The pool earmarked for graduate medical education, one of the two core programs of HCRA 1996, has been left empty even as the tax levied to fill it, the covered lives assessment, brings in more money than ever.

The other core program of the HCRA 1996 – subsidizing hospital care for the indigent and uninsured – continues at about $1 billion a year, despite the major decline in New York’s uninsured rate since the advent of the Affordable Care Act. The money is distributed so haphazardly that many of neediest “safety net” hospitals receive less support, proportionally, than hospitals serving mostly privately insured patients. (See “Indigent care dollars follow institutions, not patients,” below.)

Major public health initiatives that HCRA formerly supported – Family Health Plus, Child Health Plus, EPIC, Healthy New York – have either been fully or partially replaced by the ACA and its federal funding. Yet the HCRA taxes enacted to support those programs have gone up, not down.

Other programs – including tobacco control efforts launched with much fanfare in HCRA 2000 – have been cut, shifted back to the general state budget, or both.

Today, HCRA primarily serves as a vehicle for funding Medicaid, a program formerly financed entirely with general tax revenues. This year, HCRA is due to transfer more than three-quarters of its revenue, or $4.7 billion, to the Medicaid budget, accounting for 18 percent of the state’s share of the program. (See Figure 2)

Did it work?

Measured against the central goal of the original law – to control spiraling hospital costs – HCRA has shown at least some success.

In the early 1990s, at the end of the NYPHRM era, New York’s per capita spending on hospitals was rising faster than in the rest of the country. As of 1994, its hospital spending rate climbed to be the costliest among the 50 states and 28 percent higher than the national average. Both of those measures were the same in 1996, when Pataki signed HCRA into law.

But starting in 1997, the very first year the law took effect, New York’s per capita spending began moving closer to the national average (Figure 3). As of 2014, the most recent year for which federal data are available, New York’s hospital spending ranked 13th among the 50 states.[13]

However, its spending remained 18 percent higher than the national average, leaving substantial room for further improvement.

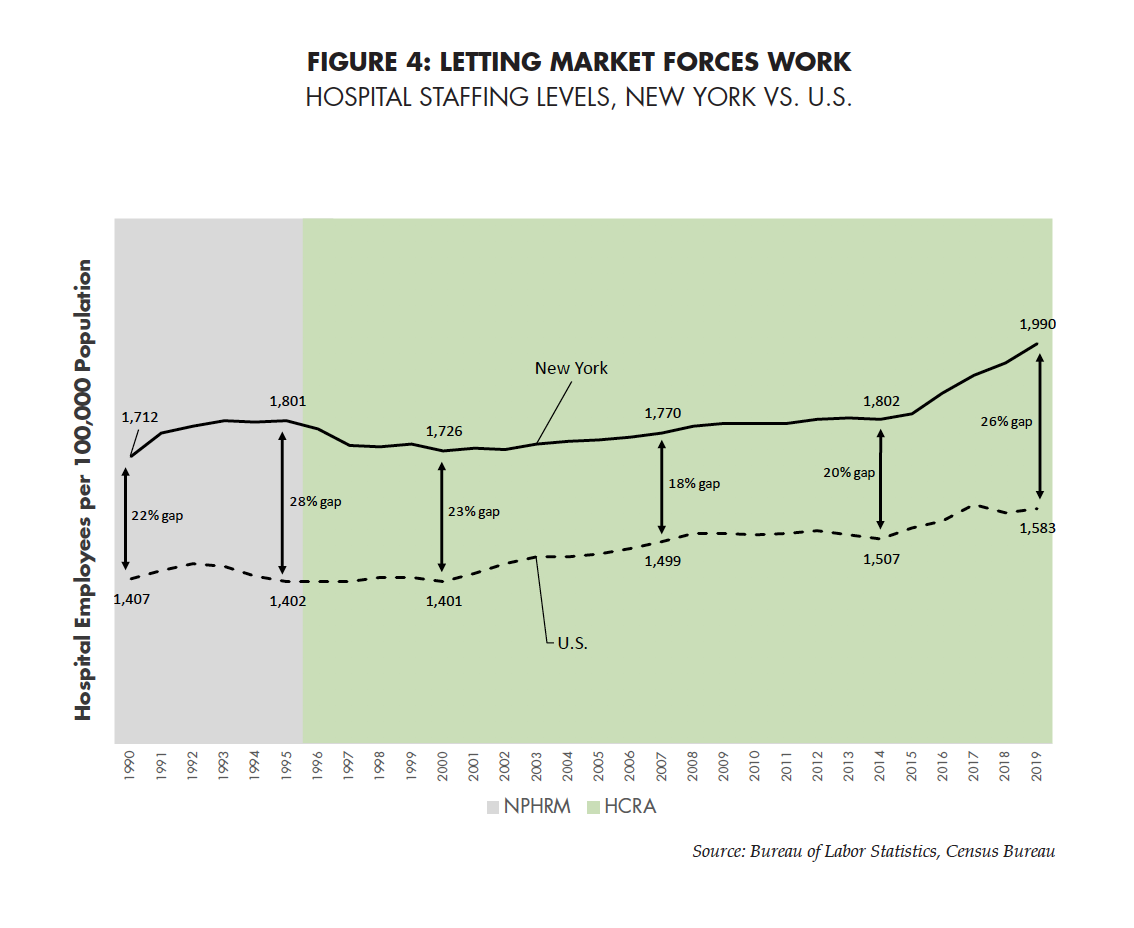

Another sign of progress in the early years of HCRA could be found in employment data. As of 1995, New York had 1,800 hospital workers for every 100,000 people, a rate 28 percent higher than the U.S. norm. By 2008, 12 years after deregulation, the New York’s rate had dropped to 17 percent above national average at 1,786 per 100,000.

More recently, New York’s hospital employment has surged to new high of 1,990 per 100,000 for 2019, and the gap between the state and the country as a whole was almost back to its pre-HCRA peak.[14] (See Figure 4)

To be sure, New York’s high hospital spending is partly driven by the state’s high cost of living – including wages, real estate prices, energy costs, taxes, and other factors that are far above the national norm. However, New York’s hospitals also lag by measures which they should be able to control.

Take, for example, the average length of inpatient stays, a basic measure of efficiency. New York hospitals’ average in 2016 was 6.7 days, the 8th highest among the 50 states. The national norm hasn’t been that high since 1994.[15]

Despite high spending and employment, New York’s hospitals also fall short by some measures of quality. In a federal report card that grades hospitals on a scale of one to five stars – based on 64 quality measures – New York’s hospitals collectively receive the lowest average score in the country.[16]

Although industry officials have disputed the methodology of this report card, there is little question that New York’s hospitals collectively rate poorly on important benchmarks. For example, according to federal data gathered through June 2018, 15.8 percent of the state’s hospital inpatients were readmitted within 30 days, the second-highest rate among the 50 states.[17]

NEW YORK’S UNDERCOVER HEALTHCARE TAX

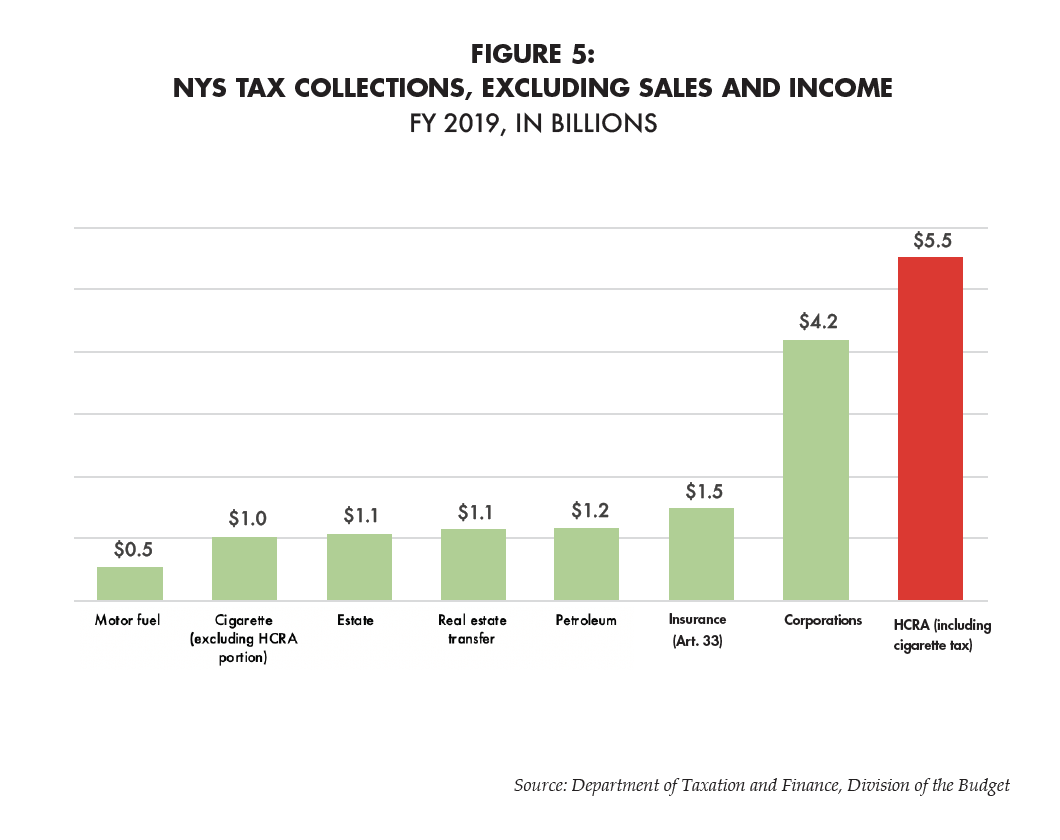

From their relatively modest beginnings, HCRA’s insurance surcharges have mushroomed into the state’s third-largest tax – behind income and sales taxes – and the single largest tax on business.[18] (See Figure 5).

With combined revenues of almost $6.2 billion in fiscal year 2020, HCRA collections surpass the petroleum, estate, the real estate transfer and motor fuel taxes combined. The two taxes on health insurance make up the bulk of that amount, or $4.9 billion.

That cost ultimately falls on the 11.2 million New Yorkers with commercial health plans and their employers. The average bite of HCRA insurance taxes is $440 per person, or $1,760 for a family of four.

The two main taxes – the covered lives assessment and the patient services surcharge – add substantially to the cost of health insurance at a time when many New York families and businesses are struggling to afford premiums.

As a share of median silver-level individual premiums for 2019, the covered lives assessment ranges from 0.12 percent in the Utica/North Country region to 2.20 percent in New York City. (See Table 1).

The patient services surcharge adds another 3.71 percent, according to a 2015 analysis by Excellus Blue Cross Blue Shield of Rochester.[19]

Taken together, the combined effect of HCRA’s insurance surcharges amounts to almost 6 percent for New York City consumers – roughly the cost of an extra three weeks’ coverage per year.

These taxes apply to everyone with non-Medicare coverage. Even the government-funded Medicaid program pays the patient services surcharge, albeit at the lower rate of 7.04 percent.

By making health insurance less affordable, HCRA taxes work at cross purposes with the policy goal of moving toward universal coverage.

For now, the uninsured rate is declining, both in New York and nationwide.[20] This is largely due to the massive expansion of Medicaid under President Obama’s Affordable Care Act. This progress could be undone if the ACA is overturned by the courts or if the employer-sponsored insurance market sees excessive premium increases.

In any case, HCRA taxes tend to make things worse. They add to insurance costs, which increases pressure for employers to drop coverage. This creates higher demand for Medicaid and charity care, more financial losses for hospitals, redoubled demand for state funding, and upward pressure on HCRA taxes – the same vicious cycle seen under NYPHRM.

HCRA taxes are also regressive, affecting all New Yorkers with private health insurance without regard to their ability to pay.

The 9.63 percent patient services surcharge, which comes out of what insurers pay to hospitals and clinics, perversely imposes the highest costs on the sickest patients, costs which must then be absorbed by their insurers, employers, and coworkers. The covered lives assessment, which is a flat fee for each insured person in any given region, costs the same for the retail clerk or fast-food workers as for a Wall Street executive.

The covered lives assessment varies dramatically from part of the state to another, ranging from $8.85 per individual in the Utica-Watertown region to $173.53 in the five boroughs of New York City – a difference of 1,861 percent.[21]

State lawmakers designed the assessment this way to avoid compelling Utica residents to subsidize teaching hospitals in New York City that they would rarely use. Now that HCRA funding for graduate medical education has all but disappeared, the assessment revenue is mostly going to Medicaid and other broad, statewide programs. Residents of New York City – or, for that matter, Rochester, where the rate is $106.21 – have a right to ask why they should pay so much more.

Another undesirable feature of the HCRA surcharges is that they are hidden from public view. Consumers never see an annual statement of their cost. Instead, they’re invisibly baked into insurance contributions routinely deducted from their paychecks. After a major procedure, consumers might notice the patient services surcharge buried among the many charges itemized on a hospital bill, but that figure has no clear relation to their copayment or coinsurance.

Still, the tax has an undeniable effect – in driving up health premiums, adding to the cost of hiring for business, and shifting more compensation away from wages and into benefits.

Cigarette taxes that finance HCRA are also regressive – in that lower-income people are more likely to smoke – but can come with the offsetting benefit of discouraging people from picking up the habit, particularly children and teenagers with limited money to spend.

However, New York’s second-highest-in-the-nation state tax, at $4.35 per pack, has led to widespread evasion and black-market trafficking, which both diminishes state revenue and undercuts public health goals.[22]

This is especially true in New York City, where a local levy brings the total tax to $5.85 per pack. Smugglers known as “buttleggers” can buy cigarettes in Virginia (where the tax is 30 cents a pack), sell them on the streets of New York at a steep discount off the legal price, and still turn hefty profits.

Among those known to have partaken in this lucrative business are organized crime syndicates, street gangs, and terrorist groups.[23]

Meanwhile, the state no longer uses HCRA funds to finance its anti-smoking programs. Instead, those programs were shifted to the Health Department’s general budget and reduced by more than half since 2008.[24]

By repealing or phasing out HCRA taxes, Governor Cuomo and the Legislature could both make health insurance more affordable and make New York’s tax code less punishing for the middle class.

QUESTIONABLE SPENDING

Not all the programs financed through HCRA have lived up to the law’s promise of “reform.” Some, in fact, have been as regressive and counterproductive as the taxes that pay for them.

Problems with HCRA’s spending priorities date back to the law’s origins, when nearly all the money was devoted to two programs aimed at hospitals: a subsidy for graduate medical education and compensation for free care provided to the uninsured and indigent. The former fulfilled a questionable need; the second was spent in ways that prioritized support for institutions rather than patients.

Graduate medical education, or GME, refers to costs incurred by teaching hospitals for training young doctors. Critics questioned this part of HCRA from the beginning, noting that the state’s academic medical centers were turning out more graduates than New York needed (causing many to leave the state to practice); that doctors-in-training provide low-cost labor that offsets the expense of training them; and that teaching hospitals already collected substantial GME funding through Medicare.[25]

Lawmakers phased out the GME portion of HCRA during a budget crisis triggered by the Great Recession in 2008 and 2009.[26] Yet the tax created to finance GME – the covered lives assessment – continues.

Lawmakers phased out the GME portion of HCRA during a budget crisis triggered by the Great Recession in 2008 and 2009.[26] Yet the tax created to finance GME – the covered lives assessment – continues.

As for HCRA’s charity care program, known as the Indigent Care Pool, criticism has mainly focused not on the purpose, but on how the money is distributed.

Ideally, indigent care dollars would “follow the patient” – that is, reimburse providers for delivering specific care to specific people.

The Indigent Care Pool has never worked that way. Instead, it makes lump-sum grants to hospitals that have provided charity care in the past, or that serve low-income neighborhoods – with no requirement that hospitals use the money for treatment. This is analogous to replacing food stamps with checks written to grocery stores, without requiring stores to account for how much food they give away.

Plus, the size of an indigent-care grant relates loosely, at best, to how much charity care a hospital provides. Under the current version of the formula, some hospitals are receiving several times more than the expenses they incur for treating the uninsured, while safety-net institutions get pennies on the dollar. (See “Indigent care dollars follow institutions, not patients,” below.)

As lawmakers expanded HCRA, they devoted a portion of the new revenues to programs that offered state-subsidized, low-cost health coverage for different groups of the uninsured or underinsured. These include Family Health Plus, for low-income parents; Healthy New York, for small businesses and the self-employed; Child Health Plus, for low-income children; and Elderly Pharmaceutical Insurance Coverage, or EPIC, for low-income elderly.

It should be noted that Child Health Plus and EPIC were pre-existing programs that were shifted into HCRA and expanded. In effect, moving them into HCRA helped balance the state budget by freeing up general tax revenues to pay other costs.

Of the four programs, only Child Health Plus continues as a major expense. The EPIC program shrank with the advent of drug coverage through Medicare Part D. Family Health Plus was eliminated, and Healthy New York was scaled back, when federally subsidized insurance became available through the ACA. Despite these cutbacks, the HCRA taxes originally levied to support these programs continue at higher rates than ever.

As lawmakers fueled HCRA with billions in revenue from tobacco lawsuits and cigarette taxes, they set aside money for smoking prevention and cessation efforts. That spending peaked in fiscal year 2008 at $80 million, or 14 percent of the revenues from cigarette taxes.[27]

Since then, the program has been cut by half and shifted out of HCRA and into the Health Department’s regular budget – even as the cigarette tax was hiked two more times, in 2008 and 2010. As a result, the state with the highest tax on cigarettes ranks 23rd for its per capita spending on anti-smoking programs, according to the Campaign for Tobacco Free Kids.[28]

Over the years, the burgeoning HCRA budget made room for long list of other programs, many of which had little or nothing to do with improving the state’s healthcare system.

Workforce recruitment and retention: Starting in 2002, the state used $2.2 billion in HCRA funds over four years to boost the pay and benefits of non-supervisory health-care workers. That amount of money was enough to buy four years’ worth of health coverage, at $5,000 a person, for 110,000 uninsured New Yorkers. To this day, HCRA spends $197 million a year on “workforce recruitment and retention” for personal care workers.[29]

Physician excess medical malpractice: HCRA earmarks almost $130 million a year to subsidize medical malpractice insurance provided by participating hospitals – which was justified as necessary to prevent soaring liability premiums from driving doctors out of the state. Whether high premiums are caused by a broken litigation system or by extraordinary levels of physician negligence, shifting part of the cost to taxpayers solves nothing.

Pork barrel spending: For many years, millions of dollars in HCRA money were set aside annually in “priority pools” to be spent at the discretion of the top leaders in the Assembly and Senate. In the early 2000s, then-Assembly Speaker Sheldon Silver directed $500,000 of this money to an oncologist who, in turn, gave Silver the names of asbestos patients for lucrative lawsuits – a scheme that figured in Silver’s 2015 conviction on federal corruption charges. The judge who heard the case called the lack of oversight surrounding the two HCRA grants “shocking.”[30] The balance in these pools dropped to zero as of 2012.[31]

While some smaller HCRA-funded programs continue, the law now serves mostly as a revenue-generating vehicle for the state’s Medicaid program. In the 2019-20 fiscal year, HCRA is due to transfer $3.8 billion, or 61 percent of its funds, to the Health Department’s Medicaid account.[32]

Factor in another $892 million in scheduled spending from the Indigent Care Pool – which flows through Medicaid to draw down matching federal funds – and the share devoted to Medicaid amounts to 76 percent.

All told, HCRA funding now pays almost one-fifth of the state’s share of the Medicaid budget.

HCRA has thus played a role in financing the rapid growth of Medicaid, which has added 1.2 million recipients since 2011 and helped drive the state’s uninsured rate to an all-time low of 5.4 percent for 2018.[33]

However, hidden, regressive taxes on working New Yorkers are the wrong way to finance an ever-larger entitlement program.

A better approach would be to squeeze more efficiency from New York’s Medicaid program. As of 2017, New York’s Medicaid spending per recipient was 36 percent higher than the national average. Narrowing that gap to 20 percent would more than save enough to offset the elimination of HCRA’s contribution to the program.

As for other programs currently financed with HCRA surcharges, none is so crucial as to justify further adding to the cost of health insurance. They should be financed with existing, broad-based revenues or eliminated altogether.

Indigent care dollars follow institutions, not patients

From its beginnings in 1996, a central declared purpose of the Health Care Reform Act has been to reimburse hospitals, at least partially, for providing free care to the indigent and uninsured.

The need for such support is clear. Despite recent progress in reducing the uninsured rate, 5.4 percent of New Yorkers, or about 1 million people, lack coverage of any kind.[34] When these patients seek critical care, hospitals are legally obliged to treat them regardless of ability to pay. Some institutions serving lower-income communities annually rack up tens of millions of dollars in unpaid bills.

Failing to compensate safety-net hospitals for this service would jeopardize their financial survival – and the healthcare of hundreds of thousands of New Yorkers.

Harder to justify, however, is the state’s methodology for fulfilling this need.

Throughout its 24-year history, the Indigent Care Pool has distributed money using arcane formulas in which the amount of free care a hospital provides is just one of many factors, and not necessarily the most important.

As a result – as the Commission on the Public’s Health System, the Community Service Society, and other critics have long argued – the system overcompensates hospitals serving relatively affluent communities while shortchanging the safety-net institutions where the need is greatest.

Despite three attempts at reform over the past 12 years, this critique remains as valid as ever today.

An examination of pool distributions for 2018 shows that the amount of money a hospital receives usually bears no relation to how much free care that hospital provides. Some institutions receive significantly more than the value of their charity care, while others get pennies on the dollar.[35]

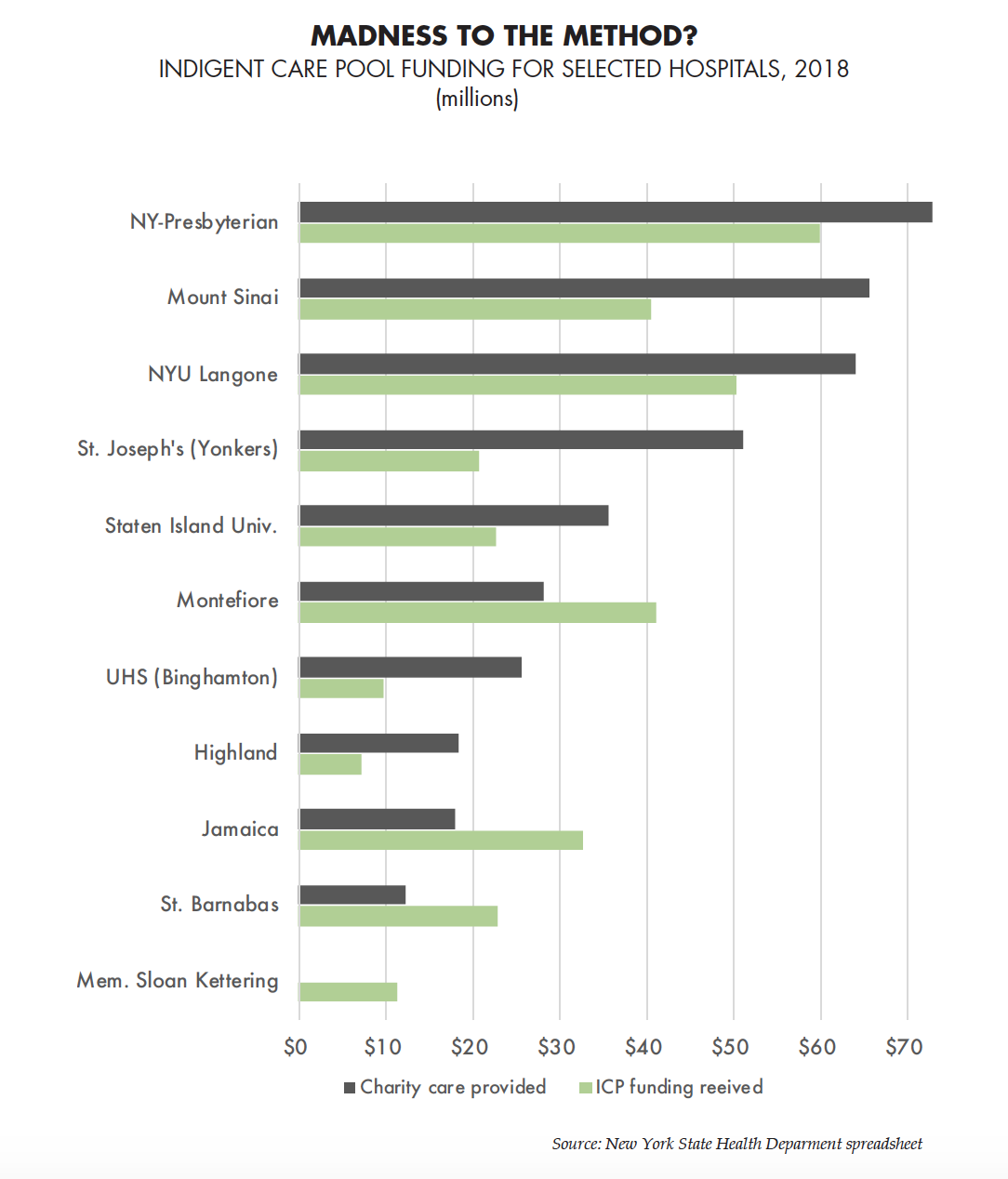

St. Joseph’s Hospital in Yonkers, for example, provided $51 million in free care in 2018 and received $21 million from the Indigent Care Pool, a reimbursement rate of 40 percent. Jamaica Hospital Medical Center in Queens, by contrast, provided $18 million in free care and received $33 million from the pool, a reimbursement rate of 181 percent.

Meanwhile, some hospitals with net charity care expenditures of zero (according the Health Department’s calculations) nonetheless collected substantial grants – including $11 million to Memorial Sloan Kettering Cancer Center.

In fact, there was small negative correlation between the neediness of a hospital’s patient population and the generosity of its payout from the Indigent Care Pool. Hospitals serving a higher percentage of Medicaid patients tend to be reimbursed for a lower percentage of their uncompensated care – a reverse-Robin Hood effect.

These seemingly topsy-turvy numbers were no accident, but the result of a formula most recently overhauled in 2013. To understand how that formula functions, some historical context is necessary.

First, pre-2013 versions of the Indigent Care Pool were designed to compensate not just services provided to uninsured patients, but also “bad debt” – the unpaid bills of patient who had coverage but could not afford or simply failed to pay their share of the cost. Compensation for bad debt flowed mainly to hospitals with large numbers of insured patients.

Second, since 2009, the pool also earmarked extra money for charity care provided by academic medical centers – the result of a budget fix in which the former pool for graduate medical education was folded into the Indigent Care Pool as a way of maximizing federal Medicaid revenue.

Third, lawmakers budget separate allocations within the Indigent Care Pool for private and government-owned hospitals, with the latter group receiving proportionally less.

As consumer advocates had long documented, these and other measures tended to benefit hospitals serving relatively well-off communities at the expense of safety-net institutions providing the bulk of charity care.

Yet industry representatives resisted sweeping reform, on grounds that major shifts might destabilize institutions that had come to depend on the funding.

The Community Service Society has further shown that many of the hospitals receiving indigent-care funds were not proactively offering free care to the people who needed it.[36] Instead, they were billing indigent patients for their full charges – regardless of how much indigent care funding they received – and in some cases using heavy-handed tactics to collect.

A 2007 law requires hospitals to offer charity care on a sliding scale to all uninsured patients up to 300 percent of the federal poverty level. However, the Community Service Society found most hospitals were not fully complying with the law and Health Department guidelines as of June 2010.[37]

In 2008, lawmakers required hospitals for the first time to report detailed information on the charity care they provide to the Health Department. However, this data was used to determine distribution of only 10 percent of the Indigent Care Pool.

The most recent reforms, enacted in 2013, grew out of recommendations from the Medicaid Redesign Team established by Governor Cuomo.

Citing research by the Commission on the Public’s Health System, the team’s Health Disparities Group found “little or no relationship between the actual dollars received by the hospitals [from the Indigent Care Pool] … and the amount of health care services they provided to the uninsured.” Going forward, the group wrote in its 2011 report, indigent care funding “should follow the patient.”[38]

Citing research by the Commission on the Public’s Health System, the team’s Health Disparities Group found “little or no relationship between the actual dollars received by the hospitals [from the Indigent Care Pool] … and the amount of health care services they provided to the uninsured.” Going forward, the group wrote in its 2011 report, indigent care funding “should follow the patient.”[38]

The group further warned about changes in federal regulations accompanying the Affordable Care Act, which said indigent care funding for hospitals should be based on only two factors: how much uncompensated care a hospital provides to the uninsured, and how much they lose treating Medicaid patients due to the program’s low fees. States that failed to comply would risk losing federal aid.

In response to those recommendations, lawmakers in 2013 enacted a new formula that includes no explicit provision for bad debt or for teaching hospitals – and uses only the amount of care provided to the uninsured and the Medicaid utilization rate to calculate a “nominal need” for each hospital.

However, the lawmakers added a “transition adjustment” that sharply limits how much any given hospital’s funding can change from one year to the next. As of 2018, hospitals were guaranteed to receive no less than 85 percent of what they got, on average, from 2010 through 2012. At the same time, the formula also capped increases. Public hospitals could receive at most 14.3 percent more, and voluntary hospitals 33 percent more, than their average allotment from 2010 through 2012.[39]

For most hospitals, this transition adjustment effectively made the rest of the formula irrelevant. More than half of the hospitals, or 89, were guaranteed a minimum amount that exceeded their need-based share – and, in some cases, also topped the full value of their charity care. Another 32 hospitals were capped at a maximum that was less than what they otherwise would have been entitled to, sometimes significantly so. Only 34 hospitals, or one in five, received grants as prescribed by the need-based part of the formula.

Thus, New York nominally removed bad debt and graduate medical education from its Indigent Care Pool formula – then minimized the impact of that change by adding the transition adjustment. In effect, the state has continued to reimburse hospitals as it had in the past, and diverted money from charity care to do so, while continuing to draw federal matching funds. This would seem to run afoul of the spirit, if not the letter, of federal regulations.

Meanwhile, lawmakers continued segregating the pool based on ownership. The 2018 budget allocated $994.9 million for private hospitals and $139.4 million for public-sector institutions.

Government-owned hospitals collectively delivered 48 percent of the charity care in 2018 yet received just 12 percent of the pool funding. Voluntary hospitals delivered 52 percent of the charity care and received 88 percent of the pool funding.

In 2018, the hospitals’ nominal need collectively amounted to $1.5 billion, and the Indigent Care Pool had $1.1 billion available to distribute. If the formula had simply allocated the money proportionally by need, each institution would have received about 74 cents on the dollar. Instead, private hospitals collectively received 129 percent of their nominal need, while public hospitals got just 19 percent.

Particularly hard-hit by the formula are the 11 hospitals owned and operated by New York City Health + Hospitals. Located in some of the city’s poorest neighborhoods, serving large numbers of undocumented immigrants ineligible for Medicaid, these institutions collectively provide 35 percent of the state’s charity care – and receive just 8 percent of the Indigent Care Pool funding.

Like other public hospitals, city hospitals qualify for additional streams of funding that are not available to private institutions. Even so, Health + Hospitals has required repeated infusions of extra money from the city budget and still faces chronic budget shortfalls.[40]

Even within the public and private subgroups, the transition adjustment results in vast disparities in funding.

In a comparison of 2015 distributions to two voluntary hospitals , researcher Roosa Tikkanen found that NYU Langone Medical Center served 10,650 uninsured patients, compared to just 899 for Memorial Sloan Kettering. Yet each received approximately $12 million from the Indigent Care Pool.[41]

Nor are public hospitals treated even-handedly. In 2018, Westchester Medical Center, which provided $19 million worth of free care, received an Indigent Care Pool grant of $9 million, or 47 cents on the dollar. By contrast, Bellevue Hospital Center provided $104 million worth of uncompensated care – the most in the state – and received a grant of $15 million, or 15 cents on the dollar.

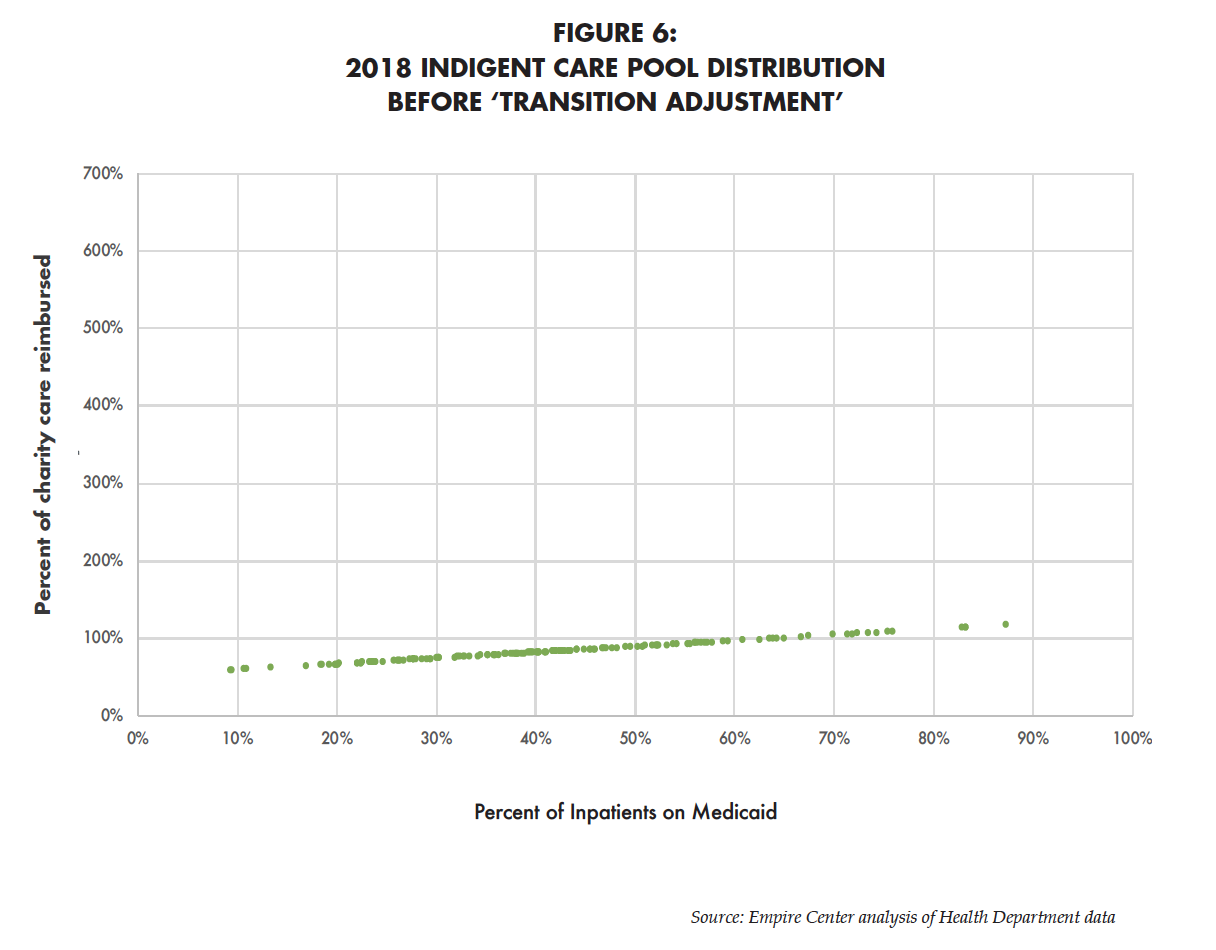

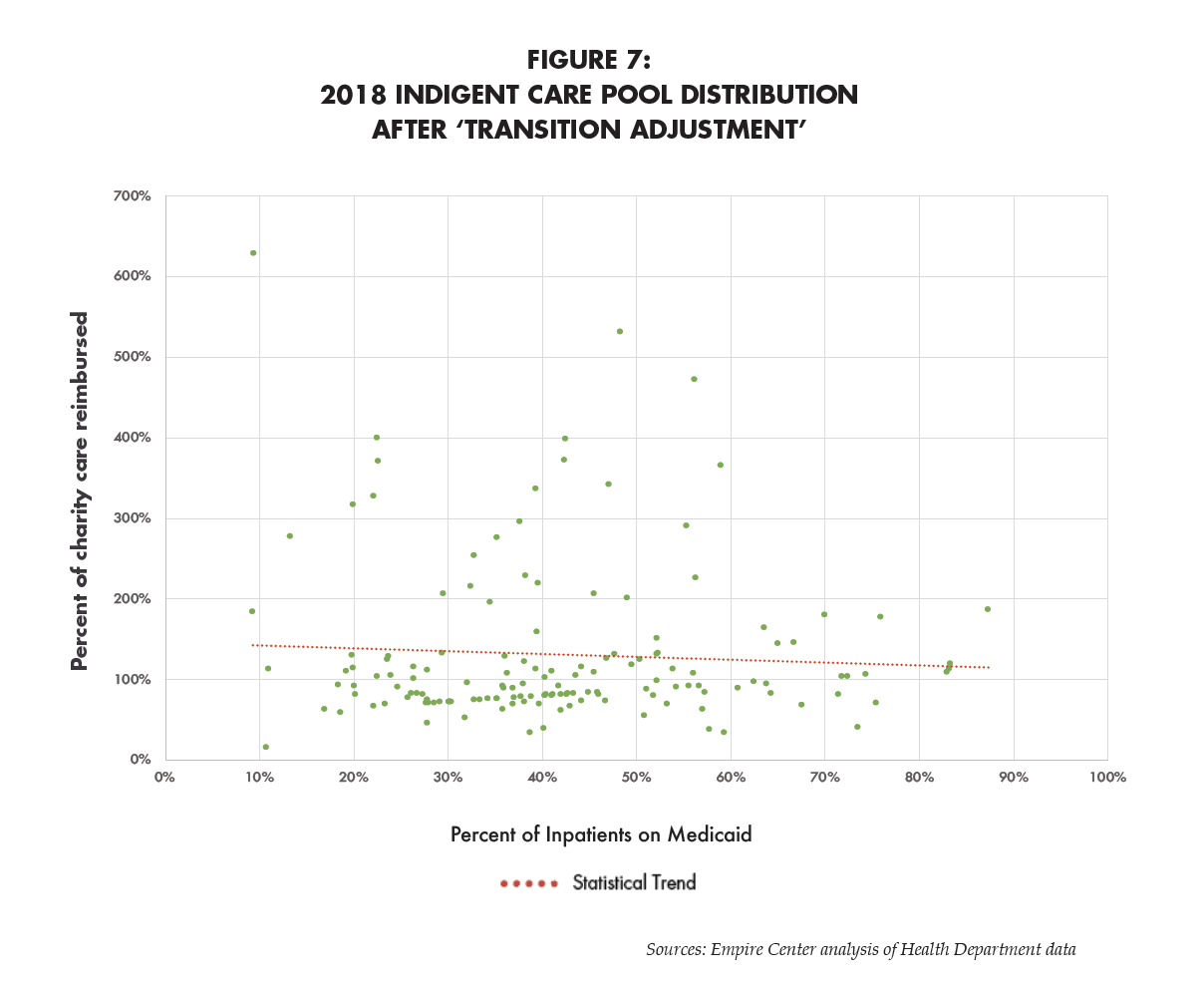

Figures 6 and 7 are scatter plots of Indigent Care Pool distributions to private, not-for-profit hospitals, with each dot representing a single institution. The X axis shows what percent of that hospital’s patients are on Medicaid (an indicator of community poverty), while the Y axis shows the amount that hospital’s Indigent Care Pool grant as a percent of its charity care expenses.

Figure 6 shows what the distribution pattern would be if the state strictly followed its funding formula without making the “transition adjustment”: The amount each hospital receives would correspond closely to the amount of charity care expenses it incurred, with gradually higher payments to hospitals serving a larger share of poor patients.

Figure 7 shows the distribution pattern as it actually is, with the transition adjustment applied. Most of the dots are scattered across the grid with no clear pattern, starkly illustrating the inequities of the formula – with hospitals at the top receiving far more generous funding than those at the bottom.

The red dotted line represents the statistical trend. Its downward slope points to a small negative correlation: Hospitals with smaller Medicaid populations tend to get proportionally bigger grants from the Indigent Care Pool, which is exactly the opposite of what one would expect.

It should be noted that demand for charity care from hospitals – the need that the Indigent Care Pool was meant to fulfill – has diminished since passage of the Affordable Care Act in 2010.

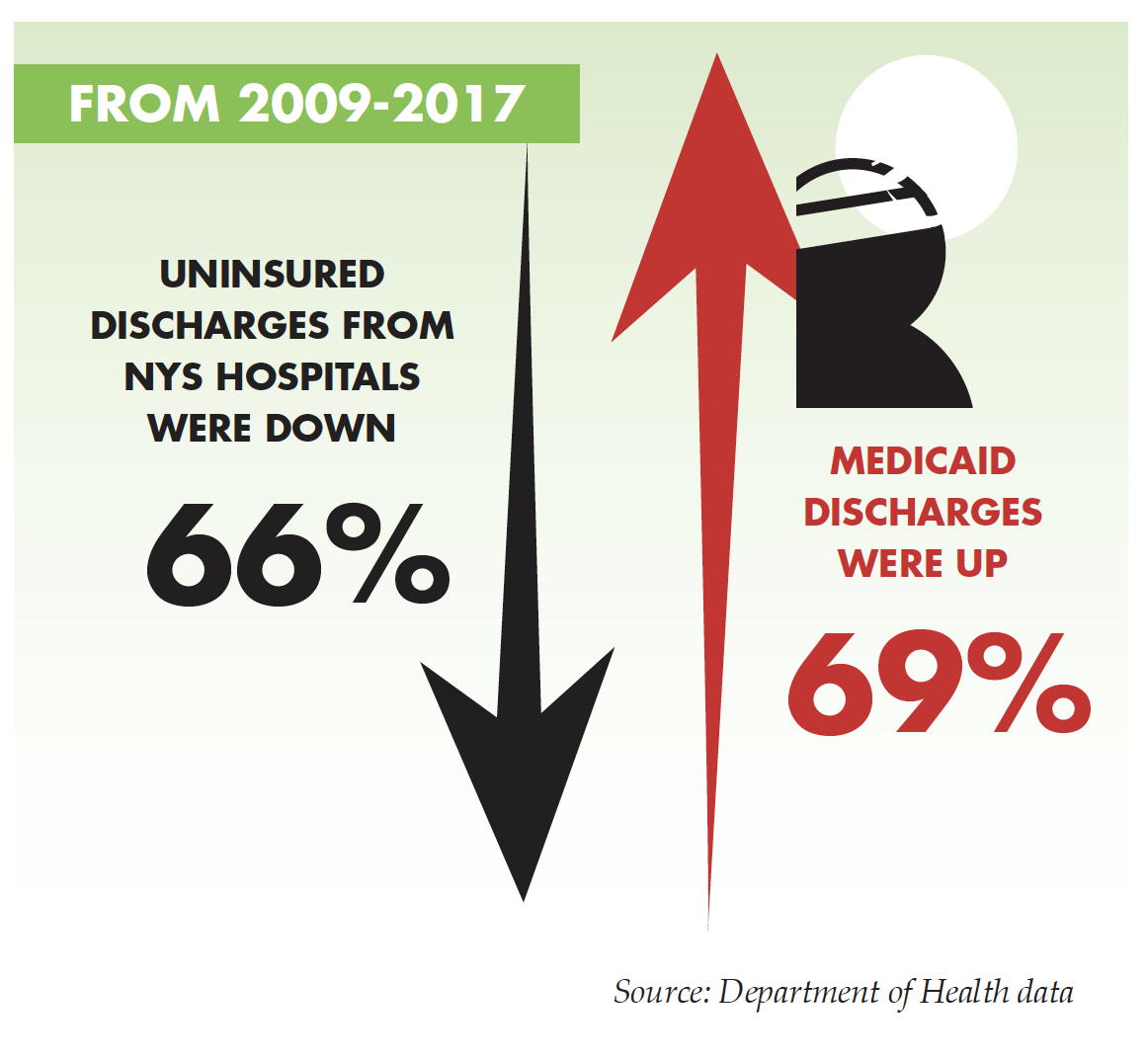

In 2017, hospitals reported discharging 46,971 patients whose insurance status was either “self-pay” or “unknown” – a decline of 66 percent since 2009, and a drop of 38 percent since ACA took full effect in 2014.[42]

Medicaid discharges increased from 416,607 in 2009 to 704,147 in 2017.

The number of uninsured hospital patients likely dropped further in 2018 and 2019, given that enrollment in Medicaid and ACA-subsidized private insurance has continued to climb. As of January 2020, the New York State of Health Exchange reported enrollment of 272,948 in ACA-subsidized private health plans, and 796,998 in the Essential Plan, a low-cost, state-operated health plan for people up to 400 percent of the federal poverty level.[43]

Despite the dramatically diminished need, spending by the Indigent Care Pool has stayed almost flat at just over $1 billion (except in 2010, when it spiked to $1.3 billion).

As with other HCRA programs, the Indigent Care Pool demands reform – both in where the money comes from, and how it is spent.

CONCLUSION: THE WAY FORWARD

If it didn’t already exist, it’s hard to imagine many state lawmakers supporting the Health Care Reform Act as it works today.

They’d be voting to hike taxes by $6 billion – which is huge, even by Albany standards.

They’ve be voting for taxes that hit the middle class and working poor harder than the wealthy.

They’d be voting to use those regressive revenues to cover one-fifth of the cost of Medicaid, a program otherwise financed with relatively progressive income taxes.

They’d be voting to make New Yorkers’ health insurance even more expensive, and more of a drag on the economy, than it already is.

They’d be voting to spend $1 billion a year on hospital subsidies that are more generous to hospitals in well-off communities than to safety-net institutions in poor neighborhoods.

They’d be voting to use healthcare dollars for a raft of other programs that confer special benefits on politically influential groups – such as physicians and unionized workers – without directly improving the health of a single New Yorker.

They’d be voting to tax cigarettes heavily enough to trigger a wave of smuggling, and then to dedicate none of the revenue to help smokers quit.

Such a plan would be unlikely to get much support from any party. Yet that is messy reality of HCRA in 2020.

The law did not arrive at this point overnight, nor would unraveling it be politically easy. It would mean upsetting the status quo, rescinding benefits for influential interest groups, and giving up billions in revenue – the last being especially tricky given the $2.5 billion shortfall in the Medicaid budget.

This year, however, there is no avoiding a vote on HCRA as it exists today. The pending expiration of surcharges in March 2020 forces Governor Cuomo and the Legislature to make a choice: They will either begin reforming the Health Care Reform Act, or perpetuate an indefensible status quo.

Here are four principles they should follow going forward:

First, stop treating HCRA revenues as a slush fund for special interests. Instead of subsidizing the state’s excessively costly medical malpractice system, lawmakers should try to fix it. Instead of earmarking money for healthcare workers’ compensation, lawmakers should focus only on buying the highest-quality care at the lowest available price.

Second, find a fairer, more effective way to finance medical care for the uninsured. Money should follow patients, not institutions. Ideally, hospitals and other providers would submit vouchers for uncompensated care that the state would partially reimburse. At the very least, what money is available should distributed based on who is delivering care, not who has the loudest voice in Albany.

Third, commit to weaning the state away from its dependence on HCRA revenues. The surcharges were defensible as a temporary measure to smooth the transition to deregulated hospital rates, but not as a major, permanent source of revenue for the state. Lawmakers should put enact a long-term plan to repeal the surcharges, reducing them by a fixed amount each year as programs are either eliminated or moved into the regular budget.

Fourth and mostly important: Do no further harm. That is, any hikes to the existing HCRA surcharges or the creation of new ones must be ruled out.

As Albany scrounges for revenue to close a Medicaid deficit, regressive taxes – especially ones that make health insurance even less affordable for employers and the middle class – are the wrong way to go.

APPENDIX

ENDNOTES

[1] Office of the State Comptroller, “The Health Care Reform Act (HCRA): The Need to Restore Accountability to State Taxpayers,” April 2003. (www.osc.state.ny.us/reports/health/hcra.pdf)

[2] John Rodat, “Hospital Reimbursement Revisited,” Empire State Report, March 1994.

[3] Ibid.

[4] Ibid.

[5] Chapter 639 of the Laws of 1996.

[6] Public Policy Institute of New York State, “Misguided Money: A Reexamination of the $2.6 Billion in Subsidies Provided by Taxpayers and Insurance Surcharges to Help Finance New York’s Medical Institutions,” November 30, 1998. (www.bcnys.org/ppi/misgdcnt.htm)

[7] Chapter 639.

[8] Ibid.

[9] Office of the State Comptroller, “The Health Care Reform Act (HCRA): State Fiscal Years 2002-03 and 2003-04,” October 2004. (www.osc.state.ny.us/reports/health/hcra102104.pdf)

[10] Op. cit., Public Policy Institute.

[11] Legislative history drawn from bill text; Division of the Budget financial plans; Office of the State Comptroller, “The Health Care Reform Act (HCRA): State Fiscal Years 2002-03 and 2003-04,” October 2004; and a slide deck prepared by the Health Department for the Health Care Reform Act Modernization Task Force, May 2015.

[12] Adam Nagourney, “Union Crosses Party Lines for Pataki,” The New York Times, March 20, 2002. (www.nytimes.com/2002/03/20/nyregion/union-crosses-party-lines-for-pataki.html)

[13] National Health Expenditure Data, Centers for Medicare & Medicaid Services. (https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData)

[14] Bureau of Labor Statistics, Current Employment Statistics. (https://www.bls.gov/data/)

[15] American Hospital Association, “Trendwatch Chartbook 2018,” Table 3.2. (https://www.aha.org/system/files/2018-05/2018-chartbook-table-3-2.pdf)

[16] Based on data from Hospital Compare at Medicare.gov. (medicare.gov/hospitalcompare)

[17] Empire Center analysis of data from the Centers for Medicare & Medicaid Services. (https://data.medicare.gov/Hospital-Compare/Unplanned-Hospital-Visits-Hospital/632h-zaca/data)

[18] “Fiscal Year Tax Collections: 2018-19,” New York State Department of Taxation and Finance. (https://www.tax.ny.gov/research/collections/fy_collections_stat_report/2018_2019_annual_statistical_report_of_ny_state_tax_collections.htm)

[19] Excellus BlueCross BlueShield, “The Facts About Taxes on New Yorkers Who Purchase Private Health Insurance,” Fall 2015. (www.excellusbcbs.com)

[20] United States Census Bureau, “Health Insurance Coverage in the United States: 2018,” September 13, 2016. (https://www.census.gov/library/publications/2019/demo/p60-267.html)

[21] New York State Department of Health. (https://www.health.ny.gov/regulations/hcra/gme/2020_surcharges_and_assessments.htm)

[22] Gordon Fairclough, “In New York, a Black Market for Illegal Cigarettes Thrives,” Wall Street Journal, December 27, 2002. (www.wsj.com/articles/SB1040938577857473793)

[23] International Consortium of Investigative Journalists, “Tobacco Underground.” (www.icij.org/project/tobacco-underground)

[24] Office of the State Comptroller and Division of the Budget.

[25] Public Policy Institute.

[26] Office of the State Comptroller cash basis reports. (http://www.osc.state.ny.us/finance/cbr.htm)

[27] Ibid.

[28] Campaign for Tobacco-Free Kids, “Broken Promises to Our Children: A State-by-State Look at the 1998 State Tobacco Settlement 21 Years Later,” December 19, 2019. (https://www.tobaccofreekids.org/what-we-do/us/statereport)

[29] Division of the Budget, “FY 2021 Executive Budget Financial Plan,” January 2020. (https://www.budget.ny.gov/pubs/archive/fy21/exec/fp/fy21fp-ex-amend.pdf)

[30] Susanne Craig and Benjamin Weiser, “Doctor in Sheldon Silver’s Corruption Trial Denies Improper Relationship,” The New York Times, November 5, 2015. (http://www.nytimes.com/2015/11/06/nyregion/witness-in-sheldon-silvers-corruption-trial-denies-improper-relationship.html?_r=0)

[31] Office of the State Comptroller cash basis reports.

[32] Division of the Budget.

[33] Census Bureau, “Health Insurance Coverage in the United States: 2018,” November 2019. (https://www.census.gov/content/dam/Census/library/publications/2019/demo/p60-267.pdf)

[34] Ibid.

[35] Details of the calculation of Indigent Care Pool distributions for 2018 are drawn from a Health Department spreadsheet obtained under the Freedom of Information Law.

[36] Elisabeth R. Benjamin, Arianne Slagle, and Carrie Tracy, “Incentivizing Patient Financial Assistance: How to Fix New York’s Hospital Indigent Care Program,” February 2012. (http://lghttp.58547.nexcesscdn.net/803F44A/images/nycss/images/uploads/pubs/IncentivizingPatientFinancialAssistanceFeb2012.pdf)

[37] Ibid.

[38] Final Recommendations of the Medicaid Redesign Team Health Disparities Working Group, October 20, 2011. (https://www.health.ny.gov/health_care/medicaid/redesign/docs/mrtcompanion.pdf)

[39] Op. cit., Health Department spreadsheet.

[40] City of New York, “One New York: Health Care for our Neighborhoods: Transforming Health + Hospitals,” April 26, 2016. (http://www1.nyc.gov/assets/home/downloads/pdf/reports/2016/Health-and-Hospitals-Report.pdf)

[41] Roosa S. Tikkanen, et al., “The New York Indigent Care Pool: Is there a relationship between hospital allocations and uninsured patient volumes among New York City hospitals?” Poster presented at the American Public Health Association Annual Meeting and Expo, October 29 to November 2 in Denver, Colo.

[42] Statewide Planning and Research Cooperative System (SPARCS), accessed at Health.Data.NY.gov.

[43] Press release from the New York State of Health, February 20, 2020. https://info.nystateofhealth.ny.gov/news/press-release-ny-state-health-announces-record-high-enrollment-more-49-million-new-yorkers

About the Author

You may also like

Opinion Poll – Energy

Executive Summary

New York voters prioritize affordable energy and show limited support for energy and climate policies that could increase costs. The survey finds broad opposition to home-heating electrification and climate-related lawsuits aga Read More

34 MTA Workers Made $200K+ In Overtime In 2025

Thirty-four employees of the Metropolitan Transportation Authority (MTA) received more than $200,000 in overtime payments in 2025, as total annual pay surpassed half a million dollars for some, according to , the Empire Center’s governm Read More

New York at the Crossroads. WILL IT MODERNIZE LIABILITY LAW OR EXPAND IT?

Executive Summary

New York’s Litigation Environment

In a wide range of areas, New York law subjects residents and businesses to greater liability than other states. Consider, for example, that:

Unlike most other states, New York a Read More

New York’s School Districts Plan To Spend Over $37K Per Student

Cover Image Credit: / at Wikipedia

School districts presenting budgets to voters on Tuesday, May 19, plan to spend an average of $37,033 per student, up 4.9 per Read More

Overtime on State Payroll Jumps 21%

104 employees made over $500k in 2025 total annual pay.

2,450 employees were paid more than Gov. Kathy Hochul's Read More

How Pension ‘Spiking’ Drives Up Costs for New York Taxpayers

Each year, hundreds of newly retired government workers across New York garner a benefit that would be unheard-of in the private sector: pensions that exceed the salaries they received while still on the job.

This is possible only because most current Read More

Energy Data Bulletin January 2026

January 2026

Summary and Insights

Electricity. In October 2025, average residential electricity price in New York was 26.95 cents per kilowatt-hour (kWh) and ranked 8th highest in the U.S., exceeding the national avera Read More

Seven Reasons Not To Raise Taxes in New York

Despite the robust growth of state revenues in recent years, many of New York's elected officials are pushing to further increase the tax burden on the state's residents and businesses.

Read More