State Comptroller Thomas DiNapoli has just taken a big step to bolster the long-term financial stability of New York State’s largest public-sector retirement system.

DiNapoli announced today that he’s approved a recommendation by the State Retirement System Actuary to reduce, from 6.8 percent to 5.9 percent, the assumed rate of return (RoR) on investments by the $268 billion Common Retirement Fund, which underwrites the New York State and Local Employee Retirement System (NYSLERS) and Police and Fire Retirement System (PFRS), of which the comptroller is the sole trustee.

To be sure, even at 5.9 percent, the RoR that the pension fund literally counts on to pay constitutionally guaranteed benefits will remain considerably higher than the yields from commensurate low-risk U.S. Treasury or high-quality corporate bonds, which currently range from 2.3 percent to 3.3 percent. Nonetheless, in isolation, cutting the RoR assumption is an unequivocally good and prudent thing for the comptroller to do.

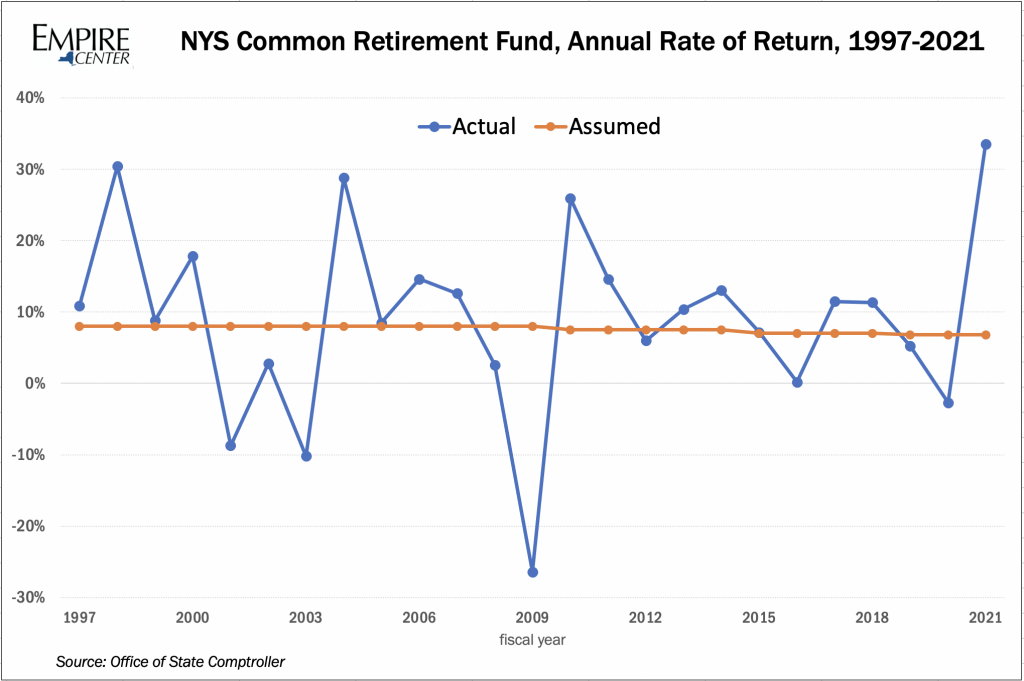

Assuming lower earnings also tends to result in higher required contributions by employers—which is why politically sensitive public pension fund administrators across the country have tended to set their RoRs at much higher levels than those required for private corporate plans. To guard against volatility in investment returns, which has been especially pronounced over the past 25 years, DiNapoli and other pension fund administrators also resort to “asset smoothing” — i.e., counting average market returns over several years—as a basis for estimating the assets available to pay retirement benefits. In New York’s case, the smoothing period is five years.

{kind=link}

But given his big reduction in the investment return assumption, sticking with smoothing would have minimized if not eliminated DiNapoli’s ability to reduce taxpayer-funded employer contributions starting next year. Unsurprisingly, while he’d like to get credit for adopting a more prudent RoR, he’d also like to save taxpayers money. And so he’s resorting to a bit of a gimmick: pension contributions for 2022-23 won’t be based on “smoothed” returns over the past five years but on a “restart” of actuarial asset measures based on the supercharged fiscal 2021 result—an all-time record return off 33.55 percent that wiped out the fund’s small loss early in the pandemic market crash.

The restart comes with risk: if investment returns over the next few years average below the assumed RoR, as they did in the early 2000s and again in the Great Recession, employer contributions will need to be sharply increased in just a few more years.

The most recent previous asset measurement re-start by the state pension fund occurred under DiNapoli’s predecessor, Alan Hevesi, following a stratospheric 28.8 percent investment return in 2004, which followed three years of net losses. Hevesi (and state taxpayers) got lucky: the restart was followed by three years of returns well above the RoR assumption at the time (8 percent). Just a few years earlier, New York City had been much less fortunate with a similar asset valuation restart pushed by Mayor Giuliani to help offset the cost of state-mandated pension benefit sweeteners in 1999. The city’s asset valuation restart was followed by a stock market downturn and recession, leading to subpar pension investment returns that led to an even sharper increase in tax-funded pension expenses.

Taxpayers to save

Thanks to the restart, and despite the move to a lower return assumption, DiNapoli has also been able to announce a sharp reduction in employer pension contribution rates for the ERS, from 16.2 percent to 11.2 percent of covered payroll for state fiscal year 2022-23. The PFRS contribution rate will be reduced by a smaller amount, from 28.3 percent to 27 percent of payroll. That translates into a big payoff for taxpayers, per the comptroller’s release:

According to the Fund’s Actuary’s estimates, the expected total employer contributions for Feb. 1, 2023 are $4.4 billion, which is $1.5 billion less than the expected employer contributions during the same period for 2022 – the lowest level since 2011.

To repeat: the restart gimmick is risky. But give DiNapoli credit: if he had also left the RoR at 6.8 percent—a technical maneuver few non-specialists would even have noticed—he could have exploited the restart to produce even larger taxpayer savings. In fact, if the RoR had stayed at 6.8 percent, the average employer contribution for ERS members would have dropped to near zero, and the PFRS rate could have been reduced by seven percentage points, according to the pension fund actuary’s estimate.

DiNapoli previously reduced the pension fund return assumption in stages from 8 percent to 7.5 percent in 2010, to 7 percent in 2015, and to 6.8 percent in 2019. At the new level of 5.9 percent, the New York fund’s assumed RoR will now be the second lowest among the nation’s 133 largest state and local government pension plans; only the much smaller Kentucky pension system, at 5.25 percent, has a lower return assumption, according to the National Association of State Retirement Administrators (NASRA). The median assumed rate of return among other large state funds is currently 7 percent, with only 34 plans lower than that, although some other states have announced intentions to further reduce their RoRs, DiNapoli noted.

DiNapoli estimated that the benefit promises of NYSLERS and the PFRS are now 99.33 percent funded by assets on hand to pay them. Even adjusting for a lenient public-sector accounting standards on which that estimate is based, New York State has one of the nation’s best funded public pension funds.

You may also like

NY Taxpayers Face Bitter Truth from Sweeter Pensions

Governor Hochul and state lawmakers this year approved a costly giveaway for public employee unions that retroactively hiked pension benefits. Now the bill is arriving. Read More

Unions are pressing bogus arguments for blowing up NY’s public pension debts

New York's public employee unions are arguing, without evidence, that state lawmakers need to retroactively sweeten the pensions of workers who have been on the job for more than a decade. In fact, state and federal data show why state lawmakers shouldn't. Read More

Senate, Assembly Budget Plans Include $4B Pension Giveaway

A little-noticed provision in lawmakers’ budget proposals would also be the most costly: their proposal to change state retirement rules would slam New York taxpayers with more than $4 billion in new debt, and immediately drive up pension costs, by retroactively sweetening the pension benefits of public employees. Read More

The False Claim Behind Albany’s Gray Scare

Public employee unions — and Governor Hochul — are pressuring state lawmakers to increase hiring at state agencies because, they say, more than a quarter of the state workforce is poised to retire. Read More

The Gov’s pension

There are several (dozens? hundreds?) of unanswered questions as the fallout from Andrew Cuomo's resignation earlier today continues. Among those are questions related to his pension, some of which can be answered, sort of.

Read More

Pension woes for 1199

Two pension funds affiliated with 1199 SEIU, the state's largest and most influential union for health-care workers, recently disclosed that they are in critical status due to funding or liquidity problems for an 11th straight year. Read More

The pension piece of “prevailing wage”

New York’s AFL-CIO has issued a statement blasting the “misinformation campaign” by business groups fighting organized labor’s push to impose union pay levels on private developments receiving public subsidies.

There is, indeed, plenty of misinformation wafting around this issue—but virtually all of it originated in the union camp. Read More

NY state pension fund earnings slump

New York's Common Retirement Fund (CRF) fell nearly two percentage points short of its investment earnings target last year—and the state's other major public pension funds are on the same sub-par track. Read More