Thanks to an absurdly wasteful federal law, New York’s Essential Plan is expected to continue running billion-dollar surpluses even as state officials more than double its spending over the next several years.

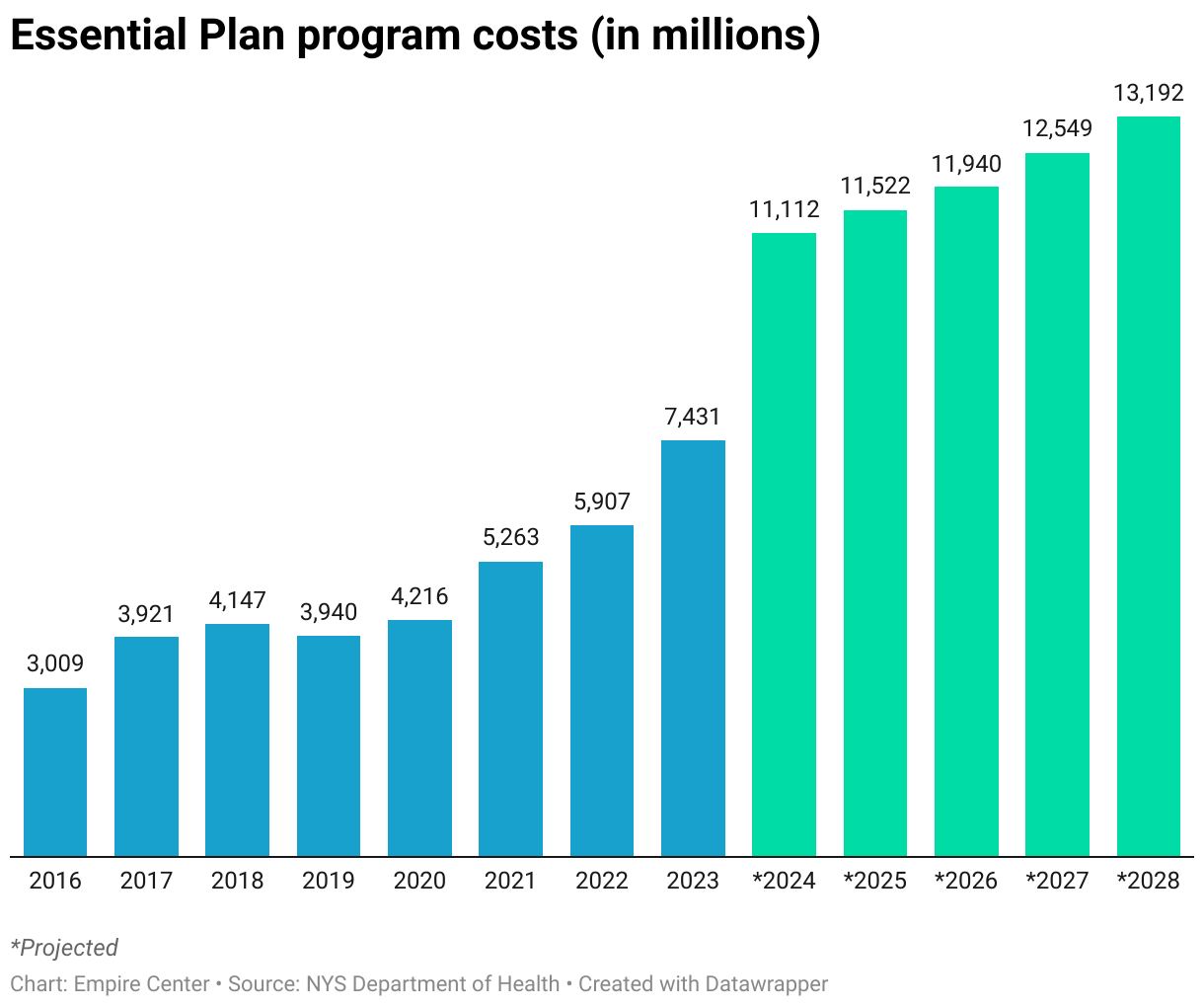

According to estimates in an expansion plan from the Health Department, the cost of the state-operated health plan for the near-poor – which was just under $6 billion in 2022 – will break $11 billion in 2024 and $12 billion by 2027, an increase of 112 percent in five years.

The expanded plan would not only cover more people, but also reduce their cost-sharing, increase payments to medical providers and health plans and add coverage for long-term care.

Yet the program won’t come close to using all the federal money it’s due to receive, meaning surpluses of $1 billion to $2 billion a year will continue piling up in a trust fund.

The peculiar finances of the Essential Plan derive from an optional provision of the Affordable Care Act that was exercised only by New York and Minnesota. Under this provision, states that establish a Medicaid-like “basic health program” for lower-income residents are entitled to collect 95 percent of the ACA premium tax credits that enrollees would otherwise receive.

In New York’s case, this funding formula has unexpectedly generated far more revenue than the state needed – likely because the tax credits are based on New York’s high commercial premiums, whereas the Essential Plan has paid relatively low, Medicaid-like fees for care.

As a result, the program’s trust fund has built up an accumulated surplus of more than $10 billion – money that’s stranded in legal limbo.

Launched in 2015, the Essential Plan currently offers low- or no-cost coverage to New Yorkers with incomes up to 200 percent of the federal poverty level, or $29,160 for an individual. As of January, more than 1.2 million people were enrolled.

The Hochul administration is seeking a federal waiver that would expand eligibility to 250 percent of the poverty level, or $36,450 for an individual, beginning in April 2024. This is expected to increase enrollment by about 100,000 – but mostly from people who already have alternate insurance. The net increase in coverage is estimated to be about 35,000.

The plan would also pay higher fees for hospitals, doctors and clinics, subsidize certain health plan expenses and add coverage for in-home long-term care. Annual spending per member would increase from about $5,600 last year to $7,800 in 2024, or 38 percent.

But the program's already over-generous revenue stream would balloon as well – thanks largely to the unusually high cost of health insurance in New York.

Under the ACA, New York is entitled to collect 95 percent of the value of tax credits that Essential Plan enrollees would have received if they bought commercial coverage through the state's insurance exchange, known as the New York State of Health. The amount of those tax credits, in turn, is based on the cost of the second-lowest silver-level plan on the exchange. In New York, those benchmark premiums have risen faster than in most other states, and currently sit at 54 percent above the U.S. average.

Under the ACA's dysfunctional formula, those higher premiums automatically generate more money for the Essential Plan – effectively rewarding New York for allowing health insurance costs to spiral.

The formula pays no attention to what the Essential Plan coverage actually costs, allowing the program to run massive annual surpluses – which the state's proposed expansion will reduce but not eliminate.

As of earlier this year, the program's trust fund reached $10 billion – a balance that is likely to sit unused for the foreseeable future. By federal law, the state cannot divert the money for any other purpose, nor can the federal government readily claw it back.

The program distorts New York's insurance market to some extent – by diverting a segment of generally younger, healthier customers from the commercial risk pool, likely contributing to higher premiums for those left behind.

Yet state officials have not been motivated to raise complaints about a program that provides health coverage for more than 1 million New York residents at Washington's expense.

From the national point of view, however, the program is massively wasteful. According to state estimates for 2025, federal taxpayers (including New Yorkers) will be spending about $9,300 per enrollee for coverage worth only $8,200 – with no one realizing any benefit from that extra $1,100.

The only available solution is for federal lawmakers to rewrite this broken provision of the ACA – which will be difficult to negotiate in a politically divided Congress.

This raises the question of how big the Essential Plan trust fund will have to grow before Washington takes action – $20 billion, $50 billion, $100 billion? As the law stands now, it's only a matter of time.

About the Author

You may also like

The Attorney General’s MFCU SNAFU

Attorney General Letitia James' latest fight with the Trump administration focuses on New York's Medicaid Fraud Control Unit, a federally funded agency housed in James' office.

On T Read More

Healthcare Revelations in the Enacted Budget Financial Plan

The state financial plan published on June 10 disclosed key information about healthcare revenue and spending that lawmakers had not made public when approving the annual budget two weeks before.

Read More

Federal Suit Traces Medicaid Fraud to the Top of NYS Government

The Trump administration's latest salvo against Medicaid fraud takes aim at a different kind of target – two high-ranking New York officials along with a major state contractor.

A Read More

Healthcare Highlights in the New State Budget

Governor Hochul's focus on affordability seems to have skipped over the healthcare portions of the new state budget.

The deal finalized May 27 Read More

Lawmakers Consider Hiking Fees for Filling Prescriptions

UPDATE: The proposal discussed below passed the Assembly Friday evening by an unofficial vote of 133-0. Having previously been approved by the Senate, the bill will head to Governor Hochul's desk for her signature or ve Read More

Budget Deal Reportedly Earmarks $100M for 1199 and Extends MCO Tax

As Governor Hochul and legislative leaders rush to finalize the overdue state budget, outlines of some healthcare-related deals have begun to emerge from the closed-door negotiations.

Read More

Four Problems with a Statewide Pied-à-Terre Tax

Soon after Governor Hochul floated the idea of a "pied-à-terre" tax in New York City, Albany Sen. Patricia Fahy proposed to expand the concept to the rest of the state.

As with H Read More

Albany Should Listen to Jamie Dimon

In his annual message to shareholders, JP Morgan Chase's chief executive, Jamie Dimon, offered a timely and pointed warning for New York policymakers.

It's worth , with emphasis add Read More