The stock market turmoil of the last week is a reminder of why it’s risky, verging on foolhardy, for New York’s state government to depend as heavily as it does on high-income households and Wall Street investors.

The stock market turmoil of the last week is a reminder of why it’s risky, verging on foolhardy, for New York’s state government to depend as heavily as it does on high-income households and Wall Street investors.

In the current fiscal year, taxes paid by the highest-earning 1 percent of New York taxpayers—including commuters to jobs in the state—are expected to generate 43 percent of personal income tax receipts, which in turn translates into 27 percent of total state taxes.

New York State taxes all income at the same rates, but capital gains typically yield revenues for Albany at a higher average rate than wage income. That’s because capital gains—and, important to keep in mind at the moment, capital losses as well—flow disproportionately to New Yorkers in the supposedly temporary “millionaire tax” bracket of 8.82 percent. Governor Andrew Cuomo’s reliance on repeated extensions of the higher rate, bundled with also (supposedly) temporary cuts in middle class tax rates, has the net result of making New York’s largest revenue source even more subject to swings in income among the top 1 percent, whose incomes typically start around $1 million.

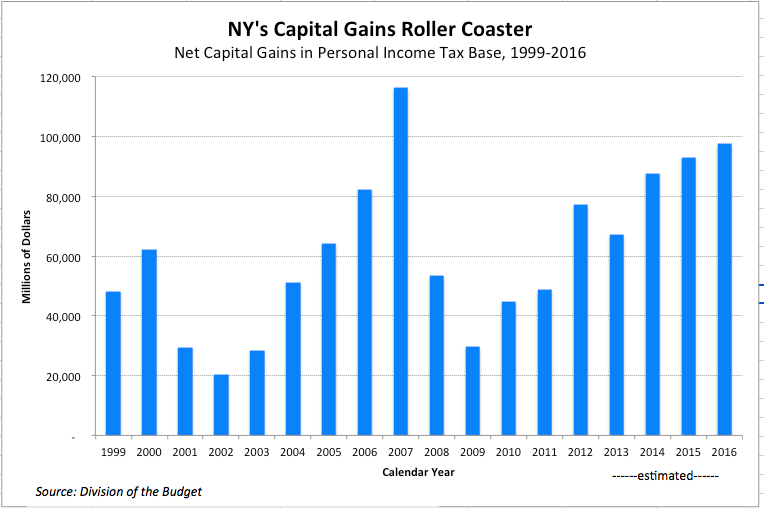

Net capital gains (profits minus losses) are also highly volatile. They were about 11 percent of adjusted gross income subject to New York State taxes last year, up from a low of 5 percent in 2009, but capital gains have accounted for fully 28 percent of the total increase in the state’s income tax base since 2010, according to the state Budget Division. That’s a pretty striking figure when you keep in mind that a large chunk of the state’s highest-income taxpayers are out-of-state commuters whose capital gains, unlike wages earned here, are not taxed by Albany.

In the wake of the last big Wall Street crash, between 2007 and 2009, net capital gains income of New Yorkers plunged by more than half, from $116 billion to $53 billion, accounting for all of the decrease in the state income tax base that year. The following year, capital gains dropped by nearly half again, to just below $29 billion, the lowest level since 2003. Much of the change in capital gains since the recession has reflected what DOB calls “income shifting” influenced by taxpayer expectations of federal tax rate increases in 2010 and again in 2012. All of the recent ups and downs are illustrated in the chart below.

Cuomo’s fiscal 2016 budget estimated that net capital gains of New York residents would hit $93 billion this year, an increase of 6.1 percent over 2014, and will rise by 5 percent in 2016. But even after yesterday’s Wall Street rally, as of the start of trading this morning, the Dow was down 5 percent from levels at the start of the year, and the S&P 500 was down almost 7 percent in the same period. For New Yorkers to hit Cuomo’s budget estimate for gains in their stock portfolios alone, the Wall Street indices will need to jump by at least low double digits over the rest of this year.

Of course, stock market gyrations also affect public pension funds, but even if the market falls further, it will be a couple more years before there is any impact on tax-funded pension bills. That’s because the pension funds calculate required contributions only after “smoothing” asset returns over a five-year rolling average, so that a sharp spike up or down in any one year doesn’t immediately affect the bill. In the wake of big market “corrections,” the high bill hits just as taxpayers and local governments are struggling to recover from a downturn.

The pension funds are still digging their way out of the holes created by the 2007-09 meltdown; while the contribution rates (as percentages of employee salaries) billed to the state and localities have begun to drop, they remain well above actuarial “normal” levels. A true bear market scenario in the next few months, on the heels of subpar returns in fiscal 2015, would wipe out much of the pension funds’ double-digit gains in 2012 and 2014, and rates could shoot back to recent peaks.

You may also like

Albany Should Listen to Jamie Dimon

In his annual message to shareholders, JP Morgan Chase's chief executive, Jamie Dimon, offered a timely and pointed warning for New York policymakers.

It's worth , with emphasis add Read More

Mamdani Gets an Important Tax Fact Wrong

At a hearing in Albany last week, New York City Mayor Zohran Mamdani lobbied state lawmakers to help him balance the city's finances with a two-percentage-point hike in the city's income tax on people making over $1 million Read More

Highlights of Albany’s Bloated and Belated Budget

The state Legislature approved the last of nine budget bills Thursday evening, 38 days after the start of the fiscal year. Here are some highlights of the fiscal impact of final spending plan:

Top lines

Read More

Courts set a limit on NY’s tax reach

Just in time for tax season, New York State's tax agency just lost a major legal challenge to its policy of pursuing maximum income tax payments from wealthy vacation homeowners—even when they live elsewhere. Read More

Despite working at home, commuters kept paying a big share of NY taxes

Average daily office occupancy in New York City has bounced back from 2020-21 lows, but by most accounts remains well below pre-pandemic norms. Read More

The Inflation Tax Paid by New York State Filers

With inflation rampaging, the seven-percent increase in key federal tax code thresholds is the biggest one-year hike since key aspects of the IRS code were indexed to inflation. Read More

NY’s pre-Covid tax base drain confirmed in new comptroller’s report

New York was a net loser of income tax filers to other states even in the five years leading up to the pandemic disruption of 2020 Read More

Upstate Economy at Risk Under NYC Renewable Energy Plan

While the power from these new projects will go directly into the City, all New York utility users will help pay for them through their utilities’ purchases of renewable energy credits. Read More