![]() The New York State Teachers’ Retirement System (NYSTRS) will reduce its taxpayer-funded pension contribution rates for a third consecutive year in 2017-18, even though the pension fund’s investment returns came in well below its target rate in fiscal 2016.

The New York State Teachers’ Retirement System (NYSTRS) will reduce its taxpayer-funded pension contribution rates for a third consecutive year in 2017-18, even though the pension fund’s investment returns came in well below its target rate in fiscal 2016.

NYSTRS, which covers all public school teachers and administrators outside New York City, needs to earn 7.5 percent a year to match its actuarial assumptions. However, the $107.5 billion pension fund earned just 2.3 percent last year, actuary Richard Young told the NYSTRS board this week.

During the year ending June 30, NYSTRS actually outperformed some of its larger counterparts—including the New York City pension funds, which earned an average of 1.5 percent, and the California Teachers Retirement System, which reported a return of 1.4 percent. NYSTRS also fell short in fiscal 2015, with a return of 5.2 percent.

Nonetheless, Young told NYSTRS trustees that the teacher pension contribution rate billed to employers as a percent of covered payroll will drop, from 11.72 percent of 2016-17 payrolls to between 9.5 and 10.5 percent of 2017-18 payrolls. This will save participating employers, mainly school districts, up to $300 million. That’s on top of $800 million a year districts have saved from reduced rates over the past two years. Suffice to say, you will not hear this number mentioned much when public school advocates claim the property tax cap is starving them of resources.

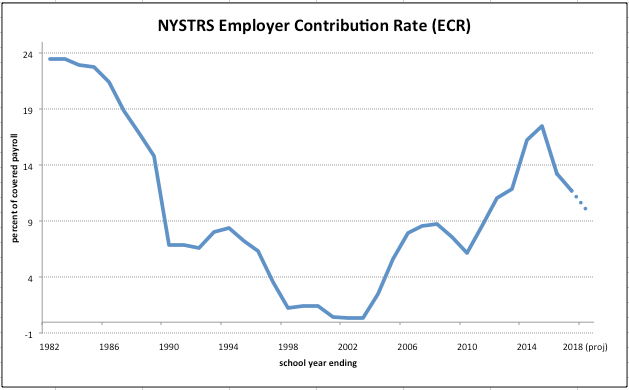

The chart below traces the NYSTRS employer contribution rate since the 1981-82 school year, including the projected level for 2017-18.

As shown, the rate fell to negligible levels in the 1990s, then spiked after the stock market downturn of 2000-02, then spiked again, at a 28-year high of nearly 18 percent, in 2014-15. This kind of volatility is a feature, not a bug, of the traditional pension system, which guarantees a high level of wage replacement to retired teachers based on optimistic return assumptions rooted in risky investment strategies.

By public-sector standards, NYSTRS is an exceptionally well-funded pension system. But using the real-world standards favored by a broad consensus of private-sector actuaries, economists and financial experts, it is still underfunded.

As explained here last year, NYSTRS’ seemingly counterintuitive trends of below-target investment returns and dropping pension costs in the short term is a figment of magical accounting rules under which public pension funds operate. While the continuing savings will be real enough in the short term, the NYSTRS contribution rate is actually too low.

The fund’s investment advisors calculate that its current mix of assets, adjusted for risk, will earn 6.6 percent a year, nearly identical to the return predicted by NYSLRS actuaries. That, in fact, is the maximum rate the fund ought to be assuming as the basis for contributions, even if you accept the dubious premise that public funds can be less conservative than private ones because they have taxpayers as a backstop. But a 6.6 percent assumed rate of return would drive NYSTRS contribution rates back above 20 percent of salaries, a level last seen more than 30 years ago.

You may also like

NY Taxpayers Face Bitter Truth from Sweeter Pensions

Governor Hochul and state lawmakers this year approved a costly giveaway for public employee unions that retroactively hiked pension benefits. Now the bill is arriving. Read More

DiNapoli bolsters pension fund stability—and cuts tax-funded costs

DiNapoli announced today that he's approved a recommendation by the State Retirement System Actuary to reduce, from 6.8 percent to 5.9 percent, the assumed rate of return (RoR) on investments by the $268 billion Common Retirement Fund, which underwrites the New York State and Local Employee Retirement System (NYSLERS) and Police and Fire Retirement System (PFRS), of which the comptroller is the sole trustee. Read More

The Gov’s pension

There are several (dozens? hundreds?) of unanswered questions as the fallout from Andrew Cuomo's resignation earlier today continues. Among those are questions related to his pension, some of which can be answered, sort of.

Read More

The new (old) normal of NY pensions

The Empire State's largest public pension plan still has not fully recovered from the financial crisis and Great Recession of 2008-09, a new report from the state comptroller's office confirms. Read More

DiNapoli’s “slight gains” in context

New York's largest public pension fund earned 2 percent in its first fiscal quarter—which isn't necessarily good or bad news for taxpayers. Read More

NYC pension costs shooting up

Taxpayer-funded pension contributions in New York City will need to increase by a total of $732 million between fiscal years 2018 and 2020 due to the pension funds' paltry investment earnings in the recently concluded 2016 fiscal year, City Comptroller Scott Stringer has just disclosed. Read More

Skelos pension could exceed $95k

Following his conviction on federal corruption charges, former Senator Dean Skelos apparently will qualify for a public pension of up to $95,590 a year. Read More

A losing quarter for NYS pensions

Still betting far too heavily on the stock market, New York State's main state and local government pension fund lost money in the first half of its current fiscal year. Read More