In the face of New York’s rapidly rising Medicaid spending, both the Cuomo administration and some of its critics have pointed to demographics as a driving factor.

The state’s population is aging, they have said, so long-term care costs should be expected to increase.

There are two main reasons to doubt this narrative.

First, Medicaid’s long-term care enrollment is surging too quickly to be explained by demographics alone.

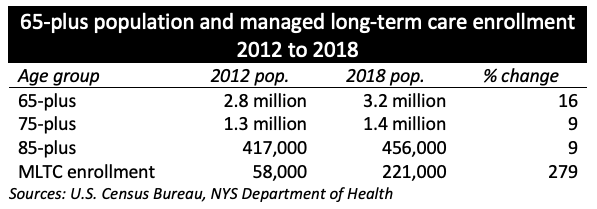

As seen in the chart below, New York’s 65-plus population grew by 16 percent between 2012 and 2018. The older cohorts – who are more likely to need long-term care – grew by 9 percent.

By contrast, enrollment in Medicaid managed long-term care plans soared by 279 percent. That’s 17 times the growth rate of the 65-plus population, and 30 times larger than the rate for the 75-plus population. (See clarification below.)

Second, New York’s Medicaid spending on certain long-term care services is dramatically out of line with that of other states – and has been since before the recent enrollment surge.

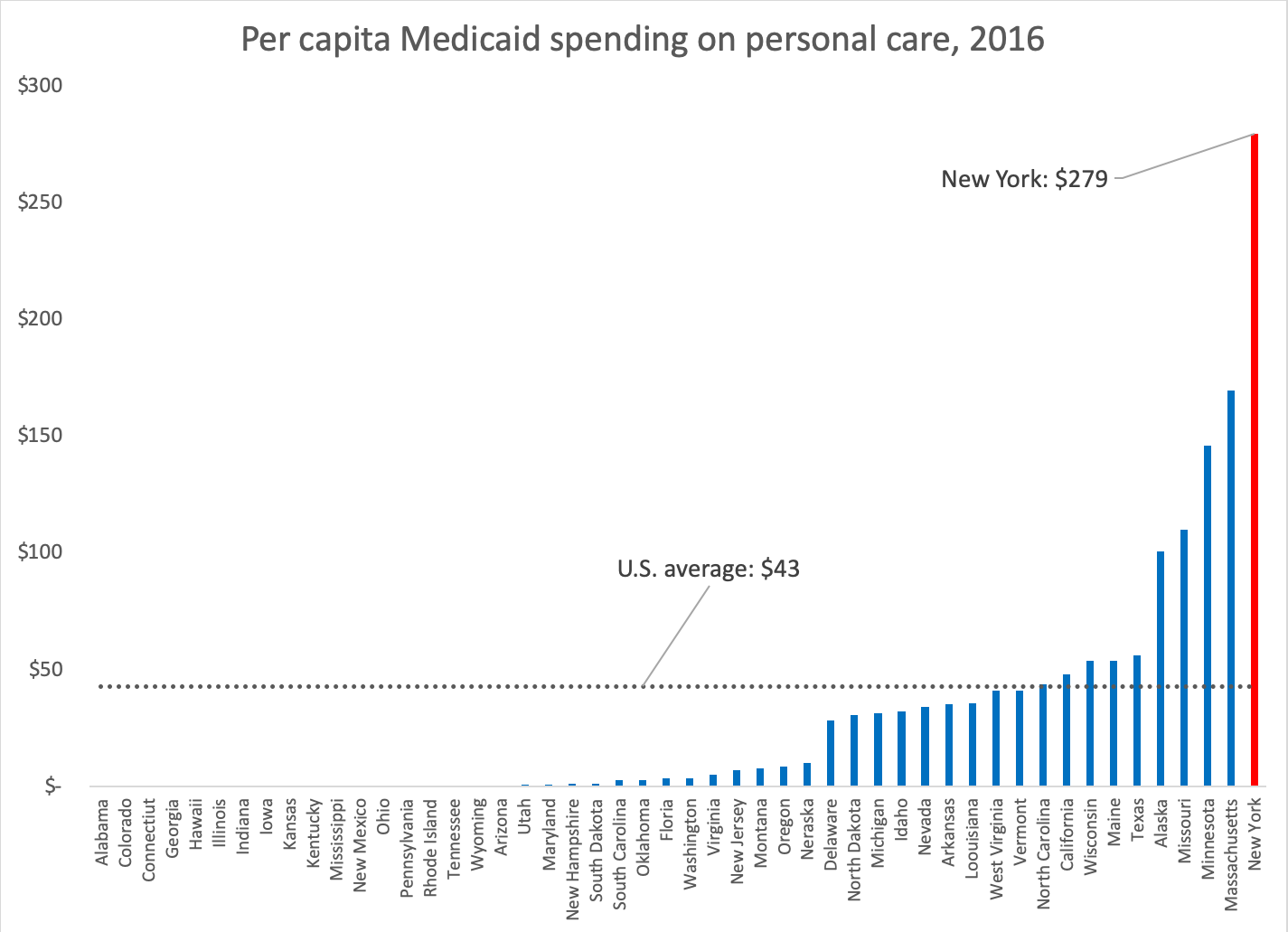

A prime example is the benefit known as personal assistance or personal care – which refers to non-medical services, such as bathing, dressing and housekeeping, provided for Medicaid recipients who are too disabled to handle these tasks.

Although this optional benefit is available in 32 other states, the scale of New York’s personal care program is an outlier. As of 2016, its per capita spending was 6.5 times higher than the national average and 65 percent higher than the No. 2 state, which was Massachusetts.

When Cuomo took office in 2011, New York accounted for 23 percent of nationwide spending on personal care. By 2016, that figure was up to 40 percent – and has undoubtedly continued to rise in the four years since.

So it’s true that New York is older than the national average, and that its elderly cohort is growing faster than the population as a whole (which is stagnant or declining). But demographics alone do not explain why long-term care spending has risen so fast.

CLARIFICATION: It should be pointed out that the initial increase in managed long-term care enrollment, from 2012 to 2015, reflected a change in policy. The state had required many long-term care recipients to switch from “fee for service” coverage, in which the state directly compensates providers, to managed care, in which payment is funneled through private insurance plans. Thus many if not most enrollees in those first three years were not new to Medicaid.

After that transition was complete in 2015, however, enrollment in continued trending upward at double-digit rates. From 2015 to 2018, enrollment increased 62 percent, compared to 7 percent for the over-65 population.

About the Author

You may also like

The Attorney General’s MFCU SNAFU

Attorney General Letitia James' latest fight with the Trump administration focuses on New York's Medicaid Fraud Control Unit, a federally funded agency housed in James' office.

On T Read More

Healthcare Revelations in the Enacted Budget Financial Plan

The state financial plan published on June 10 disclosed key information about healthcare revenue and spending that lawmakers had not made public when approving the annual budget two weeks before.

Read More

Federal Suit Traces Medicaid Fraud to the Top of NYS Government

The Trump administration's latest salvo against Medicaid fraud takes aim at a different kind of target – two high-ranking New York officials along with a major state contractor.

A Read More

Healthcare Highlights in the New State Budget

Governor Hochul's focus on affordability seems to have skipped over the healthcare portions of the new state budget.

The deal finalized May 27 Read More

Lawmakers Consider Hiking Fees for Filling Prescriptions

UPDATE: The proposal discussed below passed the Assembly Friday evening by an unofficial vote of 133-0. Having previously been approved by the Senate, the bill will head to Governor Hochul's desk for her signature or ve Read More

Budget Deal Reportedly Earmarks $100M for 1199 and Extends MCO Tax

As Governor Hochul and legislative leaders rush to finalize the overdue state budget, outlines of some healthcare-related deals have begun to emerge from the closed-door negotiations.

Read More

Four Problems with a Statewide Pied-à-Terre Tax

Soon after Governor Hochul floated the idea of a "pied-à-terre" tax in New York City, Albany Sen. Patricia Fahy proposed to expand the concept to the rest of the state.

As with H Read More

Albany Wavers on Shutting Down a Medicaid Racket

As Washington threatens to crack down on fraud and abuse in New York's Medicaid program, state legislators are doing their best to demonstrate why federal intervention is needed.

A Read More