Yesterday marked the end of a second straight sub-par fiscal year for most of the nation’s state and local public pension funds, including all five New York City funds and the New York State Teachers’ Retirement System (NYSTRS).

Yesterday marked the end of a second straight sub-par fiscal year for most of the nation’s state and local public pension funds, including all five New York City funds and the New York State Teachers’ Retirement System (NYSTRS).

The bellwether S&P 500 and the Dow Jones Industrial Average were essentially flat, and major foreign indexes were all down (some sharply) during the same period, after a volatile year marked by weak global economic growth, slumping U.S. corporate profits and uncertainty about the outlook for the China and the European union.

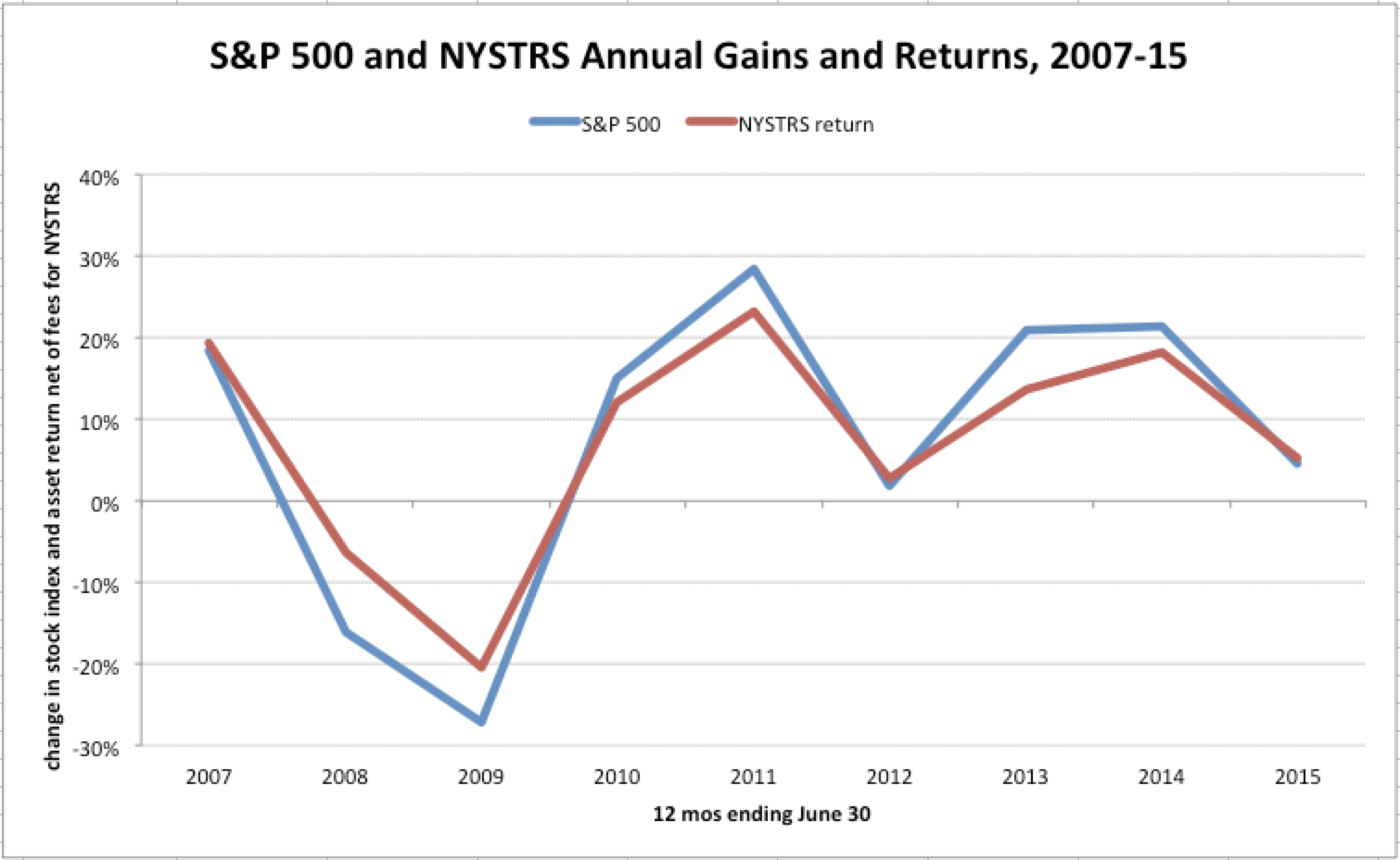

Because public pension funds typically invest roughly 70 percent of their assets in equities, and more than half in corporate stocks, their annual returns are strongly correlated with the stock markets—as shown, for example, in the following chart tracking the S&P 500 and NYSTRS returns since 2007.

The S&P 500 average change for the period shown above was 5.9 percent, while the NYSTRS average was 6.6 percent — considerably below its assumed return of 8 percent. NYSTRS has since lowered its assumed return to 7.5 percent, while the city pension funds are in the process of “amortizing” their annual expectations down to 7 percent. Their actual FY 2015 experience was well below those levels: 5.2 percent net of fees for NYSTRS, and 3.4 percent collectively for the city funds.

Based on the stock indexes, it seems likely NYSTRS and the city funds, as well as other public pension systems with July 1-June 30 fiscal years, will have much smaller gains (if any) for fiscal 2016, once again undershooting their targets.

So what does this mean for taxpayer costs? A lot depends on how the financial markets fare in the next two years. NYSTRS, for example, values assets based on a “five-year phased in deferred recognition of each year’s actual gain or loss, above (or below) an assumed inflationary gain of 3.0%.” As a result, there’s upward pressure on contributions when the formula includes big losing years such as 2009—when, for example, NYSTRS’ asset values dropped 21 percent. The city funds use a slightly different method of “smoothing” asset values over a three- to five-year period, but the underlying forces are similar.

Looking ahead, however, the smoothing formula used to figure employer contributions in 2017 will no longer be boosted by the big gains all funds realized in fiscal 2011. The net change in assets over the five years ending 2016 has roughly kept even with investment targets. So, if returns fail to meet or exceed the target over the next couple of years, taxpayer contributions will have to rise again to make up the difference. A repeat of the 2007-09 bear market—or even something just half as bad—would cause pension costs to rise again.

Much the same can be said of the Common Retirement Fund, which feeds the New York State and Local Retirement System (NYSLRS), which ended its 2016 fiscal year on March 31 with essentially no gain at all. The fund, run by state Comptroller Thomas DiNapoli, is also heavily weighted to stocks—and, like all public pension funds, is allowed to calculate its funding needs based on accounting assumptions that would not pass muster in the private sector.

You may also like

The Attorney General’s MFCU SNAFU

Attorney General Letitia James' latest fight with the Trump administration focuses on New York's Medicaid Fraud Control Unit, a federally funded agency housed in James' office.

On T Read More

Healthcare Revelations in the Enacted Budget Financial Plan

The state financial plan published on June 10 disclosed key information about healthcare revenue and spending that lawmakers had not made public when approving the annual budget two weeks before.

Read More

Federal Suit Traces Medicaid Fraud to the Top of NYS Government

The Trump administration's latest salvo against Medicaid fraud takes aim at a different kind of target – two high-ranking New York officials along with a major state contractor.

A Read More

It Is Time to Rethink the Regional Greenhouse Gas Initiative

Before budget negotiations, Gov. Hochul warned that unless New York changes its climate plans, New Yorkers could face a $2.26-per-gallon increase in gasoline prices. The reason is the so-called “cap-and-invest” scheme, under which energy companies wou Read More

Healthcare Highlights in the New State Budget

Governor Hochul's focus on affordability seems to have skipped over the healthcare portions of the new state budget.

The deal finalized May 27 Read More

Lawmakers Consider Hiking Fees for Filling Prescriptions

UPDATE: The proposal discussed below passed the Assembly Friday evening by an unofficial vote of 133-0. Having previously been approved by the Senate, the bill will head to Governor Hochul's desk for her signature or ve Read More

Lack of Common Sense on Energy in the Budget

Lack of Common Sense on Energy in the Budget

Anyone hoping the governor would make even modest, common-sense changes to New York’s disastrous energy policies will be disappointed. The energy portion of the budget is out, and the nons Read More

Budget Deal Reportedly Earmarks $100M for 1199 and Extends MCO Tax

As Governor Hochul and legislative leaders rush to finalize the overdue state budget, outlines of some healthcare-related deals have begun to emerge from the closed-door negotiations.

Read More