State-regulated health premiums for 2020 are rising faster than the medical inflation rate for the sixth year in a row, yet the officials who signed off on the hikes insist they have saved consumers money – because average premiums are lower than what insurers originally requested.

State-regulated health premiums for 2020 are rising faster than the medical inflation rate for the sixth year in a row, yet the officials who signed off on the hikes insist they have saved consumers money – because average premiums are lower than what insurers originally requested.

Positive spin notwithstanding, it’s increasingly evident that the state’s nine-year-old price-control regime, known as “prior approval,” is failing as a strategy to keep health costs in check.

The bottom line of Friday’s announcement by the Department of Financial Services is that individual premiums for 2020 will rise by an average of 6.8 percent, and small-group premiums will be up 7.9 percent. Both numbers are well above the Consumer Price Index for medical care, which is currently less than 3 percent.

This round of hikes was hardly unusual. The average annual increase over the past six years was 9.8 percent for individual plans and 7.6 percent for small groups.

It’s true that the final rates are lower than what insurers applied for – by 2.4 points for individual plans, and 4.3 points for small groups. The more important question is: Are premiums lower than they would have been if the price controls did not exist at all? A close look at the data suggests the answer is no.

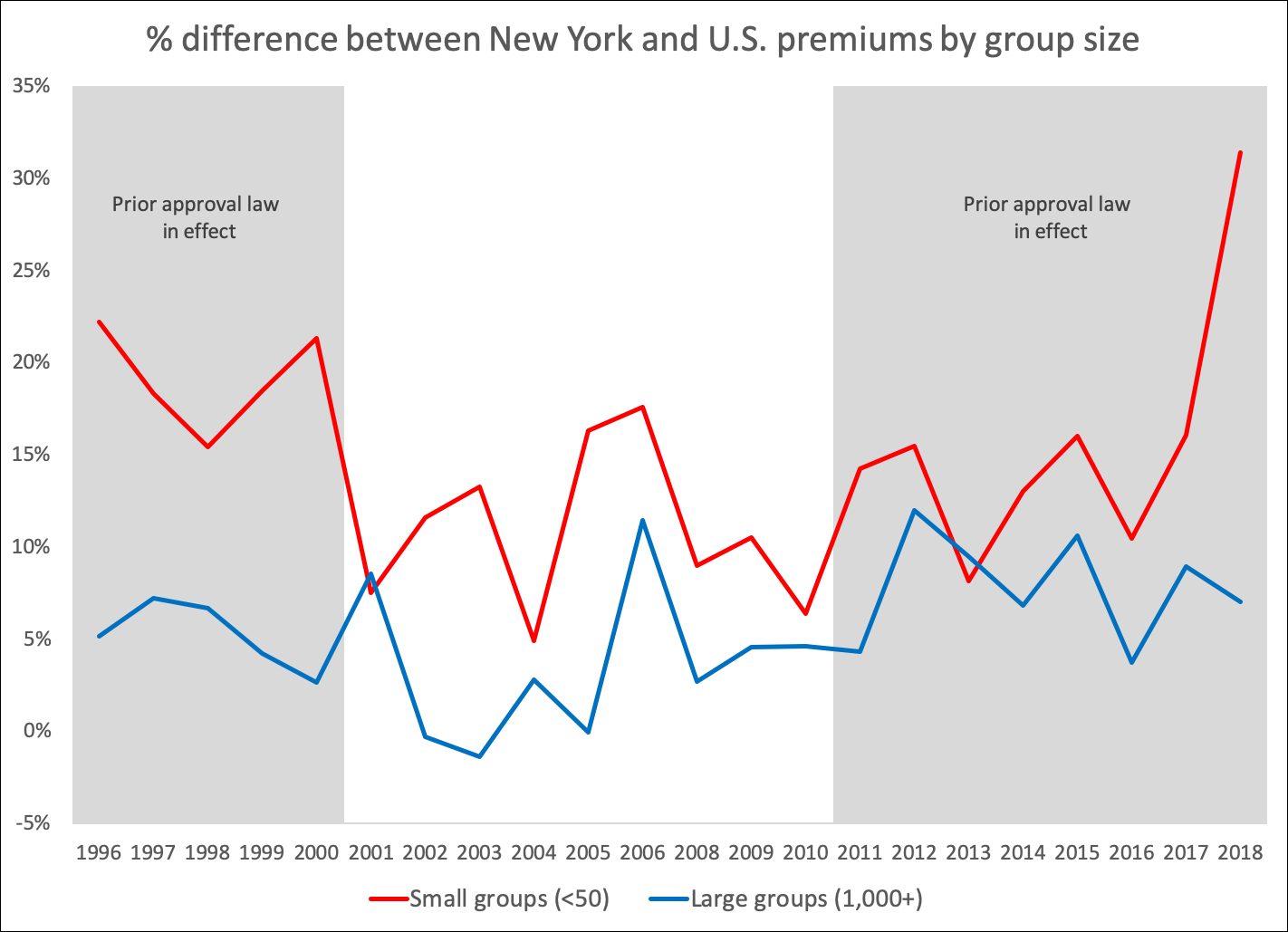

The prior approval law – which was repealed after 2000, then reinstated in 2010 – regulates policies sold to individuals and small groups but exempts large groups of 100 or more.

This sets up a kind of natural experiment: If the law were effectively controlling costs, regulated small groups would show signs of becoming more affordable relative to unregulated large groups. In fact, just the opposite is the case.

According to annual federal surveys, the difference between New York’s premiums and national averages is consistently higher for small groups than large groups – and the disparity seems to have gotten worse since prior approval took effect. (Because of how the federal data is categorized, this analysis compares small groups of fewer than 50 members to large groups of 1,000 or more. The survey focuses on employer-sponsored insurance and does not gather data on individual policies.)

For large groups, the affordability gap between New York’s premiums and the national norm has ranged since 2010 from 4 percent to 12 percent. For groups of fewer than 50, the gap ranged from 6 percent to a remarkable 31 percent in 2018, which was a 23-year high (see chart).

There’s no sign in these figures that prior approval is working at all. In fact, a case could be made that it’s making things worse.

For one thing, the give-and-take of the regulatory process encourages insurance companies to err on the high side when submitting their initial requests, knowing that they’re likely to get less in the end.

For another, prior approval does nothing to address the root causes that push premiums higher, primarily rising prices charged by drug companies, hospitals, doctors and other providers. Another factor is state policy – including heavy taxes on health insurance and a lengthening list of coverage mandates imposed on insurers.

Many large employers choose to “self-insure,” which exempts them from mandates and other state laws. Small groups, by contrast, are fully exposed to Albany’s regulatory regime.

The results of the current approach are seen in the table below: Single coverage for New York’s price-regulated small groups cost $2,094 more than the national average, while the gap for unregulated large groups is $478.

About the Author

You may also like

The Attorney General’s MFCU SNAFU

Attorney General Letitia James' latest fight with the Trump administration focuses on New York's Medicaid Fraud Control Unit, a federally funded agency housed in James' office.

On T Read More

Healthcare Revelations in the Enacted Budget Financial Plan

The state financial plan published on June 10 disclosed key information about healthcare revenue and spending that lawmakers had not made public when approving the annual budget two weeks before.

Read More

Federal Suit Traces Medicaid Fraud to the Top of NYS Government

The Trump administration's latest salvo against Medicaid fraud takes aim at a different kind of target – two high-ranking New York officials along with a major state contractor.

A Read More

It Is Time to Rethink the Regional Greenhouse Gas Initiative

Before budget negotiations, Gov. Hochul warned that unless New York changes its climate plans, New Yorkers could face a $2.26-per-gallon increase in gasoline prices. The reason is the so-called “cap-and-invest” scheme, under which energy companies wou Read More

Healthcare Highlights in the New State Budget

Governor Hochul's focus on affordability seems to have skipped over the healthcare portions of the new state budget.

The deal finalized May 27 Read More

Lawmakers Consider Hiking Fees for Filling Prescriptions

UPDATE: The proposal discussed below passed the Assembly Friday evening by an unofficial vote of 133-0. Having previously been approved by the Senate, the bill will head to Governor Hochul's desk for her signature or ve Read More

Lack of Common Sense on Energy in the Budget

Lack of Common Sense on Energy in the Budget

Anyone hoping the governor would make even modest, common-sense changes to New York’s disastrous energy policies will be disappointed. The energy portion of the budget is out, and the nons Read More

Budget Deal Reportedly Earmarks $100M for 1199 and Extends MCO Tax

As Governor Hochul and legislative leaders rush to finalize the overdue state budget, outlines of some healthcare-related deals have begun to emerge from the closed-door negotiations.

Read More