Thanks to New York’s unusual insurance laws, the impact of the House GOP health plan on the state’s non-group insurance market would be dramatically different than virtually anywhere else.

Thanks to New York’s unusual insurance laws, the impact of the House GOP health plan on the state’s non-group insurance market would be dramatically different than virtually anywhere else.

The contrast is especially sharp when it comes to age: Nationwide, older consumers would have the most to lose from the GOP’s proposed changes to tax credits and insurance pricing rules.

In New York, almost the opposite is true: Young people shopping for non-group coverage face relatively higher costs than the elderly, some of whom would see a savings windfall.

These generational effects would set up a political quagmire for Albany if the House’s American Health Care Act (or something like it) becomes law.

What sets New York apart is that it is one of only two states, along with Vermont, that ban age-rating by insurance companies. Everywhere else, older customers have to pay more for non-group policies, to reflect the higher medical costs that come with age.

President Obama’s Affordable Care Act limited the practice, allowing insurers to charge older customers no more than three times as much as the young. In effect, the young are cross-subsidizing the elderly – a phenomenon amplified by New York’s policy.

In the name of loosening regulations, AHCA would lift the maximum age-rating ratio from 3-1 to 5-1, and even higher in states that obtain waivers. At the same time, Obamacare tax credits that are based on income would be replaced with tax credits based on age, ranging from $2,000 a year for people in their 20s to $4,000 for people in their 60s.

The combined effect of those two changes varies widely based on age and income – generally favoring younger and wealthier consumers while disadvantaging older and poorer ones.

As projected in Table 5 of the Congressional Budget Office’s latest AHCA analysis, a 64-year-old non-group customer with income just above the poverty level would face an almost 850 percent premium increase compared to current law, while a 21-year-old would see almost no change.

But if the state’s ban on age-rating remains in effect, AHCA’s effects in New York will look nothing like the CBO’s projections. In some respects, they will be a mirror image.

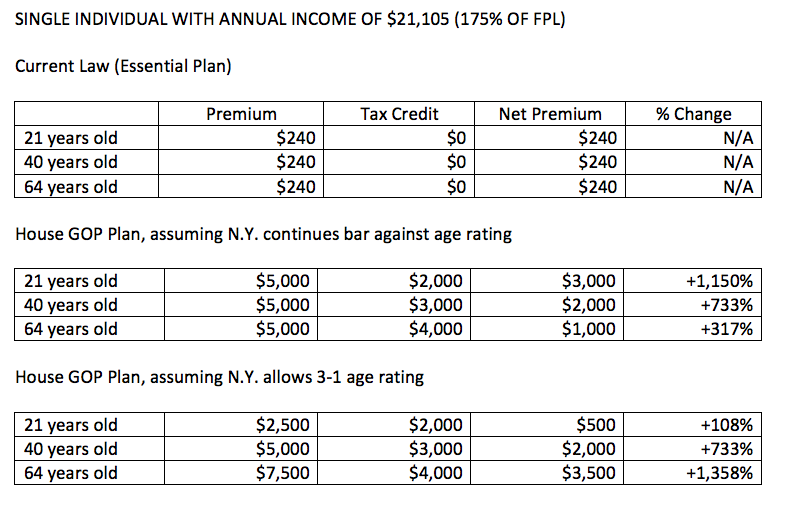

The tables below attempt to roughly sketch how AHCA would affect New York’s non-group market for a variety of age and income groups. They also look at what would happen if New York switched to a 3-1 age-rating limit.

The right-hand columns show the percentage change in net premium compared to current law. For example, if a 40-year single woman with income at 250 percent of the poverty level bought a hypothetical $5,000 policy under current law, she would receive an income-based tax credit of about $2,500, for a net premium of $2,500. Under AHCA, her age-based tax credit would be $3,000, for a net premium of $2,000, which is 20 percent less than current law.

A few caveats:

- The premium numbers in the left column are based on the rounded-down cost of the second-cheapest silver-level Obamacare plan in New York City for 2017. Real premiums vary widely based on region and plan selection.

- All figures are intended to illustrate the general impact of policy changes, not serve as actual projections.

- There has been no attempt to trend the numbers forward to 2020, when AHCA would take effect, or 2026, as in the CBO report. Nor are the numbers adjusted for the effect on the risk pool of people dropping or adding coverage in response to changing net premiums.

- This analysis does not factor in the possibility that New York would seek a waiver under AHCA related to Essential Health Benefits or pre-existing conditions.

As the tables show, New York consumers below 200 percent of the poverty level would be hardest hit – facing huge premium increases across the board. This is mainly because they currently qualify for New York’s Essential Plan, a government-funded program that costs either nothing or $20 a month, depending on income. This is an optional benefit under Obamacare that only New York and Minnesota used, and the Cuomo administration has warned that AHCA would effectively eliminate the program.

Since AHCA also eliminates the tax penalty for failing to have insurance, many lower-income New Yorkers would undoubtedly drop their coverage.

For consumers at 250 percent of poverty ($30,150 for an individual), the picture changes completely. Hypothetical 40- or 64-year-olds would save money, because their age-based tax credits under AHCA would be bigger than their income-based credits under Obamacare. A 21-year-old, on the other hand, would pay substantially more than under current law.

At 450 percent of poverty ($54,270 for an individual), consumers of all ages would stand to save money. This is because Obamacare’s tax credits cut off at 400 percent of poverty, but AHCA’s would be fully available up to incomes of $75,000 for individuals or $150,000 for families. The savings would be welcome for the demographic group that until now has paid full price for individual coverage, but they are a relatively small slice of the non-group market.

If New York’s age-rating ban stays in effect, the young would see significantly higher cost increases, or smaller savings, compared to the elderly in all income categories. If the state switched to 3-1 age-rating, the opposite would be true.

Thus AHCA would pose a knotty dilemma for state lawmakers: They could either keep an age-rating policy that would disadvantage the young – potentially causing them to drop coverage and leaving behind an older and sicker risk pool. Or they could vote to change the law in a way that would be painfully expensive for the elderly.

One potential solution would be for New York’s representatives in Washington to seek an amendment that allows for a flat tax-credit structure in states that want one. It’s also possible that AHCA will be completely changed or rejected by the U.S. Senate, which would save Albany the trouble of making a tough choice.

About the Author

You may also like

The Attorney General’s MFCU SNAFU

Attorney General Letitia James' latest fight with the Trump administration focuses on New York's Medicaid Fraud Control Unit, a federally funded agency housed in James' office.

On T Read More

Healthcare Revelations in the Enacted Budget Financial Plan

The state financial plan published on June 10 disclosed key information about healthcare revenue and spending that lawmakers had not made public when approving the annual budget two weeks before.

Read More

Federal Suit Traces Medicaid Fraud to the Top of NYS Government

The Trump administration's latest salvo against Medicaid fraud takes aim at a different kind of target – two high-ranking New York officials along with a major state contractor.

A Read More

Healthcare Highlights in the New State Budget

Governor Hochul's focus on affordability seems to have skipped over the healthcare portions of the new state budget.

The deal finalized May 27 Read More

Lawmakers Consider Hiking Fees for Filling Prescriptions

UPDATE: The proposal discussed below passed the Assembly Friday evening by an unofficial vote of 133-0. Having previously been approved by the Senate, the bill will head to Governor Hochul's desk for her signature or ve Read More

Budget Deal Reportedly Earmarks $100M for 1199 and Extends MCO Tax

As Governor Hochul and legislative leaders rush to finalize the overdue state budget, outlines of some healthcare-related deals have begun to emerge from the closed-door negotiations.

Read More

Albany Wavers on Shutting Down a Medicaid Racket

As Washington threatens to crack down on fraud and abuse in New York's Medicaid program, state legislators are doing their best to demonstrate why federal intervention is needed.

A Read More

Getting to the Bottom of the 340B Drug Discount Boondoggle

Some of New York's largest and most prosperous hospitals are reporting rapidly growing amounts of revenue from pharmacy sales – most of it apparently flowing from a controversial drug discount program known as 340B. Read More