In what has become a rite of summer, the state Department of Financial Services on Wednesday approved substantially higher health insurance premiums for 2023 – but still proclaimed in a press release that it was “saving” consumers hundreds of millions of dollars.

That’s because the industry started out seeking much larger hikes, averaging 18.7 percent in the non-group market and 16.5 percent for small groups. After regulatory review known as “prior approval,” DFS cut those requested increases roughly in half, to average of 9.7 percent and 7.9 percent, respectively.

Without that intervention, DFS estimated that total premiums would have been almost $800 million higher.

But do New York’s state-imposed price controls on health insurance really save money over the long term? An analysis of federal data strongly suggests otherwise.

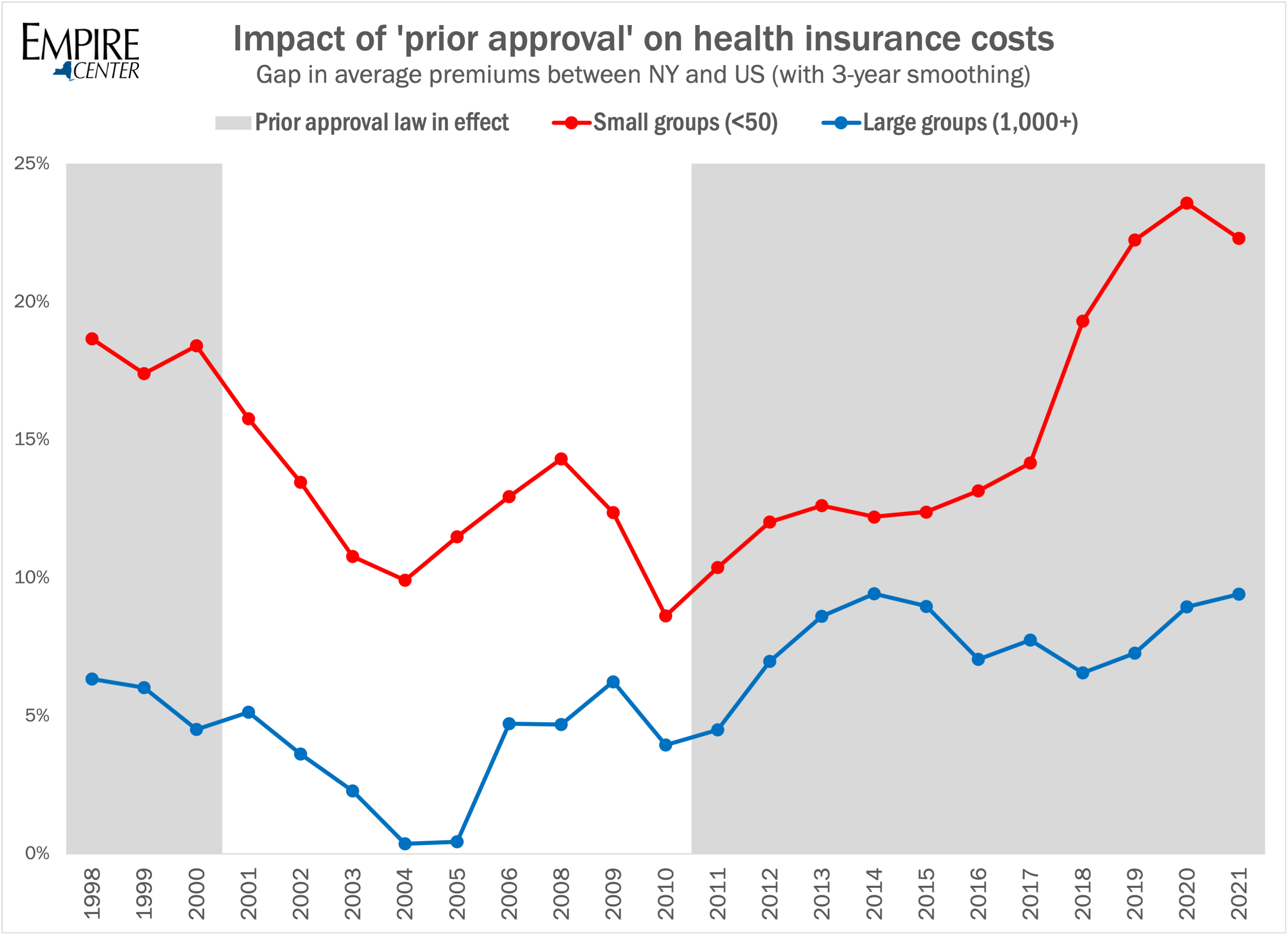

As a practical matter, the prior approval system mainly affects individual and small-group insurance plans. Most large employers operate self-insured health plans, which are generally exempt from state regulation under federal law. Thus comparing small- and large-group premiums is one way to gauge the effects of prior approval.

As shown in the chart below, drawn from annual federal surveys of employer-sponsored health benefits, New York’s premiums are generally higher than the national average regardless of group size. But the gap is significantly larger for small groups (which are subject to prior approval) than it is for large groups (which are mostly self-insured and exempt). Indeed, the disparity appears to have gotten substantially wider since the current prior-approval law took effect in 2011.

Source: U.S. Agency for Healthcare Research and Quality

As of 2010, the last year without prior approval, the three-year average affordability gap for small groups was five points higher than for large groups. As of 2021, after a decade of price controls, the gap for small groups was 13 points higher.

These results are the opposite of what would be expected if prior approval was working to keep costs down.

It’s evident from this analysis that the state’s price control system is failing to contain the cost of health insurance in New York. This is likely because it ignores the underlying costs that are the root cause of rising premiums. Those costs include the state’s extraordinarily heavy taxes in health coverage, and its ever-growing list of costly coverage mandates that legislators impose on insurance plans.

On a related note, DFS appears to have dropped a particularly outlandish claim about the impact of the Affordable Care Act on health premiums in the individual market.

From 2013 to 2020, the department asserted that its approved rates remained 50 percent or more lower than they were before the ACA. This was plausible at first, because New York’s pre-ACA premiums were exorbitantly high due to a dysfunctional combination of regulations and mandates known as a “death spiral.”

Over the next seven years, DFS approved cumulative increases of almost 80 percent above 2014, which would have eroded that original 50 percent drop. Yet as recently as 2020 the department’s press release asserted: “Rates for individuals [for 2021] are more than 55% lower than prior to the establishment of the New York State of Health in 2014, adjusting for inflation …”

In the following year’s announcement, however, no such claim was repeated. Its publication date was Aug. 13, 2021, three days after former Gov. Andrew Cuomo announced his resignation.

About the Author

You may also like

The Attorney General’s MFCU SNAFU

Attorney General Letitia James' latest fight with the Trump administration focuses on New York's Medicaid Fraud Control Unit, a federally funded agency housed in James' office.

On T Read More

Healthcare Revelations in the Enacted Budget Financial Plan

The state financial plan published on June 10 disclosed key information about healthcare revenue and spending that lawmakers had not made public when approving the annual budget two weeks before.

Read More

Federal Suit Traces Medicaid Fraud to the Top of NYS Government

The Trump administration's latest salvo against Medicaid fraud takes aim at a different kind of target – two high-ranking New York officials along with a major state contractor.

A Read More

Healthcare Highlights in the New State Budget

Governor Hochul's focus on affordability seems to have skipped over the healthcare portions of the new state budget.

The deal finalized May 27 Read More

Lawmakers Consider Hiking Fees for Filling Prescriptions

UPDATE: The proposal discussed below passed the Assembly Friday evening by an unofficial vote of 133-0. Having previously been approved by the Senate, the bill will head to Governor Hochul's desk for her signature or ve Read More

Budget Deal Reportedly Earmarks $100M for 1199 and Extends MCO Tax

As Governor Hochul and legislative leaders rush to finalize the overdue state budget, outlines of some healthcare-related deals have begun to emerge from the closed-door negotiations.

Read More

Albany Wavers on Shutting Down a Medicaid Racket

As Washington threatens to crack down on fraud and abuse in New York's Medicaid program, state legislators are doing their best to demonstrate why federal intervention is needed.

A Read More

Getting to the Bottom of the 340B Drug Discount Boondoggle

Some of New York's largest and most prosperous hospitals are reporting rapidly growing amounts of revenue from pharmacy sales – most of it apparently flowing from a controversial drug discount program known as 340B. Read More