Insurance tax credits in the U.S. Senate GOP’s health plan would have a mixed effect on New Yorkers, reducing net premiums for some young, low-income consumers shopping in the non-group market, but raising costs for older ones.

Insurance tax credits in the U.S. Senate GOP’s health plan would have a mixed effect on New Yorkers, reducing net premiums for some young, low-income consumers shopping in the non-group market, but raising costs for older ones.

Overall, the credits are less generous than those in the Affordable Care Act. They cut off at 350 percent of poverty rather than 400 percent, and they’re intended to purchase plans with higher deductibles and copayments.

While the ACA’s tax credits are based on income, and the House GOP’s are based on age, the Senate’s tax credits combine the two approaches.

Like the ACA, the Senate plan caps the net premium cost for low-income consumers as a percentage of income, a ceiling that increases with higher pay. Above 150 percent of the federal poverty level, the Senate’s cap would also increase with age. Older consumers would be expected to pay as much as 16.2 percent of their income for coverage, compared to a maximum of 9.5 percent under current law. Credit-eligible consumers under 29 would pay no more than 6.5 percent of income.

The higher costs for older consumers would reflect their higher medical costs and, in most states, their higher premiums. New York, however, is one of two states, along with Vermont, that have banned individual and small-group insurers from charging higher premiums based on age. The Senate’s Better Care Reconciliation Act would effectively override that policy for New Yorkers using the credits.

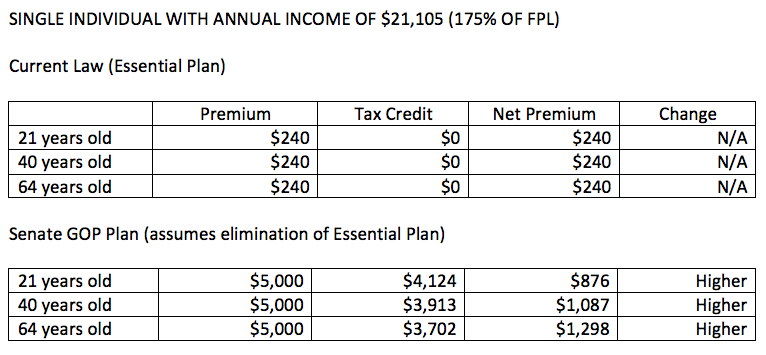

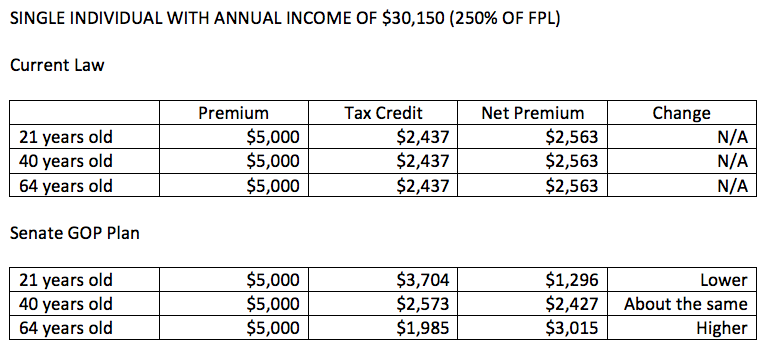

The charts below illustrate the impact of the proposed changes in the Senate and House health plans for various age and income groups. They do not attempt to project actual premiums. Instead, they start with a hypothetical premium of $5,000 per year for individual coverage, and show how different tax credits would affect net cost for different consumers. The charts do not factor in the possibility that changes to other parts of federal law, such as coverage regulations or taxation, would increase or decrease the hypothetical $5,000 premium.

The group of New Yorkers with the most to lose are enrollees in the Essential Plan, which is government-operated and costs no more than $20 a month for people up to 200 percent of the federal poverty level. Both the House and Senate plans would reduce available federal funding for the program, and the Cuomo administration has said it would be unlikely to continue. The alternative for most enrollees would using tax credits to buy commercial insurance. The Senate’s credits would offset most of the premium, especially for younger consumers, but net costs would still be substantially higher than the Essential Plan.

Among individuals with income of $30,150, or 250 percent of the poverty level, the impact would be mixed. Young consumers would pay less under the Senate plan than under current law, while older consumers would pay more and middle-aged consumers would be relatively unaffected.

Among individuals with income of $42,210, or 350 percent of the poverty level, young consumers would still see savings with the Senate plan, but middle-aged and older consumers would pay more. Above 350 percent of poverty, consumers would no longer be eligible for tax credits and would pay the full premium.

As mentioned above, the Senate plan would tie tax credits to less generous coverage – with minimum actuarial value of 58 percent instead of 70 percent under current law. That is expected to lower premiums – or at least slow their growth – but would also translate into substantially higher deductibles and copayments.

The Senate plan, like the House plan, would repeal Obamacare’s individual mandate, replacing it with a six-month waiting period to buy insurance for people who let their coverage lapse for more than 63 days in a year.

Analysts at the Congressional Budget Office project that the combined effect of changes in the Senate plan would both reduce the incentive for people to buy insurance and make it less affordable for many – resulting in a net drop in commercial coverage of 7 million over the next decade. The CBO projects that another 15 million would not have coverage due to cutbacks in Medicaid.

About the Author

You may also like

The Attorney General’s MFCU SNAFU

Attorney General Letitia James' latest fight with the Trump administration focuses on New York's Medicaid Fraud Control Unit, a federally funded agency housed in James' office.

On T Read More

Healthcare Revelations in the Enacted Budget Financial Plan

The state financial plan published on June 10 disclosed key information about healthcare revenue and spending that lawmakers had not made public when approving the annual budget two weeks before.

Read More

Federal Suit Traces Medicaid Fraud to the Top of NYS Government

The Trump administration's latest salvo against Medicaid fraud takes aim at a different kind of target – two high-ranking New York officials along with a major state contractor.

A Read More

Healthcare Highlights in the New State Budget

Governor Hochul's focus on affordability seems to have skipped over the healthcare portions of the new state budget.

The deal finalized May 27 Read More

Lawmakers Consider Hiking Fees for Filling Prescriptions

UPDATE: The proposal discussed below passed the Assembly Friday evening by an unofficial vote of 133-0. Having previously been approved by the Senate, the bill will head to Governor Hochul's desk for her signature or ve Read More

Budget Deal Reportedly Earmarks $100M for 1199 and Extends MCO Tax

As Governor Hochul and legislative leaders rush to finalize the overdue state budget, outlines of some healthcare-related deals have begun to emerge from the closed-door negotiations.

Read More

Albany Wavers on Shutting Down a Medicaid Racket

As Washington threatens to crack down on fraud and abuse in New York's Medicaid program, state legislators are doing their best to demonstrate why federal intervention is needed.

A Read More

Getting to the Bottom of the 340B Drug Discount Boondoggle

Some of New York's largest and most prosperous hospitals are reporting rapidly growing amounts of revenue from pharmacy sales – most of it apparently flowing from a controversial drug discount program known as 340B. Read More