Before the Joint Legislative Fiscal Committees

February 23, 2021

In economic terms, the coronavirus pandemic has been the most disruptive event to hit New York and the nation since the Great Depression in the early 1930s. While New Yorkers hope to resume to some semblance of normal life by summer, the fiscal hangover for the state and its local governments will linger for years.

Despite having been the epicenter of a devastating COVID-19 outbreak, New York’s tax base has held up better than those of other major states. This is largely due to our heavy reliance on a progressive income tax. Even during the pandemic, we have continued collecting state income taxes from numerous well-paid remote workers, including nonresidents who haven’t set foot in New York since last March. Our income tax receipts have held up more strongly than expected in part because New York does, in fact, “tax the rich”—as reflected in estimated income tax payments, which come mainly from high-earning business owners, professional partners and investors. Those payments in January were up $1 billion from the previous year.

The economies of New York City and State will recover eventually—but how strongly, and how soon, are open questions. In the meantime, the Legislature’s guiding principal can be summed up in five words: don’t push more taxpayers away. Avoid giving any taxpayer—especially the high earners who already generate a disproportionate share of total revenues—an added incentive to leave or to disinvest in New York. In keeping with that priority, I would offer three recommendations:

- Reject the governor’s proposed income tax surcharge. Raising New York’s marginal rate to its highest level in 35 years, even temporarily, as Part A of the governor’s revenue bill would do, would send the kind of negative signal you need to avoid. The fiscal 2022 budget can be balanced without the $1.5 billion this would produce, based on recent tax receipts and federal aid trends.

- Postpone scheduled “middle class” personal income tax cuts for up to four years, not just one year. Provide for inflation-indexing of scheduled tax brackets during the suspension period and continuing after the cuts resume no later than 2026. The tax cut, which will subtract a total of $2 billion from revenue over the next four years, is desirable but cannot be considered essential at the moment.

- Reject the proposed extension of the Film Production Credit, now due to expire in 2025, and instead repeal the credit for productions after this year, saving $420 million a year.

One further revenue proposal for your consideration: Repeal the state and local sales tax exemption on clothing purchases under $110, which has a “tax expenditure” revenue impact of $800 million a year. To provide larger savings for families with children—the original intended beneficiaries of this overly broad, poorly targeted exemption—you could redirect $400 million of the savings to expansion of the existing Empire State Child Credit. This would adjust for the recent increase in the credit at the federal level.

Suspending scheduled income tax cuts for four years, repealing the Film Production Credit, and repealing the sales tax exemption on small clothing and footwear purchases would, net of the suggested child credit increase, raise $1.2 billion in 2023, rising to $2 billion by 2025—without hitting any New Yorker with a significant tax increase.

We are hearing that President Biden’s coronavirus relief bill would hand $50 billion to the state and to local governments in New York, including $12.7 billion in unrestricted aid and nearly $10 billion to K-12 education. Those numbers will change, but it seems likely a very large—but temporary—additional injection of federal COVID relief funding is coming to New York. The revenue actions I’ve proposed, combine with spending restraint and other reforms, can be saved to help finance a transition to a sustainable budget in the longer term when the aid is exhausted.

Unfortunately, despite the very shaky future of our tax base, the current legislative session has already seen the introduction or reintroduction of some of the most radical tax increase proposals New York State has ever seen. These measures are not designed to balance the budget without cuts, but to pay for vastly expanded state spending—on a scale never previously proposed or considered in New York.

Advocates of these tax hikes claim that New York’s income tax is regressive, taxing the poor as heavily or almost as heavily as the rich. They also claim there is no evidence that tax increases will drive income millionaires and multimillionaires out of the state. But they are wrong on both counts. In fact:

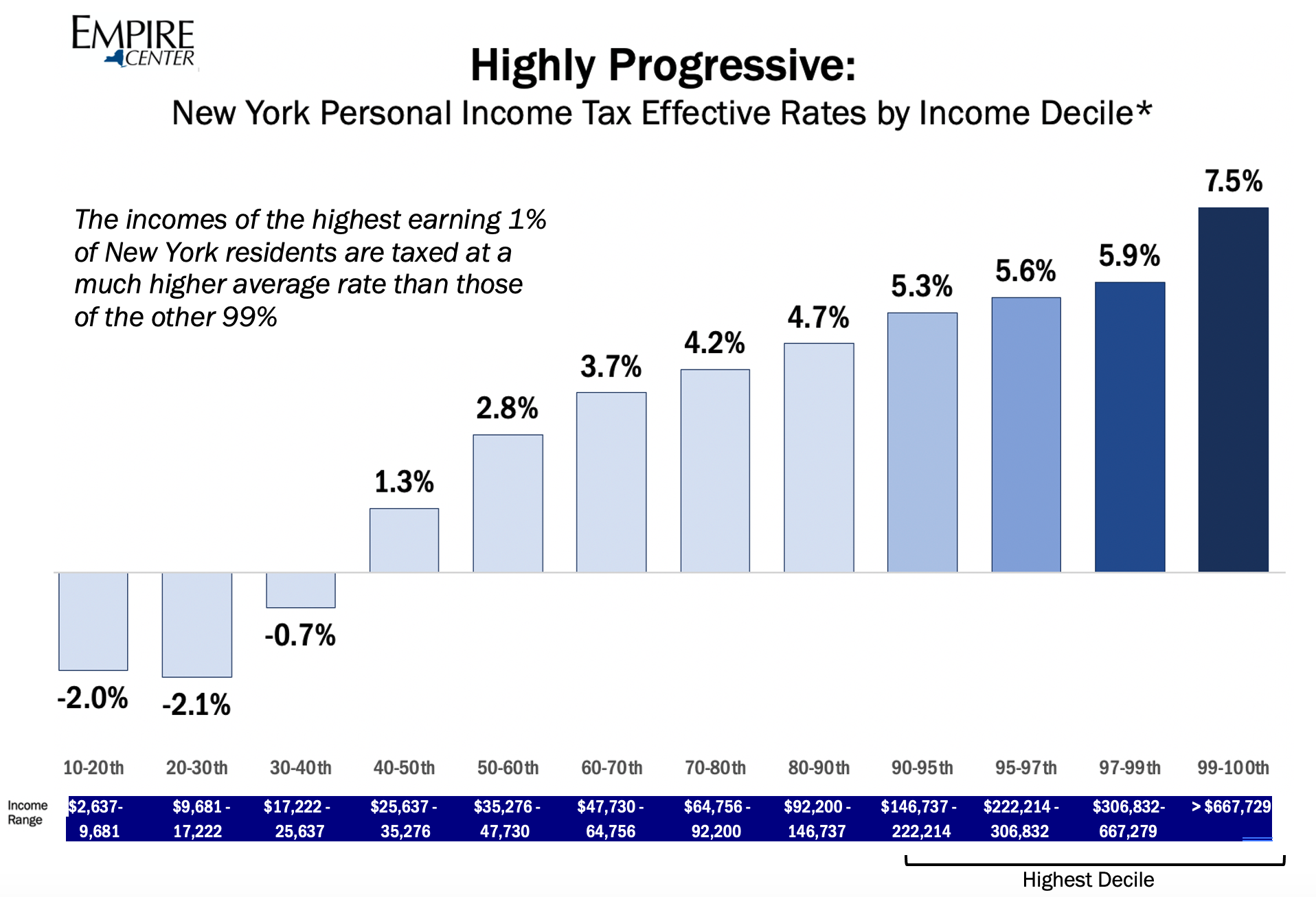

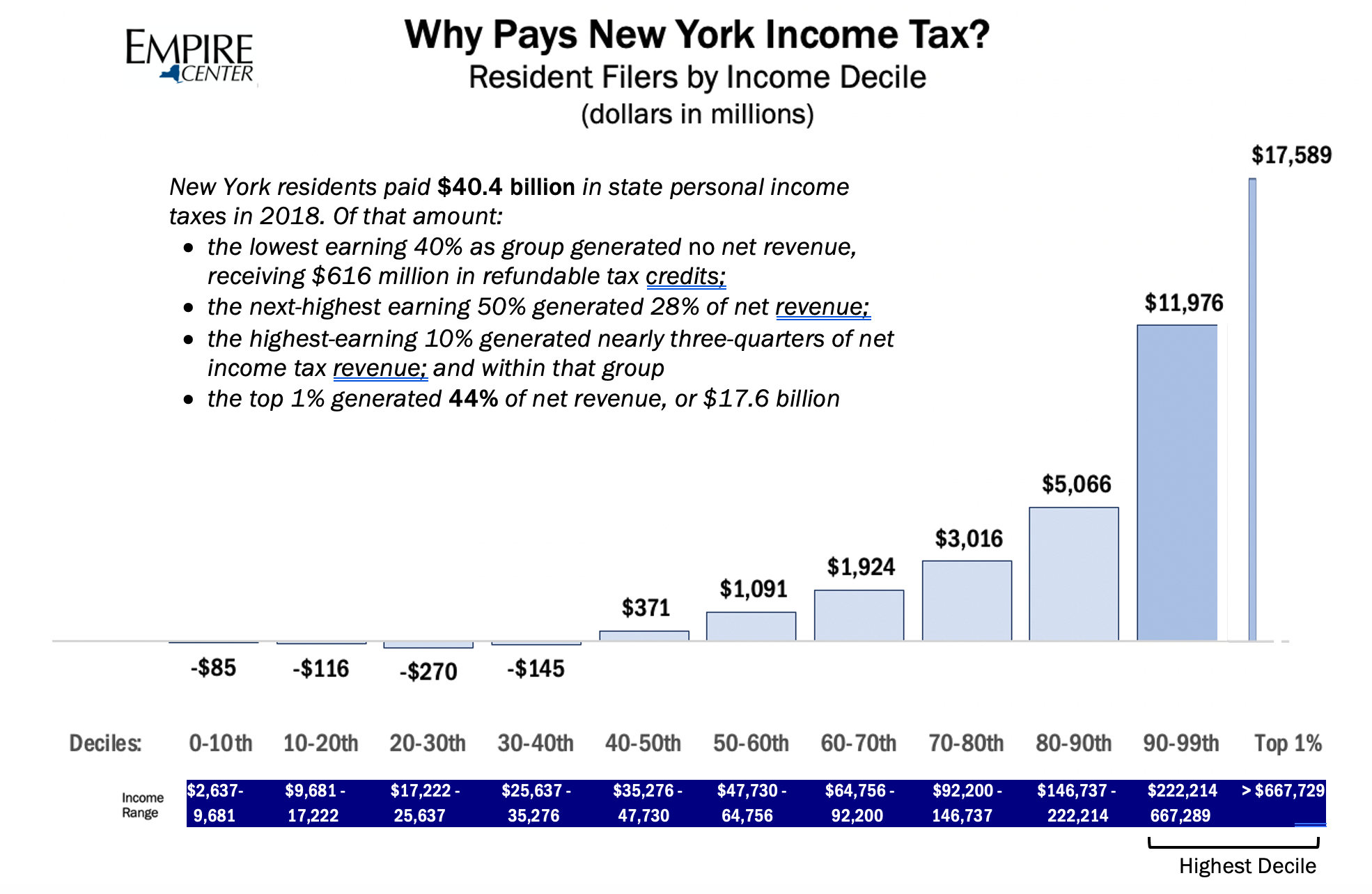

- The highest-earning 1 percent of New Yorkers generated nearly 44 percent of the total state income tax paid by state residents in 2018. By contrast, the lowest earning 40 percent of tax filers, with incomes of up to $35,276, collectively paid no taxes at all but received roughly $600 million in refunds and credits. [Appendix, Figures 1 and 2]

- Even prior to enactment of the millionaire tax in 2009, New York income tax consistently has ranked among the most progressive imposed by any state. By at least one measure, it’s the most progressive in the nation [Appendix, Figure 3].

- Since the Great Recession low point of 2009, New York’s share of the nation’s income millionaires has fallen, and their incomes have increased more slowly than those of similarly high earners in other states, including nonresident millionaire earners filing New York returns. Since 2000, there has been a steady increase in the nonresident share of all millionaires in our tax base, and a corresponding decrease in the resident share—now less than half the total. [Appendix, Figure 4]

Another perspective on the tax distribution issue [Appendix Table 1]: As of 2018, New York households with income above $10 million paid an average of $2.5 million in state income tax—as much as 438 households in the $100,000 to $150,000 bracket, 655 households in the $80,000 to $100,000 bracket, and 940 households in the $60,000 to $65,000. In other words, the loss of just 100 of the roughly 2,700 New York households with incomes above $10 million would equate to a loss of $250 million in tax revenues—equivalent to the total taxes generated by nearly 100,000 New York tax filers earning $60,000 to $65,000.

In addition to misrepresenting the tax code’s progressivity and discounting the unsettling impact of the pandemic, advocates of higher taxes on New York “millionaires and billionaires” consistently ignore the impact of the $10,000 cap on state and local tax (SALT) deductions enacted as part of the 2017 federal Tax Cuts and Jobs Act. With the SALT break virtually gone for the first time in history, the marginal rate in New York stands at its highest level ever—a noticeable increase in what might be called the “tax price” of New York, as compared to lower-taxed states.

Even before the SALT cap took effect, there were signs of erosion at the high end of New York’s tax base. From 2009—the recessionary low point following the financial crash, to 2018, the latest year for which data are available, the number of taxable returns filed by New York residents with incomes above $1 million increased by 92 percent. During the same period, the number of nonresident income millionaires in the New York tax base increased by 137 percent, according to state data. The total number of federal income taxpayers in the $1 million-and-above bracket increased by 128 percent.

Also from 2009 to 2018, the adjusted gross incomes (AGI) of New York resident income millionaires nearly doubled, from about $104 billion to $203 billion. During the same period, the AGI of nonresident New York filers in the same brackets more than tripled—increasing from $104 billion to $381 billion. The biggest increase among nonresident New York taxpayers was among those with incomes above $10 million, whose AGIs quintupled from $50 billion to $228 billion. According to IRS data, the AGI of all U.S. income millionaires increased by 145 percent, from $722 million to $1.8 trillion, from 2009 to 2018.

What I’m describing is correlation, not causation, obviously—but the data certainly do not support claims by tax hike advocates that higher tax rates haven’t mattered in New York, or that the state could raise its “millionaire tax” with impunity even before the pandemic disruption drove many New York income millionaires into temporary exile.

Raising taxes on the highest incomes to raise revenues in the short term will only accelerate the erosion of our tax base in the long run, ultimately undermining funding for the very programs the Legislature wants to protect. Even worse, as New York’s economy struggles to recover from the pandemic, enacting any one of the significant “millionaire and billionaire” tax increases now being promoted as a package could turn that erosion into a full-scale landslide.

APPENDIX to Testimony of Edmund J. McMahon

Figure 1

* Tax liability, after credits, as a percent of New York Adjusted Gross Income distribution for all full-year resident returns as of 2018. In lowest decile, not shown, total NYAGI and tax liability were both negative. New York City resident income tax not included

Source: New York State Department of Taxation and Finance, Personal Income Tax Filers Summary Datasets at https://www.tax.ny.gov/research/stats/statistics/pit-filers-summary-datasets-beginning-tax-year-2015.htm

Figure 2

Source: New York State Department of Taxation and Finance, Personal Income Tax Filers Summary Datasets at https://www.tax.ny.gov/research/stats/statistics/pit-filers-summary-datasets-beginning-tax-year-2015.htm

Figure 3

https://www.taxpolicycenter.org/sites/default/files/publication/131621/2000847-federal-state-income-tax-progressivity.pdf

Figure 4

Source: New York State Department of Taxation and Finance, Empire Center calculations

| Table 1. Average NYS Income Tax by Income Millionaire Bracket, and Equivalent Number of Middle-Class Taxpayers Based on Their Average Taxes, 2018 | ||||

| Equivalent Number of Taxpayers by Income | ||||

| Average NYS | $60,000- | $80,000- | $100,000- | |

| Adjusted gross income | Income Tax | $65,000 | $99,000 | $150,000 |

| $1 million – $2 million | $87,743 | 36 | 23 | 15 |

| $2 million – $5 million | $234,968 | 87 | 61 | 41 |

| $5 million – $10 million | $544,060 | 202 | 141 | 94 |

| > $10 million | $2,527,262 | 940 | 655 | 438 |

| Source: State Department of Taxation and Finance, Empire Center calculations | ||||

You may also like

Bill Hammond: Testimony to the Senate Aging Committee

Presented to the Senate Aging Committee

May 3, 2022

Read More

Peter Warren: Written Testimony to the Joint Legislative Fiscal Committees

Presented to the Joint Legislative Fiscal Committees

February 16, 2022

Governor Hochul’s budget plan is buoyed by a revenue surge attributable in no Read More

Bill Hammond Testifies on Public Health Spending in FY2022 Budget

The past year has taught a painful lesson about the importance of public health defenses, not just in terms of preventing sickness and death, but also preserving our economy and way of life. Read More

Residential Health Care Facilities and COVID-19 in Upstate New York

As the harrowing past few months have made clear, New York was both unusually vulnerable to the coronavirus and dangerously underprepared to fight it. Read More

Testimony: FY2016 New York State Budget

Changes made last year to the Corporation Franchise Tax and Estate Tax codes will help make New York a more attractive and competitive place to live, work and do business. However, there remains much to do. Read More

Testimony: FY2015 New York State Budget

Governor Cuomo’s 2014-15 Executive Budget would devote more resources to initiatives described as “tax cuts” than any state budget we’ve seen in quite a few years. This in itself is an encouraging sign of the recognition that New York needs to do more to shed its reputation as a high-cost, high-tax state.

Read More

Senate Testimony on State Tax Reform

This committee has chosen an opportune moment to review New York’s state tax code and consider reform options. Wall Street, the state’s cash cow for 20 years, is now retrenching. And in an era of slower economic growth, many businesses will be less willing to shoulder costs they can avoid by moving elsewhere. Needless to say, by various measures, most states can offer a lower-cost environment than New York. Read More

New York City Council Subcommittee on Forecasting and Revenue

Good afternoon, Chairman Weprin, and thank you for this opportunity to testify before your subcommittee today.

My name is Edmund J. McMahon, and I am senior fellow for tax and budgetary studies at the Manhattan Institute for Policy Research. The Manhat Read More