SUNY’s Personal Retirement Plan As a Model for Pension Reform

What you’ll learn from this report:

- Defined-contribution plans are personal retirement accounts supported by employer and employee contributions. In contrast to traditional pensions, they can follow employees if they change jobs, and the pension account is usually not wiped out if an employee dies before retirement.

- The State University of New York (SUNY) and City University of New York (CUNY) have offered a defined-contribution retirement option since the 1960s, and large majorities of professional employees in both systems have chosen it over the standard pension mandated for other public employees.

- The SUNY and CUNY model, built on annuities designed to provide a stream of lifetime income, differs in key respects from a typical private sector 401(k) defined-contribution plan.

- Defined-contribution plans are portable, allowing workers to take their benefits from one employer to another.

- Governor Cuomo’s proposed Tier 6 pension reform would allow new state and local government employees, including teachers, to choose defined-contribution retirement plans or a traditional defined-benefit public pension.

- The baseline funding level of 4 percent of annual salary for the proposed defined-contribution plans is too low.

- A new defined-contribution plan for state and local employees should require total contributions of at least 12 percent of salary, with employee shares matching the levels proposed under the governor’s proposed Tier 6 defined-benefit plan.

- State officials need to give more careful consideration to defined-contribution plan design features to ensure that employees are provided with fairly priced investment and annuity choices tailored to their long-term goals.

- The creation of a universal defined-contribution option for new state and local government employees in New York is a golden opportunity to create a national model for pension reform.

OVERVIEW

Traditional public employee pension programs in New York State have become unaffordable for taxpayers—while denying workers the ability to choose more flexible approaches to retirement planning.

But two of New York’s largest government employers are a notable exception to the rule. The State University of New York (SUNY) and City University of New York (CUNY) have long given their employees the right to opt into personal defined-contribution retirement plans. Large majorities of professors and professional staff in the two university systems have voluntarily embraced such plans since they were first offered almost 50 years ago.

As part of his proposed Tier 6 pension reform, Governor Andrew M. Cuomo would offer all new state and local workers the same kind of defined-contribution option.

Traditional pensions supply risk-free benefits under rigid formulas favoring long-term employees at the expense of those who prefer not to spend all or most of their careers with the same employer. The seemingly lower “normal” costs of public pension plans are misleading, made possible by government accounting standards that allow public pension systems to obscure their long-term liabilities.

By contrast, defined-contribution plans are financially transparent and predictable for employers, creating no liability for future taxpayers. While workers assume the market risk associated with funding their own retirements, they also gain the benefits of rapid vesting, portability to different employers and greater flexibility to shape financial plans in line with personal needs and preferences.

Critics have attacked Cuomo’s proposal by generalizing about the shortcomings of defined-contribution plans in the private sector, especially 401(k) accounts. However, as this report explains, the SUNY and CUNY plans differ in crucial respects from a typical 401(k). They mimic a traditional pension by providing a stream of post-retirement income through private insurance annuity contracts. Annuities protect against the risk that retirees will outlive their savings—a key shortcoming of tax-deferred savings plans designed primarily to accumulate wealth. The Obama Administration has been seeking to encourage use of annuities as a way to help middle-class Americans save for retirement.

Data presented in this report include the average account accumulations of SUNY and CUNY participants in defined-contribution plans offered by Teachers Insurance and Annuity Association and College Retirement Equities Fund (TIAA-CREF). Even assuming low salary growth and investment returns in the future, university employees approaching retirement age have saved enough through their TIAA-CREF annuity plans, in combination with Social Security benefits, to replace nearly 70 percent of their final salaries in retirement.

In his 2012-13 budget presentation, Governor Cuomo said he was advocating “a voluntary option for a defined-contribution plan that follows the TIAA-CREF type model.” [i]However, his bill language does not go far enough to achieve that objective. Recommendations for improving the governor’s proposal include the following:

- Raise the total funding level. The governor’s plan would require a minimum employer contribution of 4 percent, rising to 7 percent for employees who elect to contribute 3 percent of their own, bringing the total maximum savings to 10 percent. The minimum level will be tempting for many young and low-wage workers, but it would not provide the foundation for a secure retirement. Even a 10 percent savings rate would fall below the levels recommended by many retirement planning experts. The governor’s plan should be amended to raise the total contribution to a fixed 12 percent of salary, with mandatory employee shares of 4 to 6 percent depending on salary, as recommended on the defined-benefit side of Tier 6. The employer share would inversely range from 6 to 8 percent as necessary to bring the total to 12 percent. A contribution of 8 percent would still fall below the theoretical long-term expected cost of the current Tier 5 defined-benefit pension

- Create incentives to save more. The main retirement account created by the governor’s legislation should be coupled with a separate tax-deferred savings vehicle that takes advantage of the “auto-save” provisions of the 2006 federal Pension Protection Act, especially those allowing automatic escalation of contributions when pay increases.

- Pay closer attention to plan design details. The SUNY-CUNY plan is required by law to funnel deposits into annuity contracts. A strong preference for annuities— while still preserving individual flexibility to make lump sum conversions on retirement—should also be reflected in the legislative and regulatory framework for an expanded statewide defined-contribution plan. The state should also seek to bargain with financial institutions for low group fees on annuities and other products. During the savings accumulation phase, plan sponsors need to ensure that defined-contribution participants—especially young workers—do not automatically “default” to low-return vehicles such as money-market accounts, as is now the case in the SUNY plan.

________________________________________________________________________________________

ENDNOTES OVERVIEW

[i]2012 Executive Budget Presentation, Jan. 17, 2012. Webcast at http://www.governor.ny.gov/20122013ExecutiveBudget

________________________________________________________________________________________

1. THE UNSUSTAINABLE MODEL

The vast majority of New York’s 1.3 million state and local government employees are automatically enrolled in defined-benefit (DB) pension plans, which guarantee a stream of post-retirement income based on peak average salaries and career duration. Pension (and disability) benefits are financed by large investment pools, which in turn are replenished by tax-funded employer contributions. Some public employees, depending on their hire date, also contribute a small share of their own salaries to pension funds.

While employee contributions (where required) are fixed or capped, contributions by employers fluctuate, depending on the rate of return on pension fund assets. Since the mid-1980s, when pension funds began allocating more of their assets to equities, those rate of return assumptions have ranged from 7.5 percent to 8.75 percent; for most of the last 10 years, New York’s public pension plans have assumed their investments would produce a return of 8 percent annually.

Stock returns went through the roof during the bull markets of the 1980s and 1990s, and by the end of the century employer pension contribution rates were barely above zero. This situation clearly could not last. The 10 years starting in 2000 saw two sharp market contractions resulting in hardly any net gain for major indexes by the end of the decade. Interest rates have hovered near record lows since the financial crisis in 2008. Meanwhile, the number of retirees has continued rising, and retirement benefit payments have more than doubled during the same period. Taxpayers must make up for the shortfall, which has translated into a $12 billion increase in pension contributions since 2001.

Article 5, Section 7 of New York’s Constitution guarantees that pension benefits shall not be “diminished or impaired”—which is widely assumed to mean that employees cannot be required to help pay for the rising costs for their future benefits, even benefits they have not yet accrued. This has been interpreted to mean that benefits for all current workers can never be changed or interrupted. As a result, pension plans are organized into “tiers” based on hiring date, with each successive tier representing an attempt to curb benefits or reform the excesses of previous ones.

Governor Cuomo’s proposed Tier 6 would raise employee contributions, reduce benefit multipliers, and increase the retirement age and vesting period for most defined-benefit pensions. In a break with previous tier reform patterns, Cuomo also has proposed allowing state and local employees to opt into a defined-contribution plan. Instead of a single common retirement fund, a defined-contribution plan consists of individual accounts supported by employer contributions, usually matched at least in part by the employees’ own savings. Defined-contribution retirement plans are not new to New York State. As detailed in the next section, SUNY and CUNY employees have had such an option for nearly 50 years.

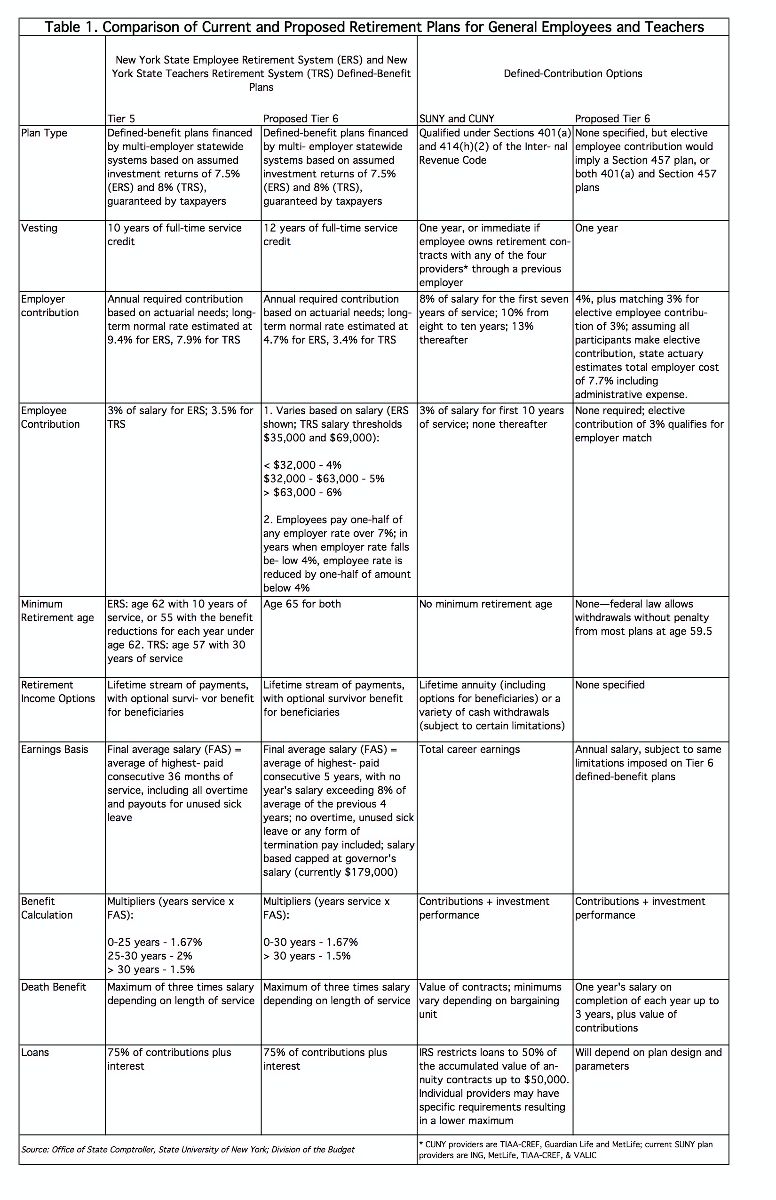

Table 1, below, compares proposed Tier 6 and existing Tier 5 pensions for state and local employees outside New York City and the SUNY and CUNY optional defined-contribution program.

2. CHOICE FOR HIGHER EDUCATION EMPLOYEES

Since 1964, the State University of New York has given faculty and other employees a choice between traditional public pension plans and personal investment accounts whose performance determines the amount of retirement income. The City University of New York began offering the same choice in 1968. (See “Made-in-New York Pension” Reform on pages 8 and 9 for more historical background.)

TIAA-CREF was the sole provider of SUNY retirement plans until 1994, when units of MetLife, ING Group and VALIC were added to the list of eligible vendors. At CUNY, the vendors are TIAA-CREF, Guardian Life and MetLife. TIAA-CREF has the largest share of accounts at both institutions.

Total contribution rates for new employees joining the defined-contribution plans are 11 percent a year during the first seven years of service and 13 percent thereafter — levels that were designed to roughly approximate the “normal” cost of defined-benefit pensions under the Tier 4 plan. Employees contribute 3 percent of salary during their first 10 years of service, but thereafter contribute nothing, so the employer share is 8 percent during the first seven years, 10 percent during years eight through ten, and 13 percent thereafter.[i]

“401(k)-like” — not!

Federal law over the past 40 years has given rise to a variety of tax-deferred, employer-sponsored retirement savings vehicles, of which the 401(k) is the best-known and most popular type in the private-sector. Indeed, “401(k)” has become a synonym for all defined-contribution plans, and the phrase “401(k)-like” has often been used to describe Governor Cuomo’s proposal to offer a defined-contribution option to New York’s state and local employees.

However, the SUNY and CUNY retirement plans differ from 401(k) accounts in several important respects.

To begin with, the 401(k) designation itself is limited to the private sector, except for a number of states (excluding New York) that had such plans “grandfathered” under the 1986 federal tax reform.

The SUNY and CUNY plans are qualified under Section 401(a) of the Internal Revenue Code, which authorizes tax-deferred employer-sponsored retirement plans in the government sector.[ii] While 401(k) contribution levels can fluctuate at the discretion of both employers and employees, contributions to a 401(a) plan are fixed by the employer. The total contribution can vary based on factors such as career longevity, but 401(a) plan parameters do not allow for the voluntary “matching” incentives provided under many 401(k) plans. Employers and employees cannot choose to opt out of making their full required contributions.

The other big difference between a standard 401(k) plan and New York’s higher education 401(a) plans is the form of the investment vehicles they offer. First authorized in 1978, 401(k) accounts typically offer a range of professionally managed mutual fund investments in stocks, bond or money market instruments. Employees can directly manage their own accounts through plan administrators, and can draw on the accumulated investments when they retire.

Participants in the optional SUNY and CUNY plans must deposit their funds in annuity contracts. These investment vehicles, managed by insurance companies, are designed to accumulate wealth and provide a stream of income in retirement.[iii] While 401(k) plans tend to focus mainly on wealth accumulation alone, the focus of annuity-based plans is more on retirement income.[iv]

About annuities

Annuity contracts vary widely in their details and prices, but those offered at SUNY and CUNY all promise payments for the life of the retiree (the “annuitant,” or a beneficiary he or she designates). Annuitants and beneficiaries give up their remaining investment value at death in exchange for protection against the risk of outliving their assets. The SUNY plan allows annuity contracts to be easily converted to lifetime annuities at retirement.

Variable annuities are accounts similar to mutual funds, which can be invested in stocks, bonds, or a combination of the two, and can be converted at retirement from a savings accumulation mode to an income payout mode. TIAA-CREF’s variable annuities for retirees currently pay a rate equal to 4 percent of the value of the investment fund—plus the annual return of principal, which varies according to the age of the annuitant when distributions begin after retirement. The dollar value of the 4 percent distribution fluctuates with the value of the investments.

The two university plans also offer annuities backed by insurance companies, which rely on their own investment portfolios (bonds, real estate and stocks) to make the promised payments. The companies annually determine how much they can afford to pay as dividends, above a minimum annuity guarantee for accumulations and payouts.

Among SUNY and CUNY employees opting for the defined-contribution plan, the most popular insurance annuity is TIAA’s “Traditional” product. When illustrating the potential benefits the Traditional Annuity, TIAA-CREF uses an assumed rate of 6 percent for payouts, plus the gradual return of principal. While only a 2.5 percent return on the amount invested is guaranteed, the company has declared a higher dividend every year since 1948.[v] Interest rates paid by the fund in the accumulation stage have gradually declined in recent decades, from 10.81 percent for contributions made in 1985 to 3 percent currently.[vi]

The chief disadvantage of an insurance annuity is that it does not offer the higher returns possible from stocks. By the same token, it can shield investors from the risk of sudden, sharp decreases in stock prices.

This was illustrated during the volatile past decade on Wall Street, which was the worst for the stock market since the 1930s. During the 10 years ending in December 2011, funds deposited in a CREF variable annuity stock account yielded an average return of 3.49 percent, while a TIAA Traditional retirement annuity yielded 5.3 percent, according to figures provided by the company. SUNY or CUNY employees dividing their investments evenly between TIAA and CREF funds would have thus realized an annualized gain of 4.4 percent a year during that period. The 20-year return from the same fund was 6.73 percent.[vii]

The income promised by an insurance annuity ultimately is no more or less secure than the company writing the contact. TIAA-CREF is the most highly rated of the four vendors in the SUNY plan, and the other vendors all have credit ratings in at least the mid to high range of investment grade. In case of insurance company insolvencies, the Life Insurance Company Guaranty Corp. of New York is required to make good on up to $500,000 of annuity benefits per individual per company.[viii]

All lifetime annuities in the SUNY plan pay benefits only for the life of the account holder, or for a surviving spouse or other beneficiary. When annuitants and their beneficiaries die, the insurance company keeps the remaining principal amount. The remaining principal from annuitants who died before collecting their principal is used for payments to those who live longer than expected. Long-lived annuitants continue to receive benefits even after collecting all of their principal.

As of late 2011, neither SUNY nor CUNY was collecting data indicating the extent to which their employees were choosing to convert their accounts to lifetime annuities upon retirement. According to TIAA-CREF, about 70 percent of all annuity accounts are now converted to retirement annuities, down from 90 percent in the mid-1980s. Low interest rates and concern about rising health care costs and possible cuts to the Medicare program may be among factors influencing the reluctance of retirees to tie up more of their savings in annuity contracts.[ix]

Charges, fees and investments

The promise of lifetime income, like any financial benefit, comes at a cost. An annuity typically comes with a fee known as the “mortality and expense” or M&E charge, which pays for the insurance guarantee, sales commissions and administrative costs. This charge is expressed as a percent of the fund balance and is deducted from what employees and annuitants earn.

According to the Securities and Exchange Commission, the average M&E fee for a variable annuity is about 1.25 percent. TIAA-CREF comes in far below this benchmark, with M&E charges ranging from 0.005 percent or 0.05 percent depending on the fund. MetLife charges an M&E of 0.75 percent, plus an administrative charge of 0.20 percent.[x] ING charges an administrative fee of 0.25 percent and an M&E of 0.75 percent to 0.85 percent during the accumulation phase and 1.25 percent during distribution.[xi] VALIC says its annuity insurance charges range from 0.75 percent to 1.25 percent, and may be reduced for specific programs.[xii]

Each of the four SUNY vendors offers about 30 funds, including stock and bond index funds (intended to track a market index such as the S&P 500), in some cases managed by an outside firm. The vendors also offer funds with ready-made mixes of stocks and bonds in proportions that don’t change much, designed to appeal to investors with different levels of risk aversion. The MetLife Aggressive Strategy Portfolio, for example, aims to be 100 percent invested in stocks, which would offer the potential for greater appreciation and higher risk of loss than the MetLife Conservative Allocation portfolio, which aims for 80 percent bonds and 20 percent stocks.

Other providers provide so-called “target funds” that automatically adjust a portfolio as they near a specified target date, or as gains or losses push the fund away from its desired mix of securities. The ING Index Solution 2045 Portfolio, intended for those expecting to retire in the year 2045, was 95 percent invested in U.S. and foreign stocks with 5 percent of its assets in U.S bonds. It plans to stick to that approximate ratio until 2015 when it begins gradually moving to a mix of 35 percent stocks and 65 percent bonds in 2045. ING’s 2025 portfolio currently has a mix of 70 percent equities and 30 percent bonds, and is supposed to adjust that mix by its target date.

Although TIAA-CREF’s annuity charges are low by industry standards, the performance of its variable annuities has not been immune from criticism. In 2007, a group of Claremont University professors published a comparison study concluding that, over a 20-year period, an employee with an expanded menu including standard index funds could gain 25 percent to 40 percent in standard wealth compared to a worker restricted to TIAA-CREF options.[xiii] TIAA-CREF strongly contested this, citing what it called “serious omissions and flawed methodology.”[xiv]

Advisory services

Investor education in the SUNY and CUNY plans is left to the providers, paid for by the fees they on impose buyers of their funds. By having more providers, the university has created an element of competition among them, at least in terms of providing education and service to SUNY workers.[xv]

All four companies are required to have representatives available on all 64 campuses of the SUNY system. The for-profit investment providers, MetLife, VALIC, and ING, pay their representatives at least in part, with commissions on sales. However, TIAA-CREF financial advisors and consultants are not paid commissions. The company says they are paid a basic salary plus a bonus based mostly on quality of service, as measured by questioning plan participants after meetings or transactions with TIAA-CREF. The advisors are also graded on how many people they meet, educational sessions conducted and new accounts generated.[xvi]

CUNY’s optional retirement plan[xvii] is very similar to SUNY’s. All workers selecting the optional retirement plan are enrolled in TIAA-CREF, which offers the same array of investment options as in the SUNY plan. After one year, workers may transfer to either Guardian Life Insurance or MetLife, each of which offers a menu of variable annuities.

Supplemental retirement savings accounts

SUNY and CUNY workers who want more savings than the retirement plan provides may join the university systems’ 403(b) plans or the New York State Deferred Compensation Plan, which is qualified under section 457 of the tax code.[xviii] Section 403(b) plans, also called tax-deferred annuities, are offered to workers at public schools and not-for-profit, tax-exempt groups. SUNY’s 403(b) plan allows investments in variable annuities from the same insurers who handle the 401(a) plan, and a menu of ordinary mutual funds offered by Fidelity Investments. CUNY workers can select variable annuities from either TIAA-CREF or Lincoln Life and Annuity Co.

Each plan allows pre-tax contributions by the employee of up to $17,000, with an additional $5,500 catch-up allowed for those age 50 and older. Additional contributions of up to $3,000 per year for a maximum of $15,000 are allowed in the 403(b) account for those with more than 15 years service, in addition to the catch-up. Participants in the 457 plan who are within three years of age 55 may increase their contributions up to twice the limit or the unmade allowable contributions from previous years, whichever is less.

Withdrawals from the 403(b) plan before age 59½, unless part of an annuity contract, incur a 10 percent federal tax, like Individual Retirement Accounts and 401(k) plans. The 10 percent penalty doesn’t apply to 457 plan balances, unless they have been transferred to or from an account covered by the penalty, such as an IRA.

Distributions from the investment accounts are allowed anytime after SUNY employment ends, and can be done through periodic withdrawals, a lump-sum cash distribution or the purchase of a lifetime annuity. In any form, the distributions are subject to federal income tax, either in one payment for a large cash withdrawal, or gradually over time as with annuity payments. Federal tax law requires minimum distributions to begin after employees turn 70½ or they terminate employment, whichever comes last.

Distributions via an annuity can begin at any age after SUNY employment ends. Workers typically leave the account with the insurer, where investment gains remain tax-deferred, or they transfer the cash value of the accounts to another savings plan, such as an individual retirement account or a 401(k) plan. Accounts at outside plans cannot be transferred to the SUNY optional retirement program.

________________________________________________________________________________________

ENDNOTES 2

[i]For SUNY employees hired before July 26, 1976, the employer pays a full 12 percent on the first $16,500 and 15 percent of salary above that level.

[ii]Under a separate section of law, Section 414(h)(2), employee contributions to the SUNY and CUNY plans are technically considered a “pick-up” by the employer. This added qualification is important; without it, the plan could have to be supported by the employer alone.

[iii]Sections 180 to 187 of the state Education Law, which authorized the SUNY Optional Retirement Program, refer to “contracts providing retirement and death benefits,” and authorize SUNY to select “insurers” to manage them. This language was originally written with TIAA-CREF in mind, and effectively referred to annuities without specifying them.

[iv]John H. Biggs, “How TIAA-CREF Funded Plans Differ From a Typical 401(k) Plan,” TIAA-CREF Institute, Trends and Issues, February 2010.

[v]TIAA Traditional Annuity: Adding Safety and Stability to Retirement Portfolios, at http://www.tiaa-cref.org/ucm/groups/content/@ap_ucm_p_tcp/documents/document/tiaa01011136.pdf

[vi]http://www.tiaa-cref.org/public/performance/retirement/index.html#TIAA-CREFFunds-RetirementClass

[vii]By comparison, the total return by the S&P 500 during the same 10-year period averaged 2.87 percent a year.

[viii]Opinion letter from State of New York Insurance Department, February 11, 2008 at http://www.dfs.ny.gov/insurance/ogco2008/rg080206.htm

[ix]Timothy Lane, managing director TIAA-CREF, interview September 8, 2011

[x]Holly Sheffer Liapis, assistant vice president MetLife, e-mail message, September 12, 1011

[xi]ING, “SUNY Optional Retirement Program,’’ at http://www6.ingretirementplans.com/SponsorExtranet/SUNY/YourPlanHighlights/index.html

[xii]VALIC, “Portfolio Director Fixed and Variable Annuity, Prospectus May 1, 2011, at http://www.valic.com/Images/pd_contract_tcm82-14920.pdf, See section labeled Separate Account Charges

[xiii]John Angus, William O. Brown, Janet Kihlom Smith, and Richard Smith, “What’s in Your 403(b)? Academic Retirement Plans and Costs of Underdiversification,’’ Financial Management, Vol. 36, Issue 2 at http://www.fma.org/FinMgmt/FinMgmt/Summer2007/FM10_Angus.pdf

[xiv]“Serious Omissions and Flawed Methodology Mar Academic Paper About Diversification in 403(b) Plans,” TIAA-CREF Fact Sheet, October 2007.

[xv]Morrell, interview September 7, 2011

[xvi]Lane, interview August 9, 2011

[xvii]City University of New York, Summary of Benefits, Full Time Instructional Staff at http://www.cuny.edu/about/administration/offices/ohrm/university-benefits/INSTRUCTIONALSTAFFMANUALspring2009.pdf, CUNY optional retirement system described on pages 32-36

[xviii] SUNY, “Voluntary Retirement Savings Programs,,’’ at http://www.suny.edu/BENEFITS/retirement/403b%20-%20457%20Comparison.pdf

________________________________________________________________________________________

3. DEFINED-CONTRIBUTION ADVANTAGES

For taxpayers, a defined contribution plan offers complete transparency and predictability—attributes the defined-benefit pension system has long lacked.

The current scale of employer contributions to SUNY and CUNY optional plans was designed to roughly equal the long-term expected “normal” contribution rates for Tier 4 of the state and local pension plans for general employees outside New York City. That rate, based on a hypothetical steady state of asset returns matching the pension fund’s ambitious 8 percent target, ranged from 11 to 12 percent, with a 3 percent employee contribution ending after 10 years’ service.

But the actual employer rate almost never aligns with the normal rate. Instead, it fluctuates with investment returns—from low single digits in the late 1990s to much higher levels today.

New York City’s pension funds, historically have demanded higher employer rates than the state plan. For CUNY, in particular, the defined-contribution plan represents a significant savings. As of 2011, the employer rate of contribution to the New York City Teachers’ Retirement System was over 30 percent of salary, compared to between 8 and 13 percent for members of the defined-contribution plan in both university systems.

The New York State Employees Retirement System, the main pension alternative for SUNY employees, currently charges an employer contribution rate of 16.5 percent, which is expected to rise to 23.1 percent by 2015.[i] The New York State Teachers’ Retirement System is currently charging an average employer rate of 11 percent, but current trends point to a peak rate of 18 percent by 2015.[ii]

From an employee’s standpoint, the primary advantage of a defined-contribution is the same one Nelson Rockefeller cited when he proposed the SUNY option almost 50 years ago: portability. It protects workers who leave the system for any reason—their own choice, for example, or simply to follow a spouse taking a new job out of state.

Members of traditional defined-benefit pension systems are not entitled to any benefit until they have “vested” in their plan. The vesting period for the current Tier 5 pension plan is 10 years, and the proposed Tier 6 plan would extend that to 12 years.

As Governor Cuomo put it: “Maybe some people don’t want to sign on as a lifetime employee. Ten years is a long time. They want to work a few years, get the benefits, and take a portable defined-contribution benefit to their new job.”

There are potentially quite a few people in that category.

The mobile many

In the five years ended 2010, almost 110,000 state and local government workers outside New York City left their jobs before vesting in their retirement benefits. The number includes about 85,000 withdrawals from the New York State Employee Retirement System (NYSERS)[iii] and about 24,000 from the New York State Teachers’ Retirement System (NYSTRS), which covers K-12 professional educators and some college instructors.[iv]

Employees who leave a state or local payroll before vesting can withdraw their own pension contributions, which amounted to 3 percent of salary for ERS and 3.5 percent for NYSTRS. The actuarial calculations for NYSERS assume the system will earn 7.5 percent on its investments, while the NYSTRS assumes a return of 8 percent, but both systems will pay only 5 percent interest on pension fund contributions withdrawn by non-vested employees.

Those who leave government jobs before vesting effectively forfeit part of their compensation by giving up all of the retirement benefits attributable to employer contributions, which are retained by the system to help meet obligations to vested and career workers.[v] This subsidy of the long-term workers by the short-term workers, together with permissive accounting standards that understate long-term liabilities, is a reason why defenders of defined-benefit pension systems can claim they are “less expensive” than defined-contribution systems.[vi] In a defined-contribution system, by contrast, employees vest in their benefits after one year. Once vested, they can withdraw all of the money contributed to their accounts, including the employers’ share. The difference this can make to an individual worker is illustrated in the table below.

A hypothetical employee with a starting salary of $40,000 who leaves the system after four years could take with her $20,378 in contributions from the SUNY optional defined-contribution plan, compared to just $5,558 for ERS or $6,484 from TRS. If reinvested at an assumed average rate of return of 5 percent, her retirement benefit in 30 years would have grown to $88,073 – roughly $60,000 more than the value of the TRS withdrawal and $64,000 more than the value of the ERS withdrawal.

The differences for an unvested employee leaving a government job after eight years are even more striking. Thirty years later, the savings this employee transferred from the SUNY optional defined-contribution plan would have grown to more than $211,000, dwarfing the value of a TRS or ERS pension fund withdrawal by that time.

An added, often overlooked advantage of a defined-contribution system is the death benefit. A member of the defined-benefit system is eligible for a death benefit equal to a maximum of three times salary, depending on length of service. Designated beneficiaries of SUNY or CUNY defined-contribution plan members receive the full value of the employee’s annuity contract. After mid-career, this amount is likely to exceed three times salary.

The choice between defined-benefit and defined-contribution plans represents a significant trade-off. Under the state Constitution, a defined-benefit pension is absolutely guaranteed. Employees in the traditional pension system thus don’t need to worry (or even think) about market risk. As noted above, when pension funds lose money or fall short of their investment goals, added contributions from taxpayers must make up the difference.

Those guaranteed benefits offer high levels of income replacement for career employees. Under Tier 5, a teacher or general employee can retire at age 65 after 40 years of service with a pension equivalent to 77 percent of final average salary, calculated as three consecutive years of peak pay. When Social Security benefits are added to the mix, the longest serving general employees and teachers in the state and local system typically are replacing more than 100 percent of their peak annual earnings while working. The governor’s Tier 6 proposal would reduce the 40-year benefit to 65 percent of final average salary, which would be calculated on the basis of five peak salary years (see Table 1).

Under the right conditions, a lifetime annuity for a hypothetical TIAA-CREF plan participant at SUNY or CUNY could approach the defined-benefit pension available under a Tier 5 plan, according to TIAA-CREF calculations shown in Table 3, below.

The assumed average rate of return on investments is the most crucial variable in determining retirement income for participants in defined-contribution plans. Assuming a 6 percent return rate through retirement, TIAA-CREF estimates an employee who starts working at age 25 could retire at 65 with an annual annuity equivalent to 73 percent of his final salary—not as much as a Tier 5 benefit would have been, but better than the proposed Tier 6 benefit.

Timing is everything

Of course, markets in real life don’t produce smooth, unvarying returns—any more than defined-benefit pension plans in the public sector charge employers a steady and predictable contribution rate. Salary progressions over the course of an employee’s career are also bumpier than a smooth hypothetical assumption would suggest. The timing of market returns in relation to changes in salary can also make a significant difference in retirement income.

This can be illustrated using actual salary histories of two anonymous members of traditional pension systems—a state employee who belonged to NYSERS, and a Capital Region public school teacher covered by NYSTRS. The two employees both retired as of July 1, 2010, at nearly identical salaries of $91,952 for the state employee (a Grade 25 professional and technical employee) and $92,309 for the teacher. The state employee joined the system in mid-1974, earning $10,532, while the teacher began working in September 1975 for a salary of $9,220.

Retirement accumulations and annual annuity incomes for these employees were computed as if they had been enrolled in TIAA-CREF 50-50 plans at the time of their employment, assuming a total contribution rate of 12 percent of annual salary throughout the period. The result: the state employee would have accumulated savings of just over $800,000, which could be converted into an annuity of $55,080, or 60 percent of final salary. The teacher would have accumulated $547,744, convertible to an annual annuity of $37,510, or 41 percent of income.

Why the disparity for two employees who worked almost the exact same period, ending at similar salary levels?

Answer: the state employee’s salary started higher and increased faster between the mid 1980s and mid 1990s, when investment returns were strong. The teacher’s salary peaked after 2000, just as investment returns had begun to fall. These comparisons point up the importance of creating investment strategies to help employees minimize the negative impact of market downturns late in their careers.

How have actual participants in SUNY and CUNY plans fared? The answer is illustrated in Table 4, below.

At our request, TIAA-CREF calculated projected fund accumulations and annuity incomes for long-serving SUNY and CUNY employees now in the immediate pre-retirement phase of their careers. The projections assume retirement at age 65 and salary growth of 2 percent a year before retirement. Total accumulations and annuity values were modeled based on two different scenarios—Low Growth (4 percent return on investments) and High Growth (6 percent before and after retirement).

The results:

- The oldest and longest-tenured members of the SUNY and CUNY plans—employees in their late 60s and early 70s, with at least 36 years of service—on average have accumulated more than $1 million in their TIAA-CREF accounts. If they retire immediately, their annual annuities would typically replace a minimum of 62 percent of income under the Low Growth scenario and 76 percent under the High Growth scenario.

- Those in the immediate pre-retirement category — aged 60-64 with at least 36 years of service—have accumulated an average of $905,000 at SUNY and $823,000 at CUNY. Under the Low Growth scenario, these amounts ultimately can be converted to annuities providing retirement income equivalent to 58 percent and 56 percent of final salary. Under the High Growth scenario, the annuity income increases to 72 percent and 74 percent, respectively.

- Employees aged 55 to 59 with 31 to 35 years of service currently have average fund accumulations of $566,852 at SUNY and $543,508 at CUNY. Under the Low Growth scenario, these accumulations will grow sufficiently to be converted into annuities averaging 50 percent for each group. Under the High Growth scenario, the projected annuity income 69 percent of final salary for the SUNY employees and 70 percent for the CUNY employees.

Social Security benefits[vii] will typically be equivalent to about 20 percent of late-career annual earnings for these workers, bringing the lowest total income replacement ratio to at least 70 percent (for the 55-59 cohort) under the Low Growth scenario for future returns. Under the Higher Growth, the minimum income replacement value of the annuity and Social Security rises above 90 percent.

SUNY and CUNY employees within 10 years of turning 65 saw their retirement savings were hit hard by financial crisis and stock market plunge of 2008. At least some have no doubt responded by working longer than they might have planned a few years ago. But as these figures show, even in an economic and market environment that has amounted to a worst-case investment scenario for late-career workers in defined-contribution plans, SUNY and CUNY employees with TIAA-CREF contracts are positioned to replace a large share of their current salaries in retirement.

It should be noted that SUNY and CUNY employees hired before July 1976 benefitted for most of their careers from a contribution rate of 15 percent on the portion of their salaries above $16,500, compared to the maximum 13 percent rate available under the current plan. For those hired between 1976 and 1992, the contribution rate rose to 15 percent of amounts above $16,500 after their first 10 years of service. This higher rate helped ensure that employees in these age groups were able to end their careers with a substantial savings cushion.

_______________________________________________________________________________________

ENDNOTES 3

[i]State of New York, 2012-13 Executive Budget, Financial Plan, p. 78. The state is “amortizing”(i.e., spreading out over 10-year periods and repaying with interest) a portion of its pension payments each year, reducing the effective rate to 10.5 percent in 2012 and 13.5 in 2015.

[ii]Updated projection by Josh Barro, senior fellow with the Manhattan Institute.

[iii]Edward R. Freda, actuary in Office of State Comptroller, e-mail message, July 26, 2011

[iv]John Cardillo, manager of public information at New York State Teachers Retirement System, telephone communication, July 27, 2011

[v]In years when investment returns have driven the employer contribution down to low levels or even zero, excess returns attributable on an actuarial basis to employee contributions are absorbed by the fund.

[vi]Annual Report to the Comptroller on Actuarial Assumptions, 2010, Active Member Decrements, p 30 at http://www.osc.state.ny.us/retire/word_and_pdf_documents/publications/annual_actuarial_assumption_report/actuarial_assumption_2010.pdf, page 30 Active Member Decrements

[vii]Assumed “Scaled-Medium” Social Security earnings of $17,134 for 2011, adjusted for assumed 2.5 percent inflation to nominal $22,841, when employees in their mid to late 50s as of 2011 will reach full Social Security retirement age of 66. See Social Security Online, Actuarial Publications, “Annual Scheduled Benefit Amounts for Retired Workers With Various Pre-Retirement Earnings Patterns Based on Intermediate Assumptions,” at http://www.ssa.gov/OACT/TR/2011/lr6f10.html

_______________________________________________________________________________________

4. THE OPTION EMPLOYEES DESERVE

Counter to predictions of some who are opposed in principle to any defined-contribution retirement plan, the participants in TIAA-CREF defined-contribution plans at SUNY and CUNY will not be impoverished or financially insecure when they can no longer work. Far from it. While they cannot match the guaranteed benefits of contemporaries who spent careers in traditional public pension plans, their total retirement incomes will average at least 70 percent of final salary. By converting to a lifetime annuity, they can be assured that they will not outlive their money.

How much income replacement can be considered “adequate” in retirement? The definition has shifted over the years and is open to dispute. While the standard benchmark for many years was 70 percent, a series of reports Georgia State University/Aon RETIRE Project has suggested a range of 78 to 94 percent depending on pre-retirement income levels.[i] This finding, in turn, has been the basis for subsequent research suggesting that Americans in general are grossly under-saving for retirement, giving rise to a “retirement crisis.”

But the use of a one-size-fits-all income replacement benchmark has been disputed by other researchers, who suggest the concept is flawed and misleading because it fails to take account of differences in household consumption patterns and needs.[ii] In any case, as noted in this report, career state and local employees in New York can now retire with a combination of pension and Social Security benefits exceeding 100 percent of their final average salaries —more than adequate by any standard.

If an income replacement ratio is accepted as a desirable goal, even if not demonstrably necessary in all cases, recent research offers a framework for considering the amount of money that should be put aside in a defined-contribution or other personal retirement savings plan. A 2007 study, taking account of variability investment returns, suggested that the savings rate of a 25-year-old aiming to replace 80 percent of a $60,000 income should be pegged at 12 percent.[iii] Approaching the question from a different perspective, a TIAA-CREF research paper in 2008 also recommended a “core” total contribution rate of 12 percent a year over a 35-year career to achieve benchmark income replacement ratios in retirement.

Getting the rate right

The average employee contribution to 401(k) plans was 6.8 percent in 2010, with 21 percent of workers paying more than 10 percent, according to data compiled by the Vanguard investment management company. The most common employer contribution was a 50 percent match of employee contributions, up to 6 percent of income, or 3 percent for an employee contributing 6 percent. Total contribution rates averaged 9.7 percent, with a median of 8.8 percent.[iv] As previously noted, total annual contributions to the SUNY and CUNY plan currently are 11 percent during the first seven years, and 13 percent thereafter.

Governor Cuomo’s proposed defined-contribution plan would require a minimum employer contribution of 4 percent of salary, with no required contribution from employees. State and local employers would be required to match a voluntary employee contribution of 3 percent, which would bring the total funding level to 10 percent per year. The defined-benefit option under his Tier 6 plan would require employee contributions ranging from 4 to 6 percent, depending on income (see Table 1)

Given a choice, many younger and lower-paid employees just starting a state or local government job may choose a plan requiring no contribution from them. But if the public policy objective is to offer an alternative plan that actually provides the foundation for an adequate income at retirement, even if retirement is far in the future, a minimal total contribution of 4 percent is not enough. Even the 10 percent combined level under the elective feature of the governor’s proposal is lower than the lowest combined contribution rate under the SUNY and CUNY plans.

To emulate the solidity and success of the SUNY and CUNY plans, the contribution rate should be at least 12 percent, if not higher. In line with the proposed Tier 6 defined-benefit plan, employee contribution rates should range from 4 to 6 percent based on salary, complemented by an employer contribution ranging from 6 to 8 percent, bringing the total to 12 percent. In addition, the contribution should be a percentage of all wages without limit, including overtime, differential and termination pay, since concerns about late-career pension “spiking” that prompted these limitations in the defined-benefit sections of the governor’s Tier 6 proposal are not relevant to a defined-contribution plan.

In a low-interest rate, low-growth environment, however, many employees will want and need to save more. To encourage higher savings, the Section 457 Deferred Compensation Plan should be promoted as a complement to the core defined-contribution account.

The state should also explore the applicability of provisions in the 2006 federal Pension Protection Act that make it easier for an employee to automatically earmark a portion of future salary increases to retirement savings. This auto-save feature would need to apply to the 457 Deferred Compensation Plan or some other supplemental plan, since a core 401(a) plan modeled on the SUNY and CUNY option could not allow for voluntary additional employee contributions.

A maximum employer contribution of 8 percent would still fall below the expected long-term normal rate of 11 percent for Tier 4 employees and 9.4 percent for Tier 5 employees who belong to the New York State Employees’ Retirement System. The rate for Tier 6 defined-benefit pensions has been projected at just 4.7 percent for state and local employees outside New York City—but all such calculations for the defined-benefit plan reflect actuarial assumptions that assume a long-term investment return of 7.5 percent (in the case of NYSERS) or 8 percent (in the case of the NYSTRS). Employers will remain unable to predict their actual contribution rate to the defined-pension plan more than a year or two ahead of time.

By contrast, contributions to a defined-contribution plan will be level, predictable—and free of accounting distortions that undermine the reliability of traditional pension financial projections.

Plan design issues

The annuity feature at the heart of the SUNY and CUNY defined-contribution plans is designed to ensure a steady stream of retirement income and to serve as a form of insurance against outliving assets. Annuity contracts (giving employees the flexibility for employers to choose mutual funds if they desire) should be a default investment under the new defined-contribution option.

The benefits of annuities are increasingly being recognized as the retirement needs of baby-boomers become more pressing.

“Promoting the availability of annuities and other forms of guaranteed lifetime income, which transform savings into guaranteed future income, reducing the risks that retirees will outlive their savings or that their retirees’ living standards will be eroded by investment losses or inflation,” was among the 2010 recommendations of the White House Task Force on the Middle Class, chaired by Vice President Joe Biden.[v] Consistent with this recommendation, the U.S. Treasury Department recently issued regulations designed to make it easier for middle-class retirees to transfer private 401(k) assets to guaranteed lifetime annuities.[vi]

In setting up a new defined-contribution option, the state’s plan sponsors—designated in Cuomo’s bill as the retirement systems sponsoring traditional pensions—should require that the default investment plan be life-cycle or target date accounts rather than money-market funds. They should seek to minimize administrative costs and investment fees and centralize record-keeping with a single vendor, while allowing more than one insurer or financial institution to offer plans. They should also find ways to package the plan with group disability and term life insurance, on an optional basis for employees willing to pay extra for it. And they should explore ways of using annuities during the savings accumulation phase to cushion themselves against the risk of late-career financial market downturns, as experienced by workers now approaching retirement at SUNY and CUNY.

________________________________________________________________________________________

ENDNOTES 4

[i]Bruce A. Palmer, 2008 GSU/Aon RETIRE Project Report, Research Report Series: Number 08-1, June 2008, at http://rmictr.gsu.edu/Papers/RR08-1.pdf.

[ii]William G. Gale, John Karl Scholz, Ananth Seshadri, “Are All Americans Saving for Retirement?” Brookings Institution (Gale) and University of Wisconsin-Madison (Scholz and Seshadri), Preliminary Paper, Dec. 31, 2009, atwww.ssc.wisc.edu/~scholz/Research/Optimality.pdf

[iii]Roger Ibbotson, James Xiong, Robert P. Kreitler, Charles F. Kreitler and Peng Chen, “National Savings Rate Guidelines for Individuals,”Journal of Financial Planning, April 2007, www.journalfp.net.

[iv]Vanguard Group, “How American Saves 2011’’ at https://institutional.vanguard.com/iam/pdf/HAS11.pdf

[v]White House Task Force on Middle-Class Working Families, “Fact Sheet: Supporting Middle Class Families,” (January 2010), http://www/whitehouse.gov/sites/default/files/Fact-_Sheet-Middle_Class_Task_Force.pdf

[vi]“New Treasury Rules Ease 401(k) Annuity Purchase,” The New York Times, Feb. 3, 2012, p.B4.

_______________________________________________________________________________________

CONCLUSION

“Why wouldn’t you want to give the person the option?”

That’s how Governor Cuomo summed up the argument for the voluntary defined-contribution plan in presenting his 2012-13 budget.[i] The governor is breaking new ground for New York by seeking to allow all public employees to select a personal and portable plan.

But the governor and Legislature should not settle for a plan that emulates a stripped-down 401(k) while being “much cheaper for the state,” as Cuomo put it. While the traditional pension system has fundamental, structural problems that the Tier 6 legislation would not address, provisions creating a defined-contribution option should draw from the best features of the SUNY and CUNY plans and best practices in the retirement planning field.

Almost a century ago, New York was the birthplace of the annuitized private pension for college professors. Almost 50-years ago, it was the first major state to sponsor an annuity-based defined-contribution option to a large group of its employees. The push for a universal defined-contribution option for all New York state and local workers is an opportunity to create a model for both public and private sector employers in the 21st century.

_______________________________________________________________________________________

ENDNOTES CONCLUSION

You may also like

The Janus Effect

The U.S. Supreme Court in 2018 ended New York’s decades-long practice of forcing state and local government employees to pay a labor union as a condition of employment. Read More

HEMMED OUT: Why Legislative Employees Can’t Unionize Under the Taylor Law

Union advocates have argued that employees of the New York State Legislature are covered by the Taylor Law, the 1967 state law that requires state and local public employers, including state agencies, municipalities, and school districts, to recognize and Read More

Tiering Up

New York taxpayers have been hit with enormous increases in pension costs for state and local government employees over the past 20 years. From less than $1 billion in 2000, combined annual employer contributions to the Empire State’s public pension funds escalated to nearly $10 billion by 2010, peaking at nearly $17 billion in 2015. Contributions have leveled off at roughly $16 billion in recent years—but under lenient government accounting standards, even that figure conceals the full long-term cost of generous, locked-in pension benefits for generations of retired government employees. Read More

Keep the Change

As the pandemic subsides and Cuomo’s emergency orders expire, the state should take some of what he has done by fiat and keep the change. Read More

Dealing In The Dark

State law doesn’t require secrecy around union negotiations, but local governments and school districts have come to believe it does. At the same time, the law fails to give the public a chance to review contracts before they’re ratified, and doesn’t require any calculations that would show the long-term effects on costs.

Read More

What Happens If Teachers Go On Strike?

New York’s largest teachers union this summer threatened to go on strike rather than allow schools to reopen for in-person classes—despite months of preparation by officials and a state law that prohibits union work stoppages. Read More

Double Insulation: How New York Law Shields Public Employees From Accountability

The rules governing public employment in New York are expressly designed to make it time-consuming and expensive to hold workers accountable for poor performance or misconduct. Read More

Dues & Don’ts

New York’s public-sector collective bargaining law, the Taylor Law, is unique in that it’s the only law that people risk breaking by discussing it. The Empire Center launched “Dues and Don’ts” to help public employers fulfill their obligation to educate employees about their rights without fear of improper practice charges under the Taylor Law. Visit the Dues & Don'ts website to learn more. Read More